SpaceX leapfrogs Amazon, Musk's net worth eclipses Bitcoin — and Anysphere lands in the orbit of the world's seventh-largest asset

A single trading session added $164.8bn to Musk's paper fortune, pushed SpaceX past Amazon, and saw his personal wealth eclipse Bitcoin's market capitalisation — before the day closed with news of a $60bn Anysphere acquisition that folds the maker of Cursor into xAI.

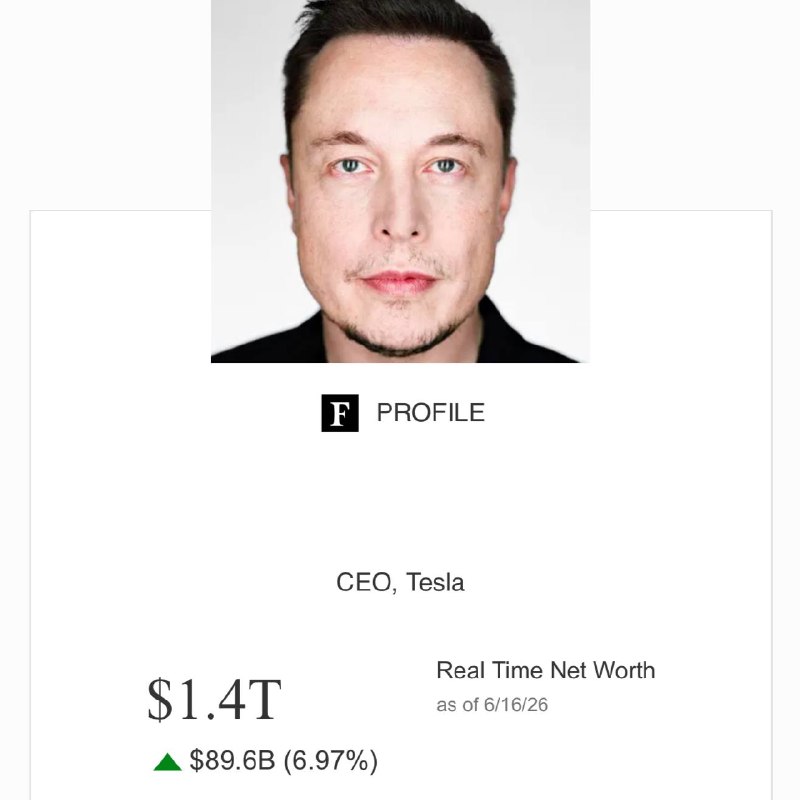

On 16 June 2026, in a single trading session, Elon Musk's net worth jumped by $164.8bn to roughly $1.3trn, the largest one-day paper-wealth gain any individual has recorded in a year of repeated records. Hours later, the same wire reported that SpaceX had overtaken Amazon to become the world's seventh-largest asset by market capitalisation, and that Musk's personal net worth had surpassed the entire market capitalisation of Bitcoin. By the middle of the UTC afternoon, the day's news had moved from valuation to corporate action: SpaceX agreed to acquire Anysphere, the four-year-old developer of the AI coding tool Cursor, for $60bn, and fold it into xAI. The deal pushes SpaceX's market capitalisation to $2.8trn, according to the wire report.

The numbers, taken together, describe an extraordinary concentration event. In roughly a decade, Musk has gone from being the public face of two listed companies to controlling a private-space-and-AI conglomerate whose market value now sits between Saudi Aramco and the largest US tech platforms. That reordering deserves a calmer look than the price-tape suggests.

The mechanics of a $164.8bn day

The trigger for Musk's one-day paper gain was a SpaceX-led private-market re-rating, not a broad equity rally. Cointelegraph's wire item, posted at 05:09 UTC, framed the move as a SpaceX-driven repricing, with the post-money value of Musk's SpaceX stake flowing through to his net-worth tally. The market-cap move that displaced Amazon — reported at 14:01 UTC — appears to be the same event reaching the consolidated-asset league tables: a single private company's valuation, jumping enough in one session to leapfrog a public hyperscaler with $600bn-plus in annualised revenue.

The data points are reported, not adjudicated. The $164.8bn figure is the kind of headline that depends on which private-market reference price is used for SpaceX, what discount (if any) is applied for illiquidity, and which Forbes or Bloomberg tracker does the consolidation. The wire does not specify the source of the print; the headline number moves with the bid. What is not in dispute is the direction.

When personal wealth outpaces a top-five asset

The Bitcoin comparison is the more revealing claim. Bitcoin's market capitalisation, even after the spot-ETF flows of the past two years and the 2024 halving cycle, sits in a band that a single individual's paper net worth is now reported to exceed. Whether one accepts the precise figure or not, the framing is meaningful: a private holding in a private company, marked at a private-market clearing price, is now being compared to the value of a public, freely-traded, globally-distributed monetary network.

The counter-narrative is straightforward and worth stating. Net worth, even for the ultra-wealthy, is mostly illiquid. Musk cannot wire $1.3trn; he can sell Tesla shares subject to a 10b5-1 plan, borrow against his SpaceX stake, or, as he has done repeatedly over the past five years, use his holdings as collateral to fund other ventures. Bitcoin's market cap, by contrast, is the cumulative price of a circulating asset that any holder can sell into a liquid order book at any moment. The comparison, in strict liquidity terms, is misleading.

It is also politically significant. The same week that the US Treasury has been warning about stablecoin reserve composition, the most-circulated chart in crypto-Telegram is one that puts a single individual's paper wealth above the network's market value. The framing favours neither Musk nor Bitcoin; it simply illustrates how far private-asset valuations have detached from the public markets that once set the tone for the rest of the economy.

The Anysphere deal — and what $60bn for Cursor actually means

The day's second act is the more consequential for the technology sector. Cointelegraph, at 15:12 UTC, reported that SpaceX would acquire Anysphere — the company behind the AI coding application Cursor — for $60bn and integrate it with xAI. If confirmed at that valuation, the deal ranks among the largest private-software acquisitions on record. Cursor is a four-year-old product built on top of large language models; it is best understood as a developer-experience layer that has, by 2026, become a default interface for working with code-generating models in the way spreadsheets once were for finance.

The strategic logic is harder to miss. xAI has been building out a vertically integrated AI stack — its own model training cluster, its own data-centre capacity, and a chatbot product competing with OpenAI and Anthropic. Acquiring the dominant coding-assistant product gives xAI a distribution surface in the developer market, the same way Microsoft leveraged GitHub Copilot to anchor enterprise AI. The reported $60bn price is steep by traditional software multiples; it is defensible if Cursor's user base is treated as a strategic asset rather than a SaaS revenue line. The wire does not disclose revenue, retention metrics, or how much of the consideration is equity versus cash.

For Musk's broader portfolio, the deal ties xAI more tightly to SpaceX's balance sheet. SpaceX's reported $2.8trn post-money valuation provides the equity currency to make a $60bn acquisition look small. It also deepens the question of how the companies relate: whether xAI is a subsidiary, a sister company, or — as some filings have hinted — increasingly indistinguishable from SpaceX at the operational level.

The structural picture, in plain terms

A handful of actors now control most of the world's most strategic private infrastructure: launch capacity, satellite broadband, frontier AI compute, and the developer tools that ride on top. Public markets still set the marginal price for the largest US tech platforms, but private markets now set the price for the assets that will define the next decade of capacity. The lesson of 16 June 2026 is not that Musk is rich; it is that the gap between private-asset valuations and public-market valuations has grown large enough that a single private company's re-rating can rearrange the global league tables in a single session.

The stakes are concrete. If the trajectory continues, the technology stack on which the next generation of products, services, and possibly defence systems is built will be increasingly concentrated in the hands of a small number of private firms whose disclosure obligations are limited. That concentration is not unique to Musk; it is the shape of the industry. The Anysphere deal illustrates how that concentration accelerates: a privately-held frontier-AI lab uses the equity currency of a privately-held launch company to buy a privately-held developer-tools company. The chain has no public-market anchor, no tender offer, and no shareholder vote. The consolidation is real; the scrutiny is not.

What remains uncertain

Several pieces of the picture have not been independently confirmed at the time of writing. The $164.8bn daily net-worth gain and the $1.3trn headline figure depend on the private-market reference price for SpaceX; the wire does not identify the data provider. The reported $2.8trn SpaceX post-money valuation and the $60bn Anysphere price have not yet been corroborated by a company statement, a securities filing, or a named source on either side of the deal. The Anysphere acquisition, in particular, is reported in a single wire item and should be treated as a credible but unconfirmed claim until SpaceX, xAI, or Anysphere publish a statement. Readers watching the data should also note that headline net-worth figures are reported, not adjudicated — they move with the inputs and are not the same as spendable cash.

What the day does establish, beyond dispute, is the order of magnitude: a single trading session in which one private company's re-rating added more to one individual's paper wealth than most sovereign budgets spend in a year, while the same individual was reported to be preparing a $60bn acquisition of one of the most strategically placed developer-tools companies of the AI cycle. The story of 16 June 2026 is less about the numbers than about who now has the equity currency to write them.

This article drew on a single Telegram-distributed wire feed for its core claims. Monexus flags that the headline net-worth figure, the $2.8trn SpaceX valuation, and the $60bn Anysphere price are reported but unconfirmed by primary-issuer statements at the time of publication.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph