Bitcoin as corporate treasury: Illinois pulls the tax lever while Strategy counts its coins

On the same June afternoon the Federal Reserve held rates steady and Illinois enacted the most punitive crypto transaction tax in the United States, Strategy declared its Bitcoin reserve could underwrite 32 years of dividends — three signals that say the same thing about how seriously this asset class has to be taken by tax authorities, monetary policymakers, and bond investors alike.

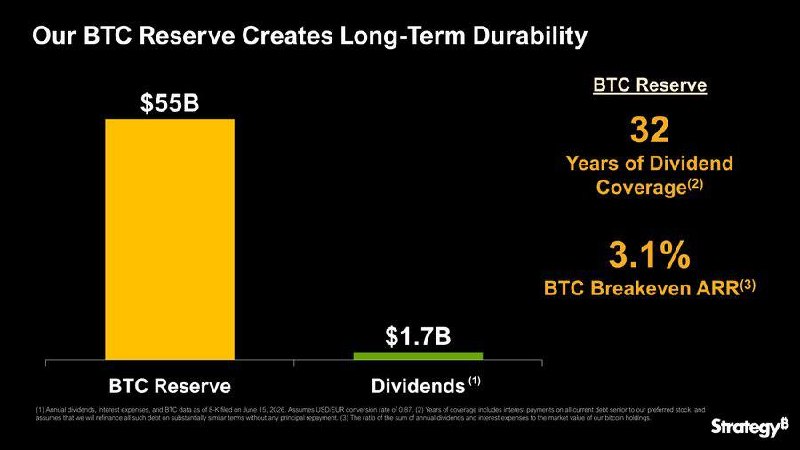

Strategy, the corporate treasury vehicle formerly known as MicroStrategy, said on 17 June 2026 at 21:20 UTC that its Bitcoin holdings are sufficient to cover dividend obligations for the next 32 years, per a Cointelegraph wire. The framing is audacious on its face. It is also the most explicit admission yet from a public company that Bitcoin, once a treasury experiment, is being treated internally as a yield-bearing reserve asset.

Three things happened on Tuesday that, taken together, tell one story. The Federal Reserve held its policy rate unchanged. Illinois enacted a 0.2 percent transaction tax on Bitcoin and crypto trades beginning in 2027 — the most punitive digital-asset levy any US state has put on the books, critics told Cointelegraph. And Strategy declared that its coin stack could underwrite three decades of dividends. None of these moves is novel in isolation. Read in sequence, they sketch a closing window.

A new kind of collateral

For most of the post-2020 era, corporate Bitcoin holdings were framed as a bet — a sideways hedge against dollar debasement, a thumb in the eye of the bond market, an idiosyncrasy of one CEO's worldview. Strategy has now re-framed the position as collateral with a duration attached to it. Thirty-two years of dividend coverage is a number only a treasurer would care to publish. It is also a number that credit rating agencies, auditors, and dividend-focused income investors will be obliged to read.

The claim is not that Bitcoin generates yield. Strategy is not running a lending desk and earning interest on its coins. The claim is structural: that the realised appreciation of the reserve, measured against the firm's contractual payout schedule, mathematically covers the forward liability. Whether the math holds depends entirely on a price assumption the company does not disclose in the wire. That is the part of the story that should make an income-fund manager pause.

Illinois draws a line

State-level crypto taxation has been a slow drift, not a single event. Illinois's move is significant because of the rate, the breadth of the base, and the timing. A 0.2 percent levy on every transaction is small enough to feel like a nuisance tax on a retail user and large enough to function as a friction tax on a high-frequency market-maker. Critics quoted by Cointelegraph called it the most punitive digital-asset tax in the country. That framing is contestable — New York's BitLicense regime imposes heavier compliance costs, even if not a clean per-transaction levy — but the directional signal is clear: states have decided that crypto volume is a taxable event worth their political attention.

The structural consequence is not a flight of capital from Chicago. It is a fragmentation of the US crypto market along state lines, with every serious venue now carrying a compliance matrix keyed to the seat of its largest liquidity providers. That is the kind of friction that pushes volume offshore or onto decentralised rails — neither outcome being what state revenue estimators assumed when they ran the numbers.

The Fed's silence is the signal

The Federal Reserve's decision on 17 June at 18:00 UTC to hold interest rates unchanged was, in itself, unremarkable. The signal is in the timing. A 32-year dividend-coverage claim is a duration call. A transaction tax on Bitcoin is a policy signal that the asset class is permanent enough to regulate. Both make most sense in a regime where the cost of holding dollars is not moving. By declining to cut, the Fed has implicitly endorsed the conditions under which corporate treasuries and state tax authorities can price Bitcoin as a long-duration instrument rather than a short-term speculative asset.

This is the part of the story the wire coverage understates. The conventional reading — that the Fed held because inflation is sticky — is fine as far as it goes. The deeper reading is that the Fed no longer needs to lean against crypto-adjacent balance sheets the way it did in 2022. Banks are not the dominant on-ramps any more. The exposure has migrated to corporates, exchange-traded products, and now state tax bases. That is a different problem, and it requires a different policy posture.

What we are actually watching

The corporate treasury movement, the state-level taxation push, and the steady hand at the Fed are not three separate stories. They are three registers of the same argument: that Bitcoin has crossed the line from speculative asset to structural component of the financial system, and the institutions that ignored it for a decade are now pricing it into their spreadsheets. Strategy's 32-year claim is the most aggressive articulation of that thesis yet published by a public company. Illinois's tax is the most explicit admission from a US state that the volume is real. The Fed's hold is the tacit acknowledgment that the macro frame can accommodate both.

The counter-narrative is straightforward. Strategy's claim rests on a price assumption that the wire does not detail, and corporate-treasury math of this kind has a long historical record of failing quietly when the underlying asset's volatility regime changes. Illinois's tax may simply drive volume to better-regulated offshore venues and produce less revenue than projected. The Fed's hold could be revised sharply at the next meeting if labour-market data softens. None of these scenarios is a refutation of the structural thesis; all of them are reminders that the structural thesis is being run as an experiment on live capital.

What remains genuinely uncertain is whether the convergence will hold. If a single major Strategy capital raise lands badly, or if Illinois's tax drives a measurable migration of volume to non-US venues within two quarters of the 2027 effective date, the policy and corporate framing will revisit the question of whether Bitcoin is being treated as a reserve asset because it behaves like one, or because the institutions engaging with it have decided, for reasons of their own, that it must.

This publication read the three wires as a single signal — that crypto is being absorbed into the institutional balance sheet at a pace the policy debate has not yet caught up with. The corporate treasury, the state tax collector, and the central bank are now arguing about the same object. That is the news.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph