SpaceX IPO tops $85.7bn as underwriters fully exercise greenshoe, leaving retail with a thin slice

SpaceX's listing has ballooned to $85.7bn after underwriters maxed out their option, but retail investors are finding allocations scarce and the hold-versus-sell debate already underway.

SpaceX's market debut closed on 15 June 2026 with the underwriter syndicate fully exercising its overallotment option, pushing total proceeds to $85.7bn and cementing the listing as one of the largest in recent memory. The greenshoe exercise, reported by CNBC at 16:23 UTC and corroborated by TechCrunch at 16:35 UTC the same day, signals the deal priced into an order book with more demand than the base deal could absorb. The headline number, however, masks a more familiar complaint: the people who most wanted in were the ones who got the least.

What is unfolding is a textbook case of an IPO sized for institutions and offered to retail as an afterthought. Allocations to individual investors have been thin, secondary-market access has been uneven, and the hold-versus-sell decision is being made on day one rather than over a multi-year horizon. The structural question is no longer whether the deal was successful — it plainly was — but who the success was structured for.

A $85.7bn deal and a fractional slice for the public

The greenshoe — the contractual right granted to underwriters to sell up to 15% more shares than the base deal — is normally a sign of a hot issue. When the option is fully exercised, as it was here, it usually means the book was oversubscribed and the lead managers wanted to deliver more paper to demand than the original filing allowed. The result, per CNBC and TechCrunch, is a final raise of $85.7bn — a figure that puts the listing in rarefied territory.

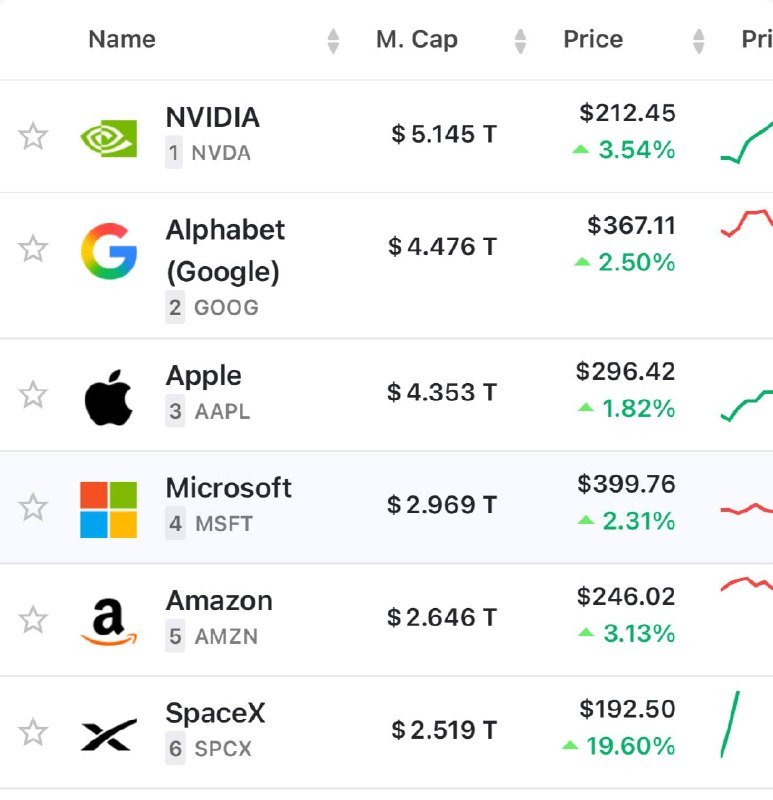

CryptoBriefing's 18:15 UTC wire the same day noted SpaceX shares had surged 16% from the issue price, pushing the company's implied valuation close to Amazon's. The two datapoints together — a fully exercised greenshoe and a double-digit debut move — describe a market that, at the margin, would have bought more shares at the IPO price than it was offered. Retail did not, on the whole, capture that premium.

The allocation problem

Retail participation in marquee IPOs has been a recurring flashpoint in US equity markets for several years. The mechanics are well known: institutional accounts are allocated the bulk of the float, retail brokers receive a residual, and the customers who wanted the deal most are told to wait for the secondary market — at a higher price. The thread context from 15 June 16:35 UTC makes the same observation directly: retail investors who did receive shares are split between selling into the debut and holding for the long term, and those who did not receive any are now weighing whether to chase a stock already up sharply.

That this is happening with SpaceX is significant. The company is not a speculative biotech with no revenue; it is a profitable, cash-generative operator with a contracted backlog across launch services, Starlink broadband, and government work. The fact that retail demand still outstripped supply at the offering price says something about the depth of the order book — and about the fact that the depth was captured upstream, by the institutions that commit capital before pricing.

Structural frame: who the IPO is for

An IPO is a sale, and the seller chooses the buyer mix. Lead underwriters reward the accounts that provide research coverage, that commit to hold shares through lock-ups, and that bring repeat flow. The economics of the deal are designed to be captured by those counterparties, not by the public. That is not corruption; it is how the system is built. Coverage that frames the greenshoe as a market verdict on the company — bullish, oversubscribed, validated — is correct as far as it goes, but it skips the question the deal itself raises: when an issuer is large enough and desirable enough to clear the market many times over, why is the offering structured the way it is?

The honest answer is that the issuer and its bankers optimised for price stability and aftermarket support, and institutional holders are better at providing both. Retail gets the news, the secondary market, and the right to decide whether the post-debut move is a sale or a hold.

Stakes and what to watch

The near-term question is the lock-up calendar. When insider and pre-IPO holder restrictions begin to roll off, the share register will broaden, the float will grow, and the price-discovery process that was compressed into the first trading session will replay over a longer window. Whether the stock holds the premium implied by the debut depends on the usual variables: execution against the existing backlog, growth in Starlink subscribers, and any new capital-intensive line of business the company decides to fund with the $85.7bn it has just raised.

The broader question is whether the pattern repeats. Each marquee listing of the last several years has allocated a thinner share to retail and a fatter one to the institutions that arrive first. The SpaceX deal is not an outlier; it is the latest datapoint in a trend. Watch the next one.

This publication framed the deal through its allocation mechanics, not its headline proceeds, on the view that the size of the raise tells you what the market thought of the company, and the way it was distributed tells you who the market thought the shares were for.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://www.cnbc.com/2026/06/15/spacex-ipo-spcx-greenshoe-overallotment.html?__source=androidappshare

- https://t.me/CryptoBriefing

- https://t.me/CryptoBriefing