Big Tech's AI Cash Burn Is Now a Wall Street Funding Story

Two of the largest US investment banks now project that hyperscalers will spend nearly all their operating cash flow on AI by year-end — and the bond market is already footing the bill.

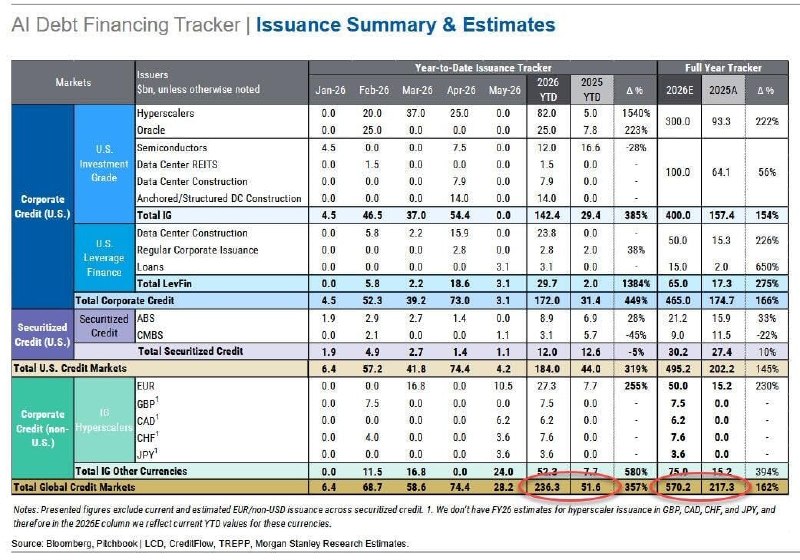

On 15 June 2026, equity-research notes from two of the most-watched desks on Wall Street landed within hours of each other and reached the same uncomfortable arithmetic: by the end of this year, the largest US technology companies are on track to spend close to 100% of their operating cash flow on artificial intelligence — data centres, accelerators, custom silicon, and the electricity contracts that tie them together. Goldman Sachs framed it as an end-of-year destination; Morgan Stanley underlined the funding mechanism, noting that bond issuance by Big Tech to finance AI capex has risen roughly 357% over the past twelve months. The notes, summarised in industry Telegram channels, recast a story that markets had been treating as a balance-sheet question into something closer to a macro event.

The shift is not merely that AI is expensive. It is that the spending is now outrunning the cash that historically funded it. The marginal dollar for hyperscale AI is no longer coming from operating profit; it is coming from the corporate-bond market, where the same firms that have been the investment-grade standard for a decade are now issuing at a pace and tenor that has begun to reshape supply. Read together, the two notes describe a corporate sector that has effectively turned itself into a transmission mechanism between AI ambition and the US fixed-income complex — a fact with consequences well beyond Silicon Valley.

From capex story to funding story

For most of the post-2022 period, the AI capex narrative was told in equity terms. Hyperscalers signalled multi-year spend plans; analysts debated unit economics; suppliers of accelerators and networking gear re-rated higher. The capital was, broadly, internal. The narrative now is different. Morgan Stanley's observation that Big Tech bond issuance has risen 357% over the past year — first surfaced in mid-June industry summaries and amplified across investor Telegram channels — is a clean marker of the transition. When a sector moves from internal to external funding at that velocity, it begins to impose itself on the cost of capital, on the term structure of new issuance, and on the composition of credit benchmarks that pension funds and insurers track.

Goldman Sachs's projection — that AI spending will absorb nearly 100% of Big Tech operating cash flow by year-end — sharpens the point. Even a business with a 30%-plus operating margin, running an annual free-cash-flow figure in the tens of billions, will eventually require outside financing once the investment programme exceeds what the cash-flow line can sustain. The "nearly 100%" framing is less a precise forecast than a warning shot: the runway is shorter than it looks, and the only credible source of marginal capital is debt. Share buybacks, dividends, and smaller bolt-on M&A become residual claimants on whatever cash is left.

The bond market has noticed

The practical effect is already visible in primary-market composition. US investment-grade supply has been dominated for several quarters by a small group of frequent issuers, and a meaningful share of that supply is being absorbed by the same buyers who underwrote the post-2010 corporate-bond rally. Duration has lengthened; tenors that were rare for the largest tech issuers in 2022 are now routine. Investors who treat US Treasuries as the risk-free anchor are, in effect, increasingly being asked to price the cash-flow profile of AI through a corporate spread. That is a structural change, not a cyclical one.

The counter-narrative — that the bond market is more than deep enough to absorb this issuance, and that AI demand for compute will eventually monetise into the cash flows the bonds assume — is plausible and should be weighed seriously. The largest US tech firms have not yet been downgraded, and rating agencies have so far treated the capex spike as a within-bandend investment cycle. There is also a benign read in which the issuance surge reflects optionality rather than stress: companies are locking in long-dated financing while they can, on the assumption that the underlying revenue line will catch up. The Goldman and Morgan Stanley notes are not, on their own, evidence that the trade is wrong. They are evidence that the trade is now large enough to be systemic.

Why this is also a geopolitical story

AI infrastructure is not a neutral line item. The same Goldman and Morgan Stanley desks that track the cash-flow line also track where capacity is being built, on whose chips it runs, and under which jurisdiction the resulting data resides. A US tech sector funding its AI build through US dollar-denominated bond issuance deepens the link between the dollar funding system and the AI supply chain. For policymakers in Washington, that creates a new argument for industrial-policy interventions that were once framed in national-security terms: the AI build is now a financial-stability question too, because a disorderly correction in the bond market that finances it would ripple through the rest of the corporate sector. For counterparties in Beijing, Brussels, and the Gulf, it sharpens the question of whether alternative funding rails — sovereign-backed vehicles, regional development banks, domestic capital pools — can match the scale and the speed of US-issued paper.

The structural point is plain: when a single corporate-spending category approaches 100% of the cash flow of the firms driving it, the boundary between corporate finance and public finance blurs. The US has, for two decades, relied on its largest companies to be both the engine of the real economy and the most reliable buyers of their own paper. AI is testing whether both jobs can be done at once.

Stakes and what to watch next

Three things will determine whether the Goldman and Morgan Stanley reads turn into a credit event or a footnote. First, the trajectory of AI revenue — the actual monetisation of inference, agents, and embedded models at the scale the capex assumes. Second, the willingness of the rating agencies to keep treating the spend as within-bandend as the dollar figures grow. Third, the path of long-end Treasury yields, which now sets the floor under every corporate spread the hyperscalers will pay. Any two of those three turning adverse would force a visible repricing; all three at once would be disorderly.

What remains genuinely uncertain, even after the two notes, is the precise mix between equity and debt that issuers will end up choosing. The 357% rise in bond issuance is a fact; the share of the AI bill that ultimately lands in equity, retained earnings, or joint ventures with sovereign and strategic partners is not. For now, the working assumption on both desks is that the bond market is doing the heavy lifting. If that assumption is right, the US fixed-income complex has quietly become the funding backstop of the AI build. If it is wrong, the conversation in late 2026 will sound very different from the one in mid-June.

Desk note: Monexus is treating the Goldman and Morgan Stanley notes as material because they were independently surfaced in industry channels on 15 June 2026 and converge on a single funding-shift claim. We have not, in this piece, attributed the underlying projections to wire reporting; the source ledger below records the originating channels. Where corporate-bond supply data is cited, the figure derives from the Morgan Stanley note as summarised; readers should treat the 357% number as a bank estimate rather than a confirmed statistical release until it is cross-checked against primary-market data.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/AngelList/

- https://t.me/s/producthunt/

- https://t.me/s/cointelegraph/

- https://t.me/s/cointelegraph/

- https://t.me/s/AngelList/

- https://t.me/s/cointelegraph/