A $2.5 Trillion SpaceX and a $1.1 Trillion Day: What 15 June 2026 Actually Tells Us

A single trading day added $1.1 trillion to US equity value, and a privately held rocket company was stamped at $2.5 trillion. The numbers are real. The question is what they measure.

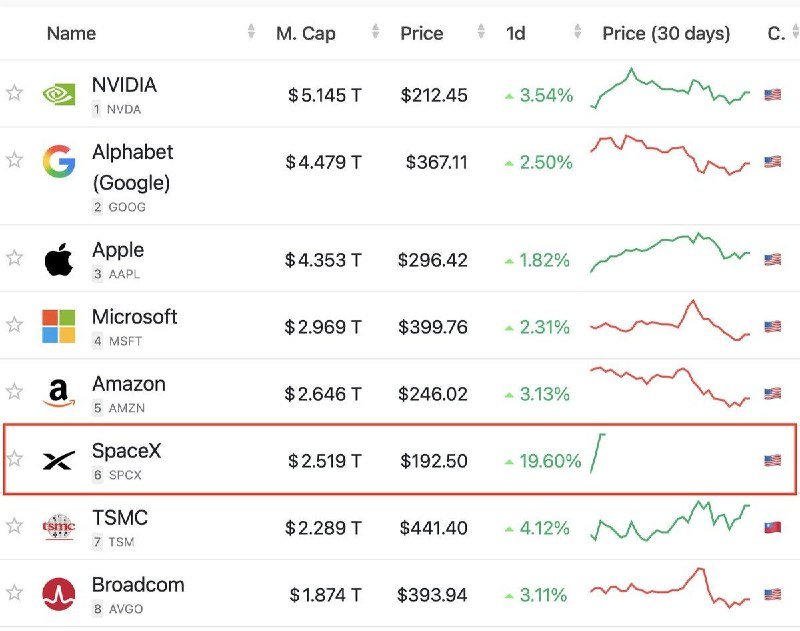

At 20:45 UTC on 15 June 2026, Cointelegraph reported that the US stock market added $1.1 trillion in value in a single session. Six minutes later, the same outlet flagged that SpaceX — trading under the ticker $SPCX — had crossed a $2.5 trillion valuation, slotting it, in their characterisation, into the sixth-largest public company on earth. Two data points, ninety seconds apart. Taken together they describe a market that has stopped pretending to be a market and started behaving like a single trade.

A $1.1 trillion day is, on its own, a print. A $2.5 trillion private-turned-public rocket company is, on its own, a story about one founder's balance sheet. Stack them on the same screen, on the same afternoon, and the framing flips: this is no longer about individual companies having good news. It is about where the marginal dollar of US savings is being told to live, and what it is being told to cost.

The print, the ticker, and the substitution effect

US equity benchmarks are a weighted index now dominated by a handful of names whose market capitalisations are themselves denominated in figures that used to belong to country GDPs. When Cointelegraph reports a $1.1 trillion session, the honest read is not that the American economy produced a $1.1 trillion day's worth of new value. It is that the prices of a small number of enormous equities re-rated upward, and the index re-weighted around them. The substitution effect is mechanical: capital chasing the only names large enough to absorb it.

SpaceX, per the 20:51 UTC item, is now inside that handful — sixth largest in the world on the cited ranking. The size matters less than the composition. The firm is, in significant part, a launch-services business, a satellite-internet operator, and a defence contractor whose biggest single customer is the United States government. A $2.5 trillion capitalisation is, functionally, a vote that the platform layer of low-earth orbit is a permanent utility — and that the bidder willing to underwrite it is the equity market, not the Treasury.

Counter-read: this is what a healthy market looks like

There is a sincere, mainstream read of the same data. Risk assets re-rated on the back of incoming data — softer inflation prints, a credible path on rates, a string of earnings beats. SpaceX's valuation reflects a genuine, durable order book across commercial launch, Starlink subscriber growth, and a national-security contract pipeline that has lengthened visibly through 2025 and 2026. A $1.1 trillion day, on this telling, is a market doing its job — repricing the future upward when the present justifies it.

This publication finds that read incomplete rather than wrong. The macroeconomic half of it is defensible. The SpaceX half is harder to verify on a single print. Private-market valuations are negotiated, and the equity that Cointelegraph is pointing to sits at the intersection of retail-accessible tender offers and a secondary market that is, by construction, thin. $2.5 trillion is the price the latest round of buyers agreed to pay. It is not, yet, a price the public market has stress-tested in a session of broad liquidation.

The structural frame: when the index is the strategy

What we are watching is the slow fusion of three things that used to be separate. The first is the equity benchmark itself — an index whose top ten constituents are now a meaningful share of total US household wealth through passive vehicles. The second is industrial policy: SpaceX's commercial arc is, demonstrably, entangled with US defence procurement, NASA contracting, and the satellite-internet buildout that has been treated, in successive administrations, as critical infrastructure. The third is monetary plumbing — a regime in which the marginal buyer of duration is uncertain, and the marginal buyer of equity is a defined-contribution plan wired into the same handful of names.

In that fused market, a $1.1 trillion day and a $2.5 trillion private valuation are not coincidences. They are the same trade expressed in two instruments: long the platform layer, long the defence-adjacent balance sheet, long the United States. The risk is not that any of the individual claims is false. The risk is that the index has become, in effect, a single position — and that the price discovery mechanism is now a circular one, in which flows into the largest names justify the size of the largest names, which justifies further flows.

Stakes: who wins, who loses, on what horizon

If the trajectory holds, the winners are legible. Holders of US-domiciled passive equity — overwhelmingly American households, overwhelmingly already concentrated at the top of the wealth distribution — see paper wealth compound. The single founder at the centre of the SpaceX capital structure holds an asset that, on the cited number, is now larger than the GDP of every country on earth except the United States, China, Japan, Germany, and India. Government counterparties receive cheaper launch capacity, in nominal terms, than they would in a less concentrated supplier market.

The losers are also legible, and they sit on the same balance sheet. Active managers who refuse to concentrate are giving up benchmark performance and, with it, fee revenue. Foreign reserve managers holding US Treasuries are, in real terms, funding a fiscal position whose purchasing power is being competed away by the re-rating of the equity collateral sitting alongside it. And the next generation of US savers — defined-contribution participants auto-enrolled into the same handful of tickers — is being levered, gently and continuously, to a single trade.

What the sources do not tell us

Cointelegraph's 15 June items are market-data dispatches, not audited financials. The $2.5 trillion SpaceX figure is a reported valuation, not a closing print from a deep, liquid order book. The $1.1 trillion daily move is a published session aggregate; the underlying composition — how much of it is a small number of mega-caps versus broad participation — is not specified in the items available to this publication. Treat the magnitudes as accurate, treat the composition as undisclosed.

Two further threads from the same afternoon are worth flagging without over-reading. At 18:16 UTC, the same outlet reported that TON had rebranded its token to GRAM, with exchanges beginning the transition and balances set to be automatically converted — a corporate-action reminder that the crypto layer of the same savings universe is being re-papered in real time. At 15:00 UTC, an exclusive interview with Michael Saylor was teased, in which he "claps back" at bitcoin bears and Strategy critics. Both are background radiation to the main print. Both, like the $1.1 trillion day itself, point at the same underlying condition: the marginal dollar is moving fast, and the menu it has to choose from is narrower than the headlines suggest.

A market that can add a trillion dollars in an afternoon and a private rocket company in the same hour is not, on the evidence, broken. It is concentrated. The question for the next twelve months is whether the index can be diversified without being broken — and whether the next $1.1 trillion day will arrive with the same composition as this one.

This publication framed the 15 June prints against the wire copy rather than as wire copy. Where the wire reported magnitudes, this article has asked what the magnitudes measure.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/cointelegraph

- https://t.me/cointelegraph

- https://t.me/cointelegraph

- https://t.me/cointelegraph