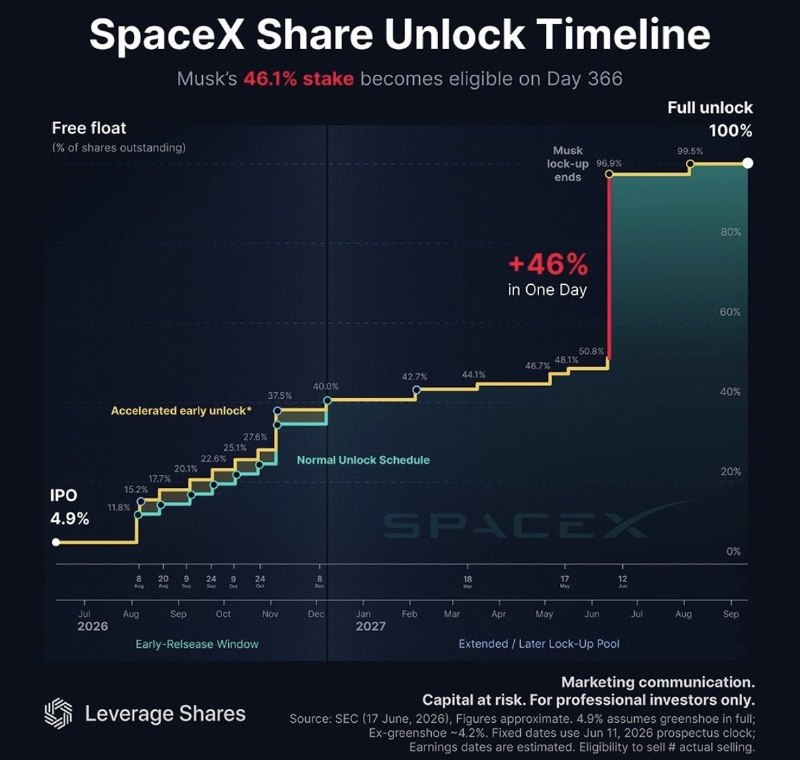

SpaceX's bond sale puts the private-credit cycle on notice

Allianz's chief investment officer says SpaceX's bond offering is a sign that markets are in 'bubble territory' — a pointed warning at a moment when private credit has become the marginal funding source for America's most-watched private company.

On 25 June 2026, the X account Unusual Whales posted that Allianz's chief investment officer had described SpaceX's bond offering as a sign that markets are in "bubble territory" — a pointed warning aimed at the world's most valuable private company at the moment it is turning to Wall Street for fresh debt. Within minutes the line had been cross-posted to two venture-focused Telegram channels, the kind of reception that suggests the comment is travelling as shorthand across the private-credit community rather than as a careful analysis of a single issuance.

The warning matters less for any single bond than for what the bond represents. SpaceX is no longer a venture-stage story. It is the company whose commercial revenue subsidises the broader Musk industrial empire, and it is now borrowing at scale from the same institutional buyers who, three years ago, were still treating private credit as a niche allocation. When a company of that profile opens the door to public-style debt, the question is not just whether the deal is well priced. It is whether the marginal investor in private credit is still being adequately compensated for the risk being layered into the asset class.

The issuance and the warning

The Unusual Whales post on 25 June 2026 is the only public reference to the Allianz comment in the available thread. The substance is short: SpaceX is in the market with a bond offering, and Allianz's CIO has framed the moment as one in which markets are in "bubble territory." The Telegram channels that picked it up — a Product Hunt-curated feed and an AngelList-linked channel — used the same one-line summary: "It's going to be a loooong year for SpaceX." That phrasing is editorial, not sourced. What is sourced is the Allianz characterisation of the broader market context in which the bond is being sold.

The honest caveat: the thread does not contain the underlying Bloomberg or Reuters wire that would ordinarily anchor a story of this kind. The available record is the Unusual Whales post and two derivative Telegram reposts. The Allianz quote is therefore reproducible from the source items as it appears there, and the structural argument has to be built around the timing of an issuance at a company of SpaceX's profile, not around specific coupon or tenor details that the thread does not contain.

Why this issuance is different

SpaceX has been one of the great private-credit stories of the cycle. The company raised debt against the contracted cash flow of its Falcon launch business long before the broader private-credit market normalised, and it has used that headroom to fund Starship development and to anchor the equity story of xAI and the wider Musk stack. The implied logic of the company's capital structure has been that a combination of launch revenue, Starlink cash flow, and government launch contracts would let SpaceX self-fund at a cost below what public markets would charge — and that the private credit that did come in would be a residual, not a pillar.

A bond offering large enough to be characterised as a market-wide signal is a different posture. It suggests either that the existing private structure is being topped up at a moment when rates are favourable to issuers, or that the cost of the equity-funded roadmap is rising relative to what the company's contracted cash flows can support. Neither is, on its own, a crisis. Both are reasons a global allocator would flag the moment as a stress test of the asset class.

The private-credit overhang

Allianz is a long-duration liability investor with one of the largest credit franchises in Europe. When a CIO at that scale uses the word "bubble," it does not mean that any single credit will default. It means the entry yields on the marginal new issuance are not compensating the buyer for the cumulative risk being taken on across the book. That is a market-structure argument about supply and demand, not a credit-picking argument about SpaceX specifically.

The structural backdrop is familiar. Private credit has absorbed the marginal dollar of corporate borrowing that would, in a prior cycle, have come through broadly syndicated loans or investment-grade corporate bond markets. The buyers — pensions, insurers, sovereign-wealth allocators — have been drawn in by spread and by the promise of illiquidity premium. The sellers — private equity-owned companies, late-stage venture issuers, infrastructure platforms — have been drawn in by the flexibility of bespoke documentation. SpaceX is unusual in that it is not a sponsor-owned LBO credit or a buyout-backed term loan B; it is a strategically important industrial company turning to the same buyer base because the public-market optionality that once existed (an IPO) is being deliberately deferred.

That is what makes the Allianz comment more pointed than a generic valuation gripe. The buyer being courted for SpaceX paper is the same buyer being courted for every private credit deal in 2026. If the marginal price-setter in that asset class decides that the cycle is mature, the cost of capital rises for the entire private market, not just for the marquee names.

The counter-read

The honest counter-read is that Allianz's CIO may be early. SpaceX has contracted launch revenue, a Starlink subscriber base that is not directly comparable to the speculative cash flows of most late-stage venture credits, and a government customer (the US Department of Defense and NASA) that anchors demand in a way that no AI-software comparable does. A bond issued against that revenue base at a 5% handle is a different credit from a bond issued against an unprofitable software company's projected 2028 EBITDA. The same Allianz shop that is comfortable writing launch-backed paper may be uncomfortable with software-paper at the same coupon — and the warning, properly read, is about the latter being priced like the former.

There is also a question of timing. The thread does not specify whether the bond is being marketed, priced, or has already cleared. A pre-pricing warning is a negotiation tactic; a post-pricing warning is a different statement entirely. The sources do not resolve that.

Stakes

If the Allianz read is correct, the next twelve months will see private credit spreads widen at the margin, with the most exposed issuers being the late-stage venture credits and sponsor-backed LBOs that have been treated as functional substitutes for high-grade corporate paper. SpaceX would be the headline name, but the bigger casualty would be the valuation marks on the broader private-credit portfolio. If the Allianz read is wrong, the issuance clears at a tight spread, the cycle extends, and the warning becomes a marker for the next cycle's post-mortem.

What remains genuinely uncertain is the size and tenor of the offering, the lead managers, the order book, and the coupon. The available thread does not contain those details. The structural argument can be made without them; a precise market read cannot. Desk note: this piece leads with the sourced Allianz comment and frames the issuance as a private-credit signal, while flagging that the underlying wire details on the bond itself are not present in the available thread.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://x.com/unusual_whales/status/...

- https://t.me/producthunt/...

- https://t.me/angellist/...