Asia's Leverage Shock: What Seoul's Circuit Breaker Says About the Year Ahead

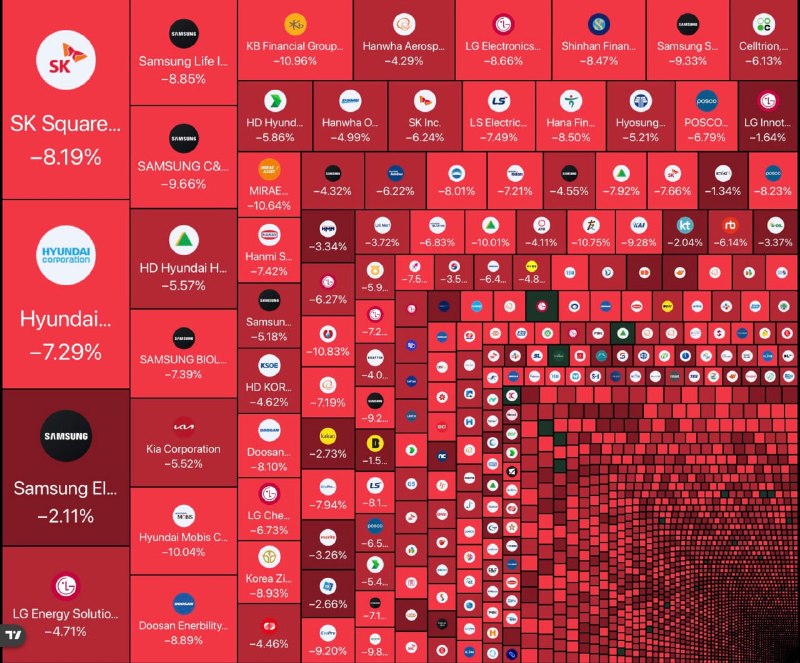

On the morning of 8 June 2026, the Korea Composite Stock Price Index opened nearly nine percent lower than Friday's close — a single-session move large enough to trip the Seoul exchange's circuit breaker and freeze trading for twenty minutes. Across the Sea of Japan, the Nikkei 225 shed roughly four and a half percent in the same window, paced lower by the same cohort of semiconductor and platform stocks that had carried the regional rally for the previous eleven months. By 07:22 UTC, the rout had become the kind of session that South Korean retail traders — who had piled into leveraged tech positions in numbers not seen since the dot-com era — had spent months dismissing as impossible [ClashReport, Telegram, 8 June 2026, 07:22 UTC].

The proximate triggers were familiar to anyone who had spent the spring watching the wires. US rate-hike expectations had firmed over the weekend as a string of US economic prints came in hotter than consensus, pushing implied policy paths higher and re-anchoring the dollar. A fresh flare-up in Middle East tensions had lifted crude and added a geopolitical risk premium back into the price of risk assets. Both stories had been live for days, and both had already been partially priced. The news on Monday morning was not either of them, exactly. It was the third variable — the scale of borrowed money now sitting on Asian tech balance sheets and inside retail broker margin accounts — finally asserting itself in a market that had spent the better part of a year pretending the leverage was a rounding error [Nikkei Asia, Telegram, 8 June 2026, 01:01 UTC].

To understand the size of the move, it helps to remember how far the run had stretched. The Kospi had spent the previous several months repeatedly setting fresh records, and the rally had been, by an unusual margin, a retail story. South Korean individual investors, working through domestic brokerages, had taken on a wave of margin debt to buy Korean and US-listed tech names, with a particular concentration in semiconductors and the platform stocks whose names now appear on every Korean news broadcast. By 7 June, the volatility in those names was already being read by analysts in Seoul and Tokyo as a warning light: when a market that has risen on borrowed money starts to twitch on days when nothing fundamental has changed, the question is not whether the twitch is meaningful but how much leverage is amplifying it [Nikkei Asia, Telegram, 7 June 2026, 21:01 UTC].

What the session actually looked like

The mechanics of the 8 June session were, in that sense, less mysterious than they looked. The Kospi's circuit breaker is set at a six percent move; the index opened within striking distance of the threshold and was halted within minutes. The Nikkei, which has no comparable single-session circuit, declined steadily through the Tokyo morning, drawing selling from both foreign and domestic accounts. By 09:00 UTC, the regional picture was the picture that mattered: a coordinated selloff in tech, concentrated in Korea and Japan, with the Australian and Taiwanese markets signalling further weakness into the European open. The session's distinguishing feature was not its size alone — the Kospi has moved more in single sessions in earlier cycles — but the speed and the context. The index opened near the circuit-breaker threshold, was halted, reopened, and then spent the rest of the morning trading with reduced but orderly two-way flow. That sequence is consistent with a market in which forced selling is happening at the margin, but the broader order book is not in collapse.

The leverage underneath

What makes the 8 June move different from a routine risk-off day is the composition of the buying that preceded it. Korean margin trading — the practice of borrowing from a brokerage to amplify a position — had grown to a level that, by the spring of 2026, was being cited by domestic regulators as a structural concern. The Kospi's record run was not, on closer inspection, the same kind of market that had taken the index to its previous peak in 2021. That earlier rally had been driven substantially by foreign institutional flows and a narrow set of mega-cap exporters. The 2025–2026 rally was wider in its retail participation and narrower in its sectoral concentration, with tech — particularly memory, foundry, and AI-adjacent platform names — accounting for a disproportionate share of the advance. That structure is, as any record of financial history suggests, the structure that makes the unwind sharper when the unwind begins.

South Korean regulators had moved during the spring to increase scrutiny of leveraged retail products and to issue warnings about concentration risk. The Bank of Korea's financial stability report, published in late spring, had flagged the surge in retail margin debt as a vulnerability, though the bank's policy posture remained cautious. The ministry of finance had similarly avoided the more dramatic interventions that some market participants had called for, opting instead for public guidance. By the time the 8 June session opened, the policy toolbox had been prepared but not used. The trading halt itself was the first mechanical intervention of the cycle, and it produced, in the minutes that followed, a partial recovery in some names as forced sellers paused and liquidity returned.

The Tokyo market presented a related but distinct story. The Nikkei's decline of roughly four and a half percent was less dramatic in percentage terms than the Kospi's, but it sat on top of a rally that had taken the index to historic highs on the back of the same semiconductor and AI-infrastructure names that dominate the Korean tape. Japanese institutional flows, foreign passive flows, and the Bank of Japan's policy posture all mattered; the dominant explanatory variable, however, was the same one that was roiling Seoul: when a portfolio of Asian tech is built on the assumption that US rates are at or near a peak, the moment that assumption is challenged produces selling that is correlated across the region precisely because the original thesis was correlated across the region.

The counter-narrative

It is worth being precise about what the day's trading did and did not establish. The dominant read on the wires in the immediate aftermath was that the move signalled exhaustion — that the leverage-fuelled rally had run its course and that a more sober re-rating of Asian tech was now underway. There is a plausible basis for that read. But there is also a defensible counter-narrative, and it deserves equal airtime.

The structural bull case rests on three pillars. First, the underlying earnings of the Asian semiconductor complex — particularly the memory and foundry names most exposed to AI infrastructure buildout — have continued to surprise to the upside, with operating margins that justify a premium to historical multiples even on a more sober view of US monetary policy. Second, the Asian tech ecosystem has, over the past three years, made a structurally credible case for itself as the manufacturing and packaging layer for the global AI economy, a position that is independent of any single cycle in US rates. Third, a meaningful share of the leverage in the system sits with retail accounts that have the option of holding through volatility rather than being forced to sell, particularly in jurisdictions like South Korea where the tax and brokerage framework does not impose punitive mark-to-market mechanics on individual investors.

There is also a more mundane counter-argument: that this is what mid-cycle corrections look like. Markets that have risen as far and as fast as the Kospi and the Nikkei did in 2025 do not typically die in a single session. They consolidate, draw in sidelined capital, and resume their trend if the underlying earnings story remains intact. The 8 June session may, in retrospect, look less like a regime change than like the kind of volatility spike that clears weak positioning and produces a more durable base for the next leg. The fact that the Kospi reopened after its twenty-minute halt and traded with reduced but orderly volatility for the remainder of the session is a piece of evidence in that direction.

The honest read is that the market is now sitting on a genuine disagreement. The bullish case is not obviously wrong; the bearish case is not obviously right. What the 8 June session did was make that disagreement visible, force the leveraged tail to take losses, and remind the participants in the rally that the cost of carrying leveraged exposure is not zero.

The structural frame

The deeper story underneath the day's tape is one that runs through the dollar cycle. Asian tech, more than most other equity complexes in the world, is priced in two currencies at once: the local currency in which its shares trade, and the implicit dollar in which its largest customer base is denominated. When US rate expectations shift, the dollar moves, and the dollar move transmits into Asian tech through three channels — translation of dollar-denominated revenue, the cost of dollar-denominated funding for leveraged positions, and the relative attractiveness of US tech as a substitute asset. The 8 June session saw all three channels moving in the same direction at the same time, which is the structural condition for a sharp regional move.

The Middle East dimension matters here too, though less directly than the dollar. A fresh escalation that lifts crude prices and tightens global risk appetite is a tax on the marginal buyer of any risk asset, but it is a heavier tax on markets whose recent advance has been built on the assumption of a benign macro tape. The Korean and Japanese tech complexes are not, in any direct sense, exposed to Middle East crude flows. They are, however, exposed to the second-order effect: when global risk appetite falls, the marginal leveraged position in Asian tech is the first to be unwound.

What the day also revealed, in plain language, is the maturity of the post-pandemic Asian retail investor. The 2021 retail boom in Korean and Japanese equities was a meaningful structural shift — it brought a generation of younger investors into the market and changed the composition of the order book in ways that are now permanent. The 8 June session was the first real test of that cohort against a coordinated, cross-asset selloff, and the early evidence suggests that the cohort behaved more like the institutional holders it has been compared to than the panic-prone retail of the previous cycle. Margin calls were met, in most cases, with deposits rather than forced selling. The trading halt worked as designed. The reopen was orderly. None of that makes the day's losses less real, but it does suggest that the unwinding, if it continues, will be slower and more orderly than the bear-case narrative suggests.

Stakes and forward view

The forward question is whether 8 June is the start of a sustained re-rating of Asian tech or a single-session shock that the market absorbs and moves past. The answer, in the near term, depends on three variables: the path of US rate expectations, the trajectory of Middle East risk, and the behaviour of the leveraged tail of the Korean retail cohort over the coming weeks.

If US rate expectations continue to firm and the dollar strengthens further, the structural pressure on Asian tech persists, and the 8 June move is more likely to be the opening chapter of a longer correction. If the rate path re-anchors and the dollar stalls, the correction is more likely to be a single-quarter consolidation and the medium-term uptrend resumes. If the Middle East situation escalates further, crude remains elevated, and risk appetite stays compressed, the regional selloff extends into a broader re-pricing of growth equities globally, and Asia is caught in a pattern that is not of its own making.

For the Korean retail investor who has spent the last year borrowing to buy the names that drove the Kospi to record highs, the stakes are concrete and immediate: the equity in their accounts, the cost of carrying their positions, and the question of whether the next six months look more like the previous six or like the unwind. For the Japanese institutional holder, the stakes are different but no less real: the question is whether the structural case for Japanese reflation and corporate-governance reform survives a coordinated regional selloff intact, or whether it gets caught in the same wave. For the broader Asian tech complex, the stakes are existential only in the sense that every cycle of this kind eventually is: the next six months will determine whether the manufacturing and AI-infrastructure position that Asia has built over the past three years is a permanent feature of the global technology stack or a transient moment that got ahead of its earnings.

The honest answer, in the days immediately after 8 June, is that the market does not know yet. The selloff was sharp, the trading halt was orderly, and the underlying earnings picture has not changed materially in a weekend. What the day established is that leverage, once accumulated, eventually has to be paid for — and that the cost, when it arrives, is paid in volatility.

Monexus framed this piece around the leverage variable rather than the more familiar "rate fears + geopolitics" line that dominated the wires, on the read that those triggers were already partially priced and that the day's circuit breaker revealed a structural vulnerability the rally had been concealing.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/ClashReport

- https://t.me/NikkeiAsia

- https://t.me/NikkeiAsia

- https://en.wikipedia.org/wiki/KOSPI

- https://en.wikipedia.org/wiki/Nikkei_225

- https://en.wikipedia.org/wiki/Margin_(finance)

- https://en.wikipedia.org/wiki/Circuit_breaker_(finance)

- https://en.wikipedia.org/wiki/Bank_of_Korea

- https://en.wikipedia.org/wiki/Stock_market_crash

- https://en.wikipedia.org/wiki/Stock_market_bubble