Strait of Hormuz, June 2026: When a Chokepoint Becomes a Talking Point

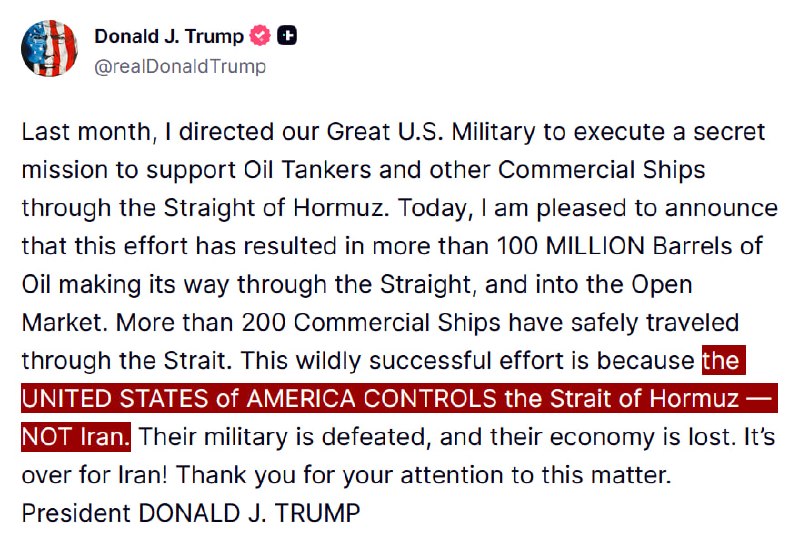

At 18:05 UTC on 10 June 2026, a message moved through the wire claiming that U.S. military operations had helped "more than 100 million barrels of oil and over 200 commercial ships safely transit the Strait of Hormuz." The number — 100 million barrels, 200 ships — was large, specific, and unverifiable from a single Telegram post. It carried the cadence of a victory lap. Eight hours earlier, the chief executive of CMA CGM, the world's third-largest container line, had told a different audience that it would be "unwise" to assume the Strait of Hormuz will return to its pre-conflict state. Both statements landed on the same day, in the same news cycle, and they do not reconcile. The chokepoint is open enough for the White House to count barrels; it is fragile enough for a shipowner to warn that the old baseline is gone.

This is the shape of the story: a U.S. administration presenting maritime escort as proof of restored normality, a top-tier carrier telling markets the new normality is structurally different, and a U.S. regulator — on the same morning — moving to formalise the prediction markets that have been pricing exactly this kind of rupture.

The claim and the count

The number that travelled furthest on 10 June was the 100-million-barrel figure attached to a presidential statement about U.S. military operations in the Gulf. Read literally, the claim is that American forces have shepherded that volume of crude — at typical Hormuz throughput, roughly two to three days of global supply — through the narrow waterway since operations began. The 200-ship figure sits alongside it as a count of merchant vessels moved under escort. Neither figure is broken out by date, by tanker class, by origin, or by destination in the wire text. The headline is doing the work the data should do.

The pattern is not new. Maritime-security statistics in the Gulf have been a running currency since at least the 1980s tanker-war era, when the U.S. Navy's own operational readouts often lagged the political messaging. The difference in 2026 is that the audience is no longer just the OPEC delegations in Vienna or the insurers at Lloyd's. The audience is also the prediction-market traders, the CFTC comment file, and the Telegram group chat.

The carrier's counter

The most useful line published on 10 June came not from a general, a minister, or an analyst, but from the head of a shipping company that actually moves boxes through the waterway. CMA CGM's chief told an industry audience on the morning of 10 June 2026 that it would be "unwise" to assume the Strait of Hormuz will revert to its pre-conflict operating state. The phrasing matters. He did not say the Strait is closed. He said the pre-conflict baseline — the frictionless transit that shippers, charterers, and oil traders priced into contracts for decades — is no longer the working assumption.

Translated into the language of the trade, that means war-risk premia, routing decisions, and insurance underwriting are now calibrated to a different floor. A tanker operator that used to assume a Hormuz transit at, say, $0.30 per barrel of additional premium may now underwrite at a multiple of that. The chief executive was not contradicting the White House; he was clarifying that "safe transit" and "a return to the pre-conflict state" are not the same thing. A road can be open and a different road.

What "more than 100 million barrels" actually measures

The volume figure does useful work, but not the work it is being asked to do. Escorted tonnage is a smaller category than total throughput. A vessel moving under U.S. naval escort through the Strait is, by definition, a vessel the U.S. has decided merits escort — typically a high-value tanker, a U.S.-flagged ship, or a carrier moving under a U.S. task force's protective bubble. The remaining commercial traffic moves under its own decisions, often at higher speed, often with armed private security on deck, and often with the implicit understanding that the U.S. umbrella is a deterrent rather than a chariot.

The 200-ship number, similarly, is a count of discrete escort missions, not a census of the merchant fleet in the Gulf. The total number of transits the Strait has hosted since the latest crisis began is, on most published industry estimates, an order of magnitude larger. The administration's headline picks the numerator that suits the message and leaves the denominator out.

This is not, on the evidence available, a fabrication. It is a framing choice. And the framing is consequential because the same wire is feeding both the political claim of restored normality and the market signal of permanent risk premium.

The structural shift: from escort to embedded presence

Plainly stated, what is happening in the Gulf is the institutionalisation of a military escort regime that used to be episodic. The U.S. has, on this reading, moved from a posture in which Gulf transits are nominally commercial and the Navy responds to incidents, to a posture in which escort is a standing service and a fraction of commercial traffic uses it. The shift matters less for the 100 million barrels — a single quarter of OPEC+ output, in round terms — than for the precedent.

Once escort is a standing service, it acquires a constituency. U.S. naval commands want the missions. U.S. flag operators want the cover. Gulf state coastguards want the signalling. Iranian, Houthi, and other actors who view the waterway as a pressure point now have a permanent target set. The result is a Gulf in which "open" and "closed" are no longer the operative variables, replaced by a sliding scale of risk-priced transit.

The carrier chief's warning lands inside that shift. Pre-conflict Hormuz was, in industry shorthand, a free-access corridor with intermittent insurance add-ons. Post-conflict Hormuz — even with 100 million barrels successfully moved — is a toll road with a moving toll. The 100-million-barrel figure tells the public the road is open. The CMA CGM chief tells the market the toll is permanent.

Prediction markets price the new shape

The third leg of the 10 June story is the CFTC's announced intention to propose new prediction-market rules, allowing most sports contracts while reserving the right to block markets vulnerable to manipulation, per the Wall Street Journal. On its face, the rule is a domestic American question about event contracts on football games and election outcomes. The connection to a Gulf chokepoint is structural, not topical.

Prediction markets have become, over the last two years, the most reactive real-time read on geopolitical tail risk in the U.S. retail-trader ecosystem. Volumes spike on Hormuz headlines, on F-18 overflights, and on shipping-association statements. The CFTC's new proposal is, in part, a recognition that those markets are no longer fringe — and that the manipulation risk now runs in two directions: operators rigging outcomes and political actors treating market prices as policy inputs.

The 10 June juxtaposition is striking. The same morning that the White House announces escorted-barrel counts, the regulator tightens the perimeter on the markets that will price the next Hormuz crisis in real time. The political class wants to claim credit for normalising the Strait; the financial regulator wants to manage the instruments that will, increasingly, tell the public whether the claim holds.

Stakes: who wins, who pays, and over what horizon

In the short term — the next two to four quarters — the winners are the actors with pricing power over the new risk layer. U.S. naval commands and defence contractors in the escort-and-surveillance stack. Private maritime-security firms. War-risk underwriters, who can reprice premia upward without losing volume. Tanker operators with the balance sheets to absorb longer routes around the Cape of Good Hope when Hormuz premia spike. The losers, predictably, are the smaller operators, the importing economies with thin dollar reserves, and any Gulf state that had built fiscal plans on the assumption of a return to pre-conflict throughput.

In the medium term — twelve to thirty-six months — the structural question is whether the escort regime hardens into a permanent feature of the maritime order, with the U.S. effectively running a toll road it does not formally own, or whether the political pressure to declare victory and stand down pushes the Navy back to a responsive posture. The carrier chief's warning suggests the industry is already pricing the first outcome.

The longer-horizon stakes are not just about oil. A chokepoint that is permanently risk-priced reshapes refinery investment, shipping-fleet design (the case for double-hull newbuilds strengthens), and the strategic case for pipelines that bypass the Strait altogether. The Eastern Mediterranean, the Red Sea, and the Cape route are not substitutes; they are layers in a more expensive, more redundant global oil logistics stack. The bill for that redundancy will be paid, eventually, by fuel consumers in the importing economies — and disproportionately by those least able to absorb it.

What remains uncertain

The sources available on 10 June do not, taken together, answer the most basic question: what is the actual current throughput of the Strait of Hormuz, and how does it compare to the pre-conflict baseline? The White House count covers a specific subset — escorted tonnage — and is silent on the rest. The carrier chief's statement is qualitative, not volumetric. The CFTC rule is a process announcement, not a data point on Gulf risk. The wire traffic on 10 June is dense with claims, thin on independent measurement.

Three things would help. First, an independent tonnage series — from Lloyd's List, from Vortexa, or from a Gulf-state customs source — for the same window covered by the 100-million-barrel claim, to test whether the numerator is being honestly described. Second, a war-risk premium series from a named underwriter, to test whether the carrier chief's warning is reflected in the insurance market. Third, a CFTC comment file that records, on the record, whether prediction-market manipulation is being addressed at the venue level or at the political-input level. None of those have been published in the material this article draws on.

The honest read on 10 June 2026 is this: a chokepoint that is open enough to count barrels, fragile enough to count on, and contested enough to be priced in real time by markets the regulator is still learning how to police. The 100 million barrels are real tonnage. The "return to pre-conflict" is not on offer. The 200 ships are a fraction of the fleet. And the prediction markets, in the absence of a return, will keep trading the gap between the two stories.

How Monexus framed this: the wire gave us a presidential claim and a carrier warning on the same day, and we have read them against each other rather than treating either as the day's verdict. The CFTC move is included not as a regulatory item but as the third data point that completes the triangle — political claim, market signal, and the venue where the two meet.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/cointelegraph/1

- https://t.me/cointelegraph/2

- https://t.me/cointelegraph/3

- https://t.me/cointelegraph/4

- https://x.com/polymarket/status/1