SpaceX's $350 billion IPO is a triumph — and a stress test for what 'success' now costs

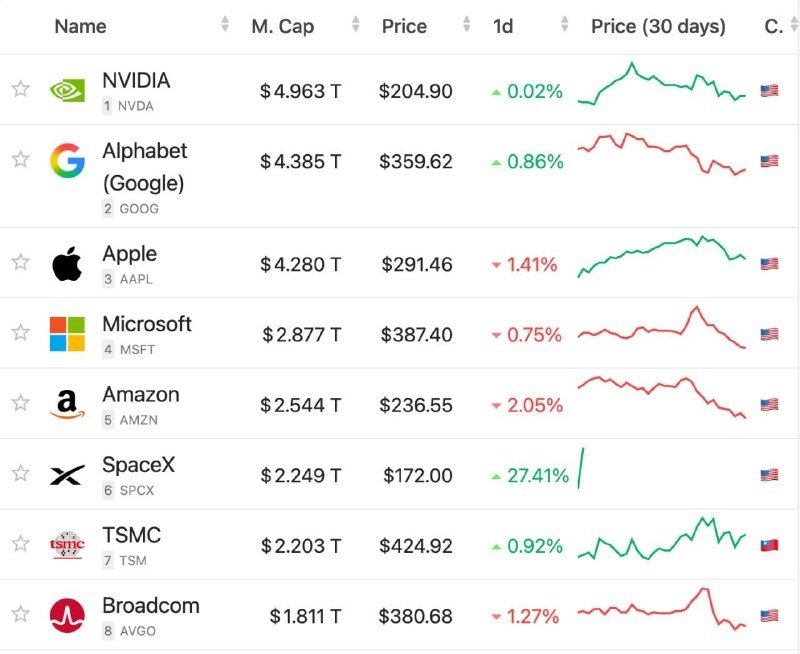

At 10:00 ET on 12 June 2026, SpaceX began trading on public markets, and within hours Reuters and Polymarket wire chatter reported the offering more than 4.5 times oversubscribed, with demand reportedly topping $350 billion. Elon Musk, who told a Nasdaq audience he had once given SpaceX less than a 10% chance of success at its 2002 founding, rang the opening bell. The story is being told, almost everywhere, as a clean American success: a private rocket company built on impossible odds, now the most-watched listing of the decade.

The framing is not wrong. It is just incomplete. The four-and-a-half-times-oversubscribed figure is, in the language of the trade, a measurement of how much money the world's largest investors were forced to leave on the table. It is the loudest signal in months that the upper end of the capital market is not short of cash — it is short of places to put it. Read against the Reuters reporting on Musk's continued ability to retain a personal following even as public attitudes toward the ultra-wealthy have soured, the IPO lands less as a referendum on rockets and more as a referendum on how concentrated the modern wealth stack has become.

The debut is not the story — the demand is

A 4.5x oversubscription on a deal of this size does not happen because retail investors woke up excited about orbital mechanics. It happens because the largest pools of capital — sovereign wealth funds, mega-funds, the sort of asset managers whose cheque size is measured in single transactions of nine figures — had already decided they could not afford to be underweight. Reuters reported the oversubscription figure on 12 June 2026; Polymarket, citing market chatter, put demand above $350 billion on the same day. Those numbers, if accurate, are the actual headline. The listing price is the door; the demand is the queue.

This matters because oversubscription of this magnitude is, mechanically, a transfer. When a deal is covered four and a half times, the issuer is leaving the difference between what the market would pay and what it is being charged on the table. For an issuer that is already the most valuable private company in history, that is a choice, not a market verdict. The market is not disciplining the price. The price is disciplining access.

The founder quote is doing more work than it should

Musk's line about giving SpaceX less than a 10% chance at founding — relayed on the Polymarket wire at 13:58 UTC on 12 June 2026 — has already been laundered into the conventional telling. It is a clean narrative: visionary doubted, visionary vindicated. The problem is that the quote functions as a rhetorical eraser. It papers over the roughly $100 billion in cumulative equity capital, the NASA anchor contracts, the Starlink cashflows that now subsidise everything else, and the structural advantage of operating in a regulatory environment that was, by design, friendly to a single national champion.

Tom Mueller, who told the BBC on 12 June 2026 that he was employee number one at SpaceX, offered a more honest account. The company survived its early years on the back of federal launch contracts and a small group of engineers who took pay in equity that, for most of the 2000s, looked worthless. The 10% odds were real. So was the public money.

A counter-read the wires are skipping

There is a plausible alternative reading. SpaceX's orbital launch cadence, its reusable-booster economics, and its Starlink constellation are genuine industrial achievements that no other country — not China, not the European Space Agency, not Roscosmos — has matched at scale. On the merits of the business, the demand is rational. Investors are not buying a personality; they are buying a monopoly position in low-earth-orbit launch.

That is also the worry. A company with a near-monopoly on a strategic national capability, controlled by a single individual, listed on terms that ration access to the largest pools of capital in the world, is not a market outcome in the older sense. It is a state-private hybrid that the capital structure has not yet learned how to price. Reuters's framing of Musk's continued personal popularity amid a broader turn against the ultra-wealthy is the most honest version of the contradiction: the same public that resents concentrated wealth is, through its pension funds and index trackers, a passive holder of it.

What the next twelve months will test

The real question is not whether SpaceX clears its first-day pop. It is whether the public market becomes the disciplining mechanism its proponents claim, or whether the oversubscription ratio simply hardens into a permanent feature. If four-and-a-half-times-oversubscribed becomes the floor for the next marquee listings — and the Polymarket chatter suggests the order book thinks it will — then the structure of the 2020s equity market is set: a small number of issuers, rationed by a small number of allocators, with retail and smaller institutions watching from the floor.

The most contested point remains the simplest: whether the $350 billion in reported demand is genuine investible appetite or a coordinated expression of fear-of-missing-out by funds that cannot, in practice, be underweight the only live private space franchise. The sources do not resolve this. Nasdaq, the lead underwriters, and SpaceX itself have not, in the materials reviewed, published a full breakdown. Until they do, the IPO is best read not as a verdict on SpaceX but as a snapshot of how thin the upper edge of the capital market has become — and how much of the rest of us is, quietly, along for the ride.

— Monexus framed this as a structural story about concentrated capital, not a corporate-profile piece; the wire line is still leading with the founder quote, which is why we led with the order book.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://x.com/Polymarket/status/

- https://x.com/Polymarket/status/

- https://x.com/Polymarket/status/

- https://x.com/unusual_whales/status/