SpaceX's $170 debut is not a victory lap. It is a tell.

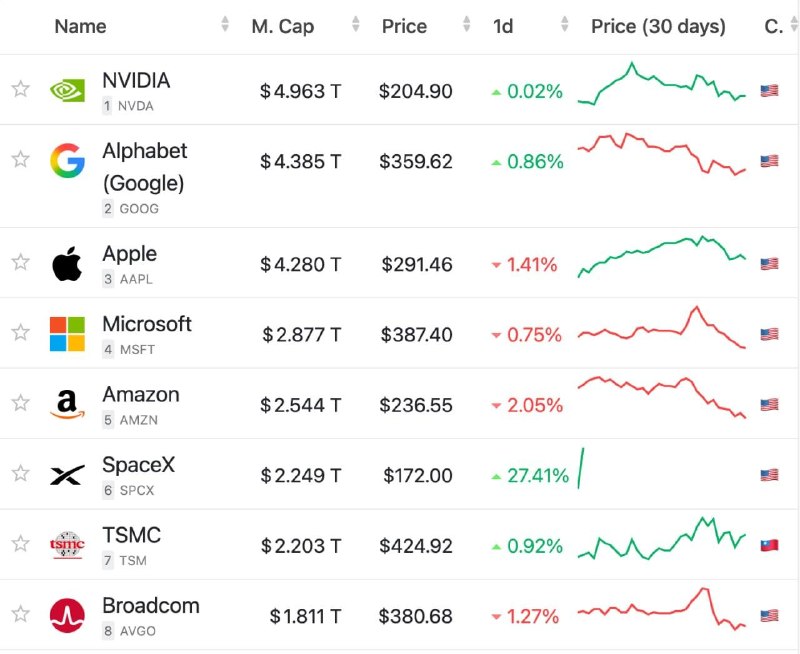

At 14:00 UTC on 12 June 2026, SpaceX began trading on the Nasdaq under the symbol SPCX. By 16:53 UTC the shares had touched a session high of roughly $170 — about 25% above the $135 IPO price flagged in pre-market indications. Per Bloomberg reporting carried in the morning flow, the order book pulled in more than $350 billion of demand. A perpetual contract tracking SPCX on Hyperliquid, which had been sliding through the week, reversed course and the implied valuation, on the back of a first-day gain above 35% in shadow markets, drifted toward $2.4 trillion. By late European afternoon, a Euronews flash had SpaceX knocking on the door of the world's six largest listed companies. It is, on paper, a triumph.

It is also the kind of number that should make a serious reader suspicious rather than impressed. A $2.4 trillion valuation for a private space and satellite company a decade ago would have been a punchline. Today it is a market quote. The story worth telling is not that SpaceX flew; it is what a market willing to crown it tells us about the market itself.

The price action is not the story

The temptation is to read the first-day chart as a verdict on Elon Musk's industrial empire — on Starlink's subscriber base, on the cadence of Starship, on the contracted NASA and Pentagon backlog. None of that is wrong, and none of it is the point. A 25% pop on a heavily oversubscribed IPO is, in the modern Nasdaq idiom, almost a regulatory artefact. It tells you the book was priced far below where the marginal buyer stood. It tells you the syndicate left money on the table, deliberately, because the prestige of the listing — the second such prestige event for a Musk-led vehicle in three years — was always worth more to the seller than the marginal $35 of first-day uplift.

Bloomberg's note that the float is set to "mint thousands of new millionaires, including cafeteria workers" is the honest line. The IPO is a wealth-distribution event dressed as a capital-markets event. The dramatic actors are not the institutions; they are the rank-and-file equity holders who, for the first time, hold something that prints on a tape.

The shadow market is the story

The more interesting print is the one that didn't happen on Nasdaq. The SPCX perpetual on Hyperliquid had been falling all week as the IPO approached — the kind of pre-listing drift that reflects sceptical offshore positioning. When the stock opened strong, the perpetual bounced, and Bloomberg's read of other shadow markets implied a first-day gain north of 35%. The convergence of a regulated opening price around $170 and a synthetic market implying something close to a 35% lift is, in a healthy market, a tension. In this market, it is a feature.

What the shadow tape is really saying is that the marginal price-discovery on the most-watched US listing of the year is being done off-exchange, on venues that did not exist a decade ago, by participants who do not clear through DTCC. That is not a complaint. It is a structural fact. The split between the official print and the perp-implied valuation will narrow as the float seasons, but the gap on day one is a measurement of how thin the regulated discovery process has become for the most consequential listings.

What the appetite actually signals

More than $350 billion in demand, against a deal sized for a small fraction of that, is the kind of imbalance that, in a saner decade, would draw questions about what investors were doing with their alternatives. Treasuries at the front end were yielding meaningfully below inflation for most of the cycle. The largest technology incumbents have spent two years trading sideways on earnings that the market refuses to re-rate. Gold has done the work of a real asset for central banks but is not a productive holding for a pension fund. The SpaceX order book is what happens when every other bid has been neutralised: capital concentrates on the one name where the growth narrative has not yet been fully arbitraged away.

Read this way, the IPO is not a verdict on SpaceX. It is a verdict on the shortage of investable growth at scale inside the US public market. That is a less flattering read, and the wire services have not been in a hurry to write it.

The other shoe has not dropped

Two things remain genuinely uncertain. The first is the float. SpaceX has historically rewarded employees with private liquidity; a Nasdaq listing changes the tax and lockup geometry for a very large group of holders, and the eventual supply path matters as much as the demand curve does. The second is what a $2.4 trillion reference valuation does to Musk's other listed vehicle, Tesla, which has spent the year defending the thesis that it is, at some level, an autonomous-driving and robotics platform rather than a car company. The closer SpaceX trades to the implied mark, the more uncomfortable that comparison becomes in both directions.

The market got its hero moment. The more useful question is what it will do with the hangover.

— Monexus framed this against the wire by reading the debut not as a corporate milestone but as a read on the state of US capital allocation: a heavily oversubscribed book against a thin growth-pickings backdrop, with meaningful first-day price discovery happening in offshore perp markets rather than on the listed tape.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/euronews

- https://t.me/s/euronews

- https://x.com/unusual_whales/status/

- https://x.com/unusual_whales/status/

- https://x.com/unusual_whales/status/