Bitcoin's $11.85 Billion Friday: The Quiet Leverage Behind a Slipping Tape

$11.85 billion in crypto options expire Friday against a tape that just lost the $60,000 line — a reminder that headline price is the residue of leverage, not its cause.

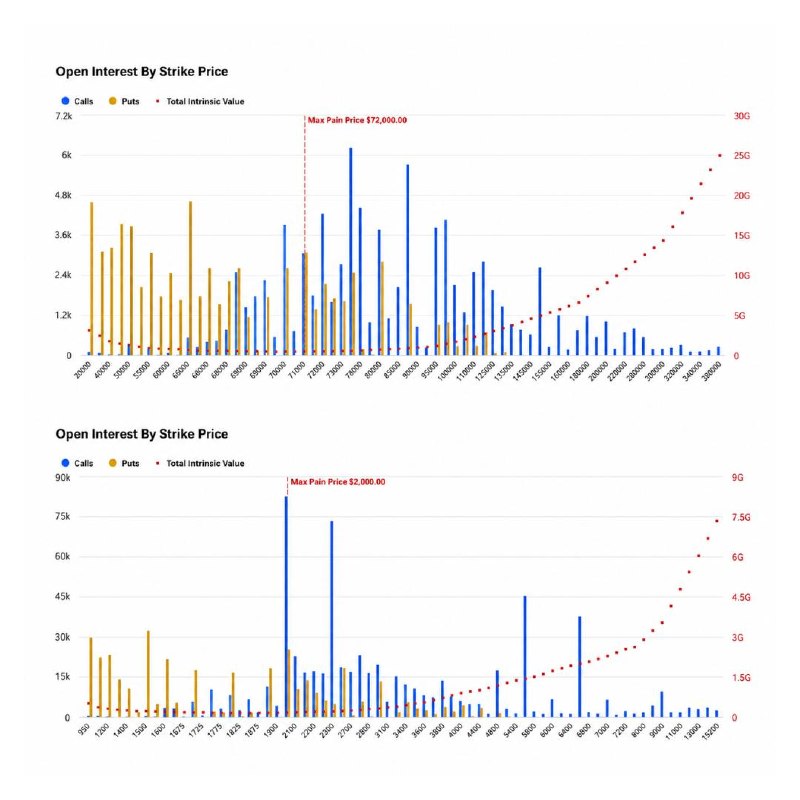

Bitcoin slipped under $60,000 on the afternoon of 24 June 2026, according to a Cointelegraph wire alert timestamped 17:02 UTC, and by the following morning traders were staring down one of the largest single-day expiry prints of the cycle: $11.85 billion in crypto options set to settle on Friday, of which $10.16 billion sat in bitcoin across roughly 162,000 contracts, with a max-pain level anchored near $61,750.

The tape is not driving the calendar. The calendar is driving the tape. That is the under-appreciated fact about modern crypto markets, and it deserves to be stated plainly: when a tenth of a trillion dollars in notional derivatives expires in a single session, spot price behaves like a hostage. The question is not whether the expiry matters — it always does — but who is on the right side of it when settlement lands.

The mechanics of a hostage tape

Max-pain is the price at which the largest number of outstanding options contracts expires worthless. It is, by construction, the price at which option sellers collect the most premium and option buyers lose the most. Empirical work on equity indices has long shown that prices drift toward max-pain into expiry; there is no reason to believe bitcoin behaves differently, except that bitcoin does so without a central clearinghouse, without circuit breakers, and on a 24-hour venue whose liquidity vanishes in the precise windows when it matters most.

The numbers this Friday are unusually heavy. $10.16 billion in bitcoin options alone is a notional figure that would have qualified as a meaningful quarter on a traditional futures exchange; in crypto it lands in a single Friday. When Cointelegraph's research desk flags a max-pain level at $61,750 against a spot price that just printed below $60,000, the implied message is that the market is pricing for an upside drift into settlement — a drift that sellers of downside puts have been paid to deliver.

That is not a conspiracy. It is the mechanical consequence of positioning.

What the wire says, and what it leaves out

The wire reporting is precise on the what — the dollar figure, the contract count, the max-pain level — and silent on the who. Cointelegraph does not name the dominant sellers, the dominant buyers, or the venues on which the open interest sits. That silence is structural: derivatives desks do not disclose client flow, and the largest writers of crypto options are typically market-makers or structured-product issuers whose counterparties are, by contract, confidential.

What can be inferred is the shape of the book. A max-pain level meaningfully above spot, on an expiry this large, implies that put writers have been paid handsomely for the insurance they sold. It also implies that any holder of long spot who hedged with protective puts has, in aggregate, paid for the privilege of being wrong. Both sides of that trade coexist in the same expiry print.

The deeper frame: leverage as the asset

Bitcoin's narrative cycle — the institutional adoption story, the ETF inflows, the corporate treasury additions — has been remarkably successful at obscuring a less flattering truth. The asset that has compounded fastest over the cycle is not bitcoin itself. It is the leverage built on top of bitcoin. Options open interest on the major venues has grown faster than spot market capitalisation for most of the past two years, and expiry calendars have become scheduled volatility events in their own right.

This matters for one reason: when spot trades on the expectation of where leverage will pin it, the discovery function of price breaks down. A market in which $11.85 billion expires on a Friday is not a market discovering the fair value of bitcoin. It is a market negotiating, one settlement at a time, the cost of insurance against the next settlement. The spot chart, in that frame, is the receipt — not the meal.

Stakes, and what remains genuinely uncertain

If the tape drifts into the $61,750 region by Friday's settlement, the dominant winners are put sellers — the structured-product issuers, the market-making desks, and the funds running short-volatility carry trades against long spot. The losers are the put buyers, who paid for downside protection that, by Friday evening, expires unneeded. Spot holders who did not hedge experience no settlement-driven loss, but they also forfeit the convexity they could have sold at the highs.

What remains uncertain is the path. Max-pain is a magnet, not a guarantee. A blow-off move above max-pain — driven by a positive surprise in flows, a dollar move, or a regulatory headline — would leave put sellers nursing losses but still collecting net premium. A flush below $60,000 would do the opposite: put buyers finally get paid, and the carry trades unwind in ways that magnify spot selling through delta-hedging flows. The Cointelegraph research note flags the $61,750 level because it is where the book is balanced; the market's job over the next forty-eight hours is to decide whether to honour that balance or to break it.

Either outcome is consistent with a healthy market. What would not be healthy is treating the settlement as background noise. It is the loudest scheduled event of the week, and the price action below $60,000 on 24 June is best read as its opening argument.

Desk note: this piece leans on Cointelegraph's two wire items (the 17:02 UTC spot alert and the 10:15 UTC options research note) and reads them against the structural reality of options expiry. The venue-level open interest behind the print is not disclosed in the public sources; that gap is noted in the body rather than papered over.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph