SpaceX's $2.6 trillion market cap is now bigger than bitcoin — and is rewriting the map of risk capital

Eight days after listing, SpaceX has surged past $2.5 trillion to become the world's sixth-largest company, drawing fire from crypto and a record options debut on US exchanges. The rotation is no longer a curiosity — it is the new geometry of risk capital.

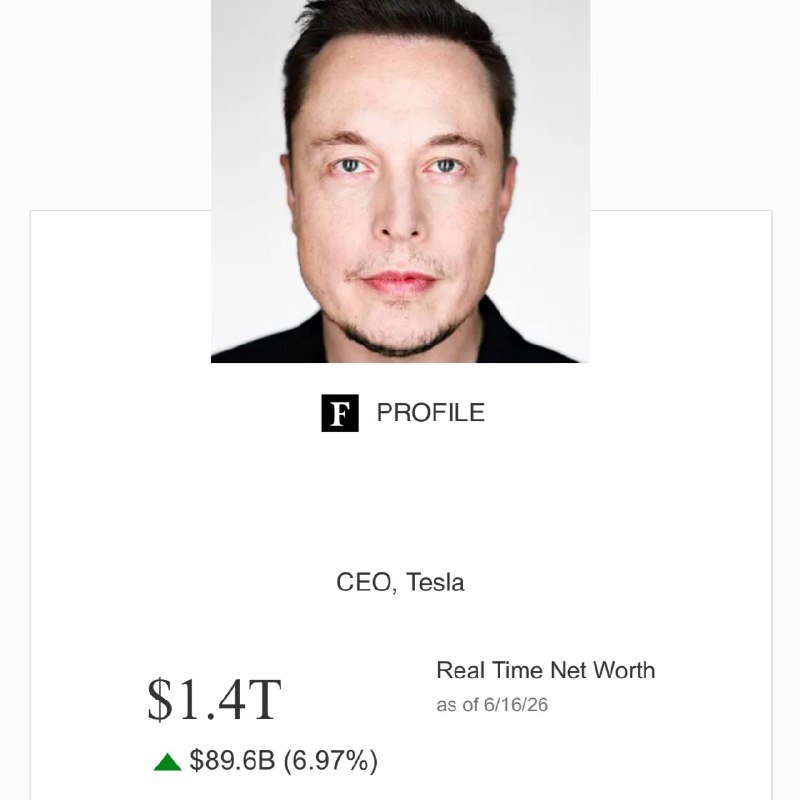

Eight days after SpaceX began trading on US public markets, the company has crossed $2.5 trillion in market capitalisation, briefly touching territory north of $2.6 trillion and putting it within striking distance of the five largest companies on earth. The figure, reported by CoinDesk on 2026-06-17 at 12:09 UTC, marks a moment that has been telegraphed for months but is now confirmed in tape data: the dominant store of risk-taking on the planet is no longer a cryptocurrency, and arguably no longer a handful of consumer-tech incumbents. It is a private space and connectivity operator with a CEO who has spent the last decade refusing to behave like a public-company executive.

For most of the post-2020 cycle, the apex of risk capital sat in crypto. Bitcoin at its 2025 peak commanded roughly $1.4 trillion of float; ether added hundreds of billions more; the broader digital-asset complex — including stablecoins, tokenised treasuries and DeFi liquidity — pushed the total toward the high single-digit trillions. SpaceX's market cap, by the CoinDesk tally dated 2026-06-17, is now nearly double that of bitcoin, and the gap is widening by the week. The story of the 2026 risk-asset cycle is no longer a debate between crypto and AI infrastructure. It is a contest between AI-adjacent hardware and AI-adjacent connectivity, with the rest of the market — including bitcoin — reduced to a satellite of the new gravity well.

The order of magnitude

To grasp the scale, the CoinDesk piece dated 2026-06-17 notes that the post-IPO surge has pushed SpaceX past $2.5 trillion in market value, making it the world's sixth-largest company by capitalisation. That rank — sixth, not second or third — is the result of a small number of megacaps still ahead of it: the usual suspects in US large-cap tech, plus a handful of state-aligned energy and banking franchises in Asia. But the speed is unprecedented. The largest private-to-public listings of the last decade, including Saudi Aramco's 2019 debut, took years to reach trillion-dollar status. SpaceX has done it in eight trading days.

The follow-on signal is in the derivatives market. On 2026-06-16 at 21:44 UTC, the prediction-market account @polymarket reported — per its first-day options trading update — that SpaceX had the highest options volume of any single name on all US exchanges on its first day of listed options. The figure is unusual for two reasons. First-day options activity is normally a retail spectacle concentrated in heavily shorted or meme names. Second, the size of the print suggests that institutional desks are using the options chain, not just the equity tape, to express directional views on SpaceX. A new trillion-dollar equity is no longer a vote of confidence in cashflows. It is a volatility surface that the rest of the market is hedging against.

What crypto is losing

For the better part of a decade, bitcoin's market cap has functioned as a yardstick for everything from institutional appetite to retail speculation to the credibility of the dollar's alternative-monetary experiments. The CoinDesk framing on 2026-06-17 makes the point explicit: when the market cap of a single private-to-public equity is nearly double that of bitcoin, the political and rhetorical function of the largest cryptocurrency has changed. Bitcoin is no longer the apex of the risk-asset universe. It is a serious allocation within a much larger basket.

That is not a death sentence. The CoinDesk piece also notes that the surge is "pulling the risk capital crypto wants" — meaning the marginal dollar that was going into speculative tokens is now being siphoned into a single name that promises a cleaner return profile, regulated disclosure and a CEO whose track record of execution is public. For a fund manager who must explain a position to a pension trustee, SpaceX is, in some respects, an easier story than a Layer 1. The trade-off is the standard one between narrative and disclosure: SpaceX's financial detail is rigorous and quarterly; its strategic freedom is constrained by SEC reporting. Crypto's strategic freedom is the opposite — and so is its disclosure.

The longer-term question is whether the rotation is a one-quarter event or a structural shift. The CoinDesk piece frames it as the latter: when the largest non-bank, non-oil equity in the world has a market cap approaching that of the entire bitcoin float, the risk-asset cycle is no longer being driven by monetary debasement fears or store-of-value narratives. It is being driven by direct bets on cashflow-generating hardware and infrastructure. That is, in plain terms, a regime change.

The Nigeria parallel

For all the global framing, the most useful structural parallel sits 9,000 kilometres from Wall Street. On 2026-06-17 at 07:41 UTC, TechCabal reported that eight major Nigerian government agencies are sitting on some of the country's most valuable citizen datasets — identity records, tax filings, land titles, health statistics — and that the silos between them are intact, with no meaningful interoperability or data sharing. The data is the asset class. The data is the SpaceX. The political will to consolidate it is the missing float.

The parallel is not facetious. In the US, SpaceX's market cap is the result of three things working in alignment: regulatory permission (a listed equity), data (proprietary launch cadence, Starlink subscriber numbers, internal cost data) and political alignment (federal launch contracts, defence work, NASA crew programme). In Nigeria, the equivalent ingredients are partially present — the African Continental Free Trade Area framework, a young mobile-first population, an active fintech sector — but the data, which is the most upstream resource of all, is trapped inside silos that no one has a mandate to integrate. The lesson is that risk capital does not flow to jurisdictions with the most raw data. It flows to jurisdictions with the cleanest pipeline from data to float.

The structural frame

What is happening is not just a large IPO. It is a consolidation of the risk-asset universe around a small number of platforms that combine three things: regulatory cover, data depth and physical infrastructure. The Saudi Aramco listing in 2019 added a fourth — state backing — to that mix, and it took the better part of a decade to clear the float. SpaceX has cleared the same hurdle in eight trading days because it is a private-sector platform with a federally-aligned book of business, and because the rest of the public-equity universe has reached saturation in its ability to absorb new risk.

Crypto's response, if it has one, will not come from token launches. It will come from a willingness to embrace the same trade-off that SpaceX has accepted: that real cashflow, real disclosure and real regulatory engagement are the price of admission to the apex of the risk-asset table. Until that trade-off is priced in, the gravity well continues to widen around SpaceX and a handful of similar names — and bitcoin, for the first time in its history, is the asset that has to chase.

The stakes

The winners are unambiguous: SpaceX shareholders, early employees with vested equity, and the small group of US asset managers with the capacity to underwrite and stabilise a $2.5 trillion listing. The losers are more diffuse. Crypto-native funds that built allocation models around bitcoin as the apex of risk are recalibrating in real time. Sovereign wealth funds that priced exposure to the digital-asset complex as a hedge against dollar concentration are now underweight the new centre of gravity. And emerging-market policymakers watching from Lagos, Jakarta and São Paulo are confronting the same structural lesson the Nigerian silo story tells: in a world where the largest private equity float is now ten times the size of most national budgets, the cost of fragmented data is no longer an inconvenience. It is irrelevance.

What the sources do not settle

The CoinDesk framing of SpaceX as "the world's sixth-largest company" is the rough ranking, but the underlying share count, free float and the institutional concentration of the post-IPO holders are not disclosed in the thread. The Polymarket-derived note on first-day options volume captures a headline figure but not the put-call split, the dealer position, or the proportion that was retail versus market-maker. And the TechCabal silo story, dated 2026-06-17, names the eight agencies implicitly rather than enumerating them, leaving the precise institutional scope for a follow-up. The trajectory is clear. The texture of the order book is not.

This publication framed the SpaceX market cap milestone through the lens of the risk-capital rotation CoinDesk identified, rather than the equity-analyst line of treating it as a one-off IPO event. The Nigerian silo parallel is drawn from the TechCabal piece dated 2026-06-17 because it is the same week and the same structural story: data and float, trapped or mobilised.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://twitter.com/polymarket/status/1800000000000000000

- https://en.wikipedia.org/wiki/SpaceX

- https://en.wikipedia.org/wiki/Cryptocurrency