Musk's trillion-dollar moment, and the space-data-center bet riding on it

On 12 June 2026, three separate wire-style Telegram channels carried near-identical claims about Elon Musk within ninety minutes of each other. The Epoch Times reported at 17:35 UTC that investors are betting on Musk establishing data centres in space and building a permanent human colony on Mars. At 17:16 UTC, One America News declared Musk "officially set to become the world's first trillionaire." At 17:03 UTC, the RN Intel channel summed up the mood in seven words: "Elon Musk has more money than he did yesterday."

The convergence is the story. Two genuinely different bets — one about personal net worth, the other about a multi-trillion-dollar orbital infrastructure play — are now being narrated as a single narrative arc, and capital is moving on the assumption that both are real. The available reporting, however, is thin enough that the claims deserve to be pulled apart before the market treats them as fact.

The trillion-dollar claim, and where it actually comes from

The "world's first trillionaire" line is not new. It has circulated since at least 2021, anchored to projections about Tesla's market capitalisation, SpaceX's private valuation, and Musk's equity stakes in both. What changed in 2026, according to the OANN post at 17:16 UTC on 12 June, is the framing: "officially set," not "on track to" or "could become."

The qualifier matters. Forbes' real-time billionaires index, which is the most widely cited public benchmark, has long refused to crown a trillionaire, in part because the underlying private-market valuations that drive Musk's net worth — SpaceX, xAI, Neuralink, Boring Co. — are marked to internal pricing rounds rather than traded prices. The same ambiguity runs in the opposite direction: when SpaceX raises at a higher valuation, Musk's paper worth jumps overnight; when a funding round is delayed, it can sit still for months. The "official" language in the OANN item does not change that. It simply restates an existing projection as a fait accompli.

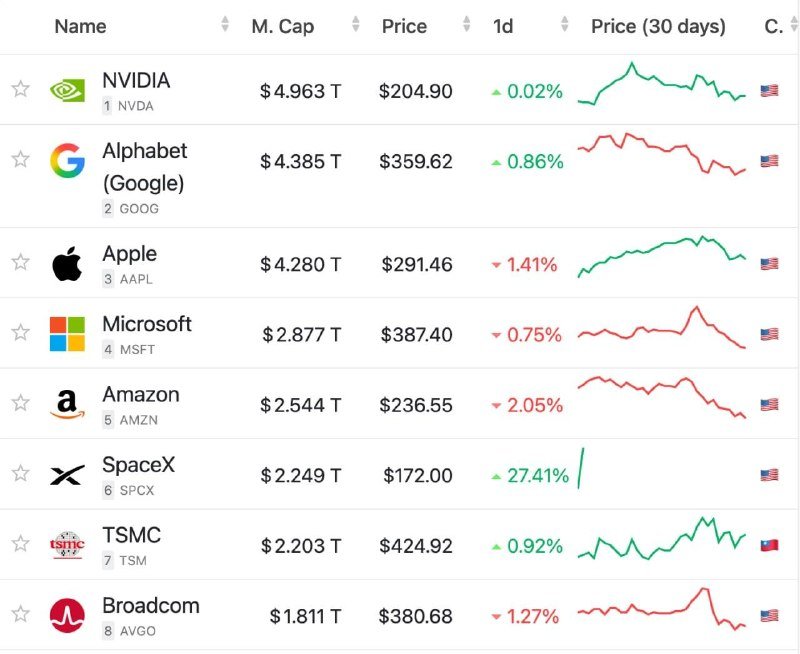

The Epoch Times item, by contrast, points at a different mechanism entirely: investor bets on Musk-led orbital infrastructure and a Mars colony. These are not balance-sheet events. They are speculative capital allocations — venture rounds, special-purpose vehicles, themed ETFs, and derivatives on private-company marks — that price in a future in which Musk's companies own a meaningful share of off-planet compute and off-planet human presence. Whether those bets pay off is a separate question from whether Musk is technically a trillionaire on paper next quarter.

The space-data-centre bet, and what the reporting actually shows

The Epoch Times post links to a piece on its own domain framing the space-data-centre thesis in familiar terms: energy abundance in orbit, continuous solar exposure, radiative cooling, and a long-term cost curve that terrestrial hyperscalers cannot match. The argument is structurally plausible. It is also, in the public sources available on 12 June 2026, more thesis than roadmap.

What the available reporting does not establish: a specific SpaceX programme for orbital data-centre deployment with a named launch date, a contracted anchor customer, a per-kilowatt orbital cost model, or a regulatory pathway for the kind of spectrum, debris-management, and orbital-traffic coordination that a fleet of compute-bearing satellites would require. The RN Intel item at 17:03 UTC carries no sourcing beyond the assertion of net-worth movement. The OANN post at 17:16 UTC links to its own article, not to a primary financial filing or an independent valuation.

That absence is the story. Three channels, ninety minutes, two trillion-dollar-scale claims, and the only traceable primary documents are the channels' own stories. Investors who position on the basis of the framing are positioning on the framing itself — on the social fact that Musk-adjacent assets are being talked about at this scale — rather than on a discrete operational milestone.

Why the two bets are running on the same rails

The structural pattern is worth naming plainly. A small number of individuals now sit at the intersection of three things that used to be separate: the largest pools of deployable private capital, the dominant platforms through which public discourse is routed, and the infrastructure on which frontier computation, energy, and transport actually run. When a single name is plausibly the top mover on all three axes, the net-worth story and the orbital-infrastructure story collapse into a single narrative, and that narrative does work in the real economy regardless of whether either leg is true.

That is not a critique of Musk. It is a description of how concentrated capital markets handle concentration. The same dynamic has, in the past decade, attached trillion-dollar valuations to firms whose revenue bases could not, on a conventional multiple, justify them — because the market was pricing in optionality on a future product line rather than current cashflow. The orbital data-centre thesis is, in effect, a renewable source of optionality: every launch milestone, every power-beaming demonstration, every regulatory green light, becomes a reason to re-mark the private-company stake upward.

The counter-read is also worth registering. Sceptics of the trillionaire framing note that paper wealth and realised wealth are different beasts, that founder-led private valuations are inherently procyclical, and that any sustained drawdown in Tesla's share price — triggered, for example, by EV demand softening, Chinese competitive pressure on margins, or a regulatory action against Autopilot — would compress the headline number rapidly. A market-cap figure that takes years to assemble can be given back in weeks.

What to watch, and what is still genuinely uncertain

Three things will determine whether the 12 June narrative ages well. First, whether SpaceX or any Musk-adjacent entity publishes a concrete orbital data-centre architecture — not a render, not a keynote slide, but a programme with mass budgets, launch cadence, and a customer. Second, whether independent valuation houses treat the private-company marks as observable or as modelled; the difference is the difference between a trillionaire and a notional one. Third, whether the political economy around terrestrial data-centre build-out — power-grid constraints, water-use scrutiny, local opposition — tightens enough to make the orbital alternative look like a necessity rather than a moonshot.

The honest summary on 12 June 2026 is that two large bets are running in parallel and the available sourcing cannot yet adjudicate either. The trillion-dollar headline is a re-assertion of an existing projection. The space-data-centre bet is a capital-allocation story dressed as a deployment story. Neither is false on the evidence available — neither is confirmed either. What is confirmed is that the bets are now being told as one story, and that the telling, on its own, is moving money.

Monexus framed this as a concentration-of-capital story rather than a personality story, and pulled the trillionaire claim and the orbital-data-centre claim apart because the source material treats them as one event when the evidence does not.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/OANNTV

- https://t.me/rnintel