SpaceX's $75bn IPO lands on Nasdaq — and Washington barely had time to read the prospectus

On the morning of 12 June 2026, SpaceX began trading on the Nasdaq under ticker "SPAX," capping the largest initial public offering in market history. The rocket-and-starlink operator sold roughly 555.6 million shares at $135 each, raising $75 billion and putting the company on a fully diluted valuation of about $1.8 trillion, according to reporting on 11 June by BBC News and financial press tracked by Monexus. The deal is large enough, on its own, to redraw the upper bound of what public equity is asked to absorb in a single session — and it lands with the United States Securities and Exchange Commission given what one source described as "almost no time" to review it.

The headline number is the story, but the structure underneath it is the more lasting one. A private company built on classified-adjacent government contracts, a vertically integrated launch and satellite-internet monopoly, and the personal brand of its largest shareholder is now priced into the retirement portfolios, index funds, and 401(k) target-date allocations of ordinary Americans. The retail-investor question — how much of this float actually lands in small hands — is the political question of the next 72 hours.

The price tag and the math

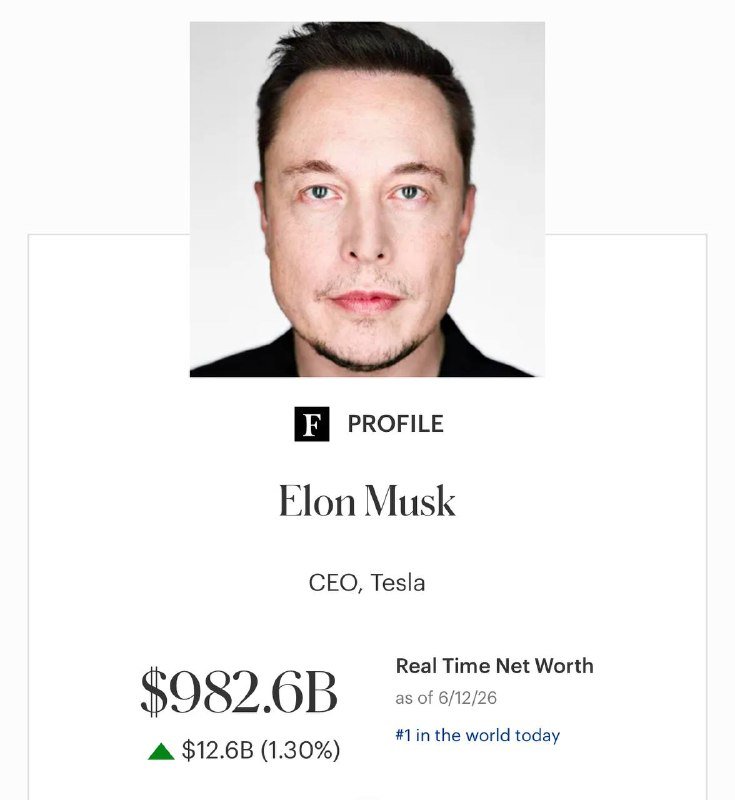

SpaceX priced at the top of its marketed range. At $135 a share and 555.6 million shares sold, the gross proceeds work out to $75 billion — a record, exceeding the previous benchmarks set by Saudi Aramco's 2019 listing and Alibaba's 2014 debut. BBC News, citing the company's filings, reported on 11 June that the fully diluted equity value would approach $1.8 trillion, a figure that, if sustained on the open market, would push Elon Musk past the trillionaire threshold that has so far belonged only to private wealth estimates.

Two numbers matter more than the headline. First, the free float: the share of the offering directed to retail buyers is reportedly in the low 20 percent range, according to a person familiar with the matter cited in wire reporting on 11 June. The remainder is understood to be allocated to institutional anchor investors, sovereign and quasi-sovereign funds, and the company's strategic partners. Second, the locked-up insider position: Musk's pre-IPO stake does not change hands on day one, but the valuation it implies converts a private balance sheet into a public benchmark that influences every subsequent capital-markets decision the company makes — from debt issuance to acquisition currency.

The regulator's compressed window

The most uncomfortable detail in the pre-debut coverage is procedural. Senator Elizabeth Warren, a long-running critic of Musk's corporate governance and a frequent SEC interlocutor, publicly warned on 11 June that the regulator was being given "almost no time to act" on her outstanding concerns about the listing, according to reporting carried by Unusual Whales. The accusation is that a deal of this size and complexity — spanning launch, defence, satellite broadband, and AI-adjacent data-centre buildouts — was pushed through a review window too short for a thorough S-1 vetting.

The counter-narrative from the company's bankers, echoed in the analyst notes tracked on 11 June, is that the IPO process has been underway for the better part of a year; that the prospectus has been on file with the SEC throughout; and that the final pricing window was always going to be tight once the company cleared its last technical milestones. The truth probably sits between the two: the disclosure window is legally compliant, but the political window — the period in which a regulator feels it has the standing to slow-roll a marquee listing — has effectively closed.

What the debut means for crypto, for indices, and for Musk

Crypto markets read the listing as a sentiment signal. CoinDesk's day-ahead note on 12 June framed the debut as a binary event for digital assets: a clean, well-bid open validates the risk-on thesis that has carried tokens through the first half of 2026, while a fumbled first session risks dragging high-beta names lower. The mechanism is not mystical — it is margin and ETF flows, with Nasdaq-listed bellwethers acting as a proxy for the appetite to hold long-duration growth assets at any price.

The index implications are more durable. At a $1.8 trillion fully diluted value, SpaceX would rank among the five largest US-listed companies on its first day, dragging benchmark weights and forcing passive flows to rebalance. The retail allocation, in the low 20s, is the slice that gives the listing its political character: small investors will own enough of the float to feel they participated, and not enough to do anything about it if the trade goes wrong.

The stakes, plainly stated

If the listing holds its footing, three things follow. The US equity market has absorbed a single new entrant larger than any it has processed before, and the policy debate about concentration moves from think-tank papers to congressional hearings. The public-equity bar for "what counts as a technology company" shifts upward, to the detriment of smaller competitors trying to clear the same listing threshold. And Musk, whose net worth has been a private estimate for two decades, becomes a balance-sheet fact on a public tape — which is a different kind of political exposure than running X, Tesla, and a federal-contract portfolio on a private cap table.

The uncertainties remain. The sources do not specify which regulators have cleared which filings, whether the SEC issued any formal comment letter on the S-1, or how the locked-up insider position will be released over the post-IPO horizon. Retail participation is described in ranges, not commitments. The trillionaire threshold is conditional on a sustained secondary-market price, not the IPO print. A single trading session is not a verdict; it is the start of one.

Desk note: Monexus framed this as a market-structure story with a regulatory subtext, not a personality piece. The wire cycle on 11–12 June led with the dollar number; we are holding the SEC-window question, the retail-allocation percentage, and the index-weight consequence as the three beats that will outlast the opening bell.