BYD's 80% China EV forecast lands as exports jump 19% in May

Shenzhen-based BYD said on 9 June 2026 that it expects roughly 80% of new passenger-vehicle sales in China to be electric in the near term, a forecast that lands the same week Beijing's customs administration reported May exports jumped more than 19% year on year, beating forecasts and reinforcing the view that overseas markets are doing the heavy lifting as domestic demand cools.

Taken together, the two data points sketch an industry at a hinge moment. The Chinese car market is, by most readings, approaching saturation for first-time EV buyers. Growth from here will be won abroad, in places where the average new car still runs on petrol and where Chinese manufacturers now price below the legacy incumbents.

BYD's bet on an electrified domestic market

BYD's projection, reported on 9 June 2026, is unusual less for the headline number than for the source. The company is the country's largest new-energy vehicle maker by volume, and its executives have been among the most aggressive in forecasting an early end to the internal-combustion era inside China. The 80% figure is presented as a near-term steady state, not a 2035 aspiration.

Two things give the forecast weight. First, BYD's own product mix has already tilted overwhelmingly toward battery-electric and plug-in hybrid models, so the company is partly describing its own sales funnel. Second, Chinese battery and component supply — cathode material, lithium iron phosphate cells, traction motors, power electronics — has reached a scale and unit cost that legacy foreign automakers still cannot match at volume, which is the structural reason a domestic EV share of 80% is plausible even as growth flattens.

The qualifier the company itself attaches is the softening of total Chinese demand. Analysts cited in the same coverage anticipate domestic appetite to taper further, which is precisely why the export number released on 9 June 2026 — a year-on-year jump of more than 19% in May, with AI-related demand singled out as a driver — matters for the car sector as well. A Chinese economy that is exporting more is also a Chinese economy that is shipping more cars, more batteries, and more of the components that go into both.

The export tailwind

The 19% May export print, flagged on 9 June 2026, was framed by market watchers as an AI-driven story. The more useful way to read it, for the vehicle sector, is that Chinese industrial capacity is finding buyers abroad at a moment when the home market is harder to penetrate. That is the same dynamic that has pushed Chinese solar manufacturers, battery makers, and now auto brands into Latin America, Southeast Asia, the Middle East, and parts of Africa faster than Western trade remedies have been able to keep up.

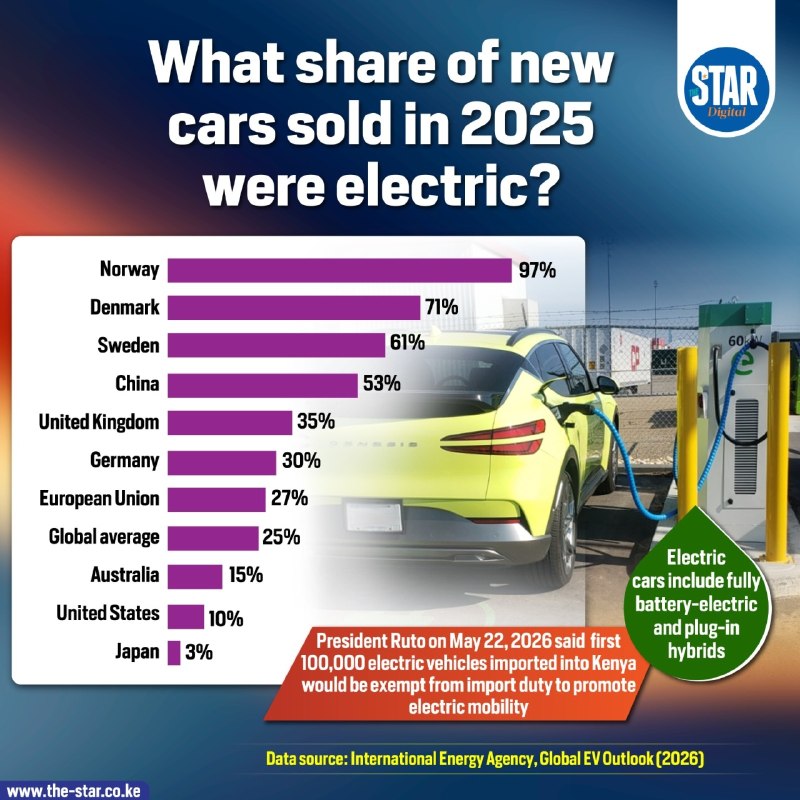

The structural point is not that Chinese cars are "cheap." It is that a country which has built a complete, vertically integrated EV supply chain inside a single regulatory jurisdiction now has a cost curve and a delivery cadence that no other country can match at the same scale. A wire-style infographic circulated by The Star Kenya on 9 June 2026, showing electric vehicles reaching majority share of new-car sales in several countries, underlines the speed at which the technology is crossing from early-adopter markets into the mainstream — a transition in which Chinese brands are over-represented in the affordable segment.

There is a counterpoint worth naming. Western trade officials and several legacy automakers argue that China's export surge is not a free-market outcome but the product of subsidies, forced technology transfer, and under-priced credit. The structural rebuttal from Beijing, repeated across official channels for years, is that the same broad industrial-policy toolkit — tax credits, concessional finance, public procurement preference — has been used by the United States, the European Union, Japan, and South Korea at earlier stages of their own auto industries. Both framings carry real weight; the policy debate now is less about whether the toolkit exists than about whether China's specific deployment of it crosses a line the WTO system was not built to police.

What the Chinese position looks like in plain terms

The Chinese industry and government line on EVs runs roughly like this. China has spent fifteen years building a battery and electric-drive supply chain because its own energy-security arithmetic made it rational to do so. The result is a public good — cheaper, cleaner vehicles — that the rest of the world is now importing. If Western governments consider that an unfair advantage, the appropriate response under existing trade rules is a countervailing duty with evidence, not a generalised framing of Chinese industry as a threat. Chinese manufacturers, for their part, argue that they have invested in overseas plants in Thailand, Brazil, Hungary, and elsewhere precisely to address the political objections to pure exports.

The Western position, in its strongest form, is that no amount of overseas plant-building changes the underlying subsidy structure, and that the speed of Chinese export growth has outrun the capacity of any trade-remedy system to respond in real time. Both are coherent. The honest read is that the global car industry is being repriced in real time, and the repricing is happening on Chinese terms because the supply chain was built there first.

Stakes and what remains uncertain

The near-term stakes are concrete. Chinese OEMs are likely to take further share in markets that lack a domestic auto industry — much of Southeast Asia, large parts of Africa, the Middle East, and Latin America — over the next 24 to 36 months. Legacy European and Japanese volume makers face a structural squeeze in mid-priced segments where Chinese brands are now price-competitive. Battery and component suppliers outside China will continue to consolidate or seek protectionist cover at home.

What remains genuinely uncertain is the trajectory of Chinese domestic demand. BYD's 80% figure assumes the share keeps climbing even as total unit sales plateau. The export number from May suggests overseas demand can absorb a good deal of the slack, but it does not tell us how durable that absorption will be if trade barriers harden. The wire services covering the export beat on 9 June 2026 also pointed to AI-related demand as a driver, which is a different engine from autos and one that can cool independently.

The Monexus reading is that the dominant Western framing of Chinese EVs — as a subsidised threat requiring defensive tariffs — is not wrong, but is incomplete. The more durable story is industrial-policy effectiveness on a scale that has not been seen since the East Asian developmental states of the 1970s and 1980s, and the policy question for everyone else is what the appropriate response is to a competitor that has built the supply chain first and is now exporting the surplus.

This Monexus piece leans on BYD's own 9 June 2026 forecast and Beijing's May export data rather than re-packaging the Western wire line; the structural argument is that the global car market is being repriced on Chinese terms because the supply chain was built there first.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/TheStarKenya