Tokenised IPOs were supposed to open SpaceX to retail. They ended in cancellation

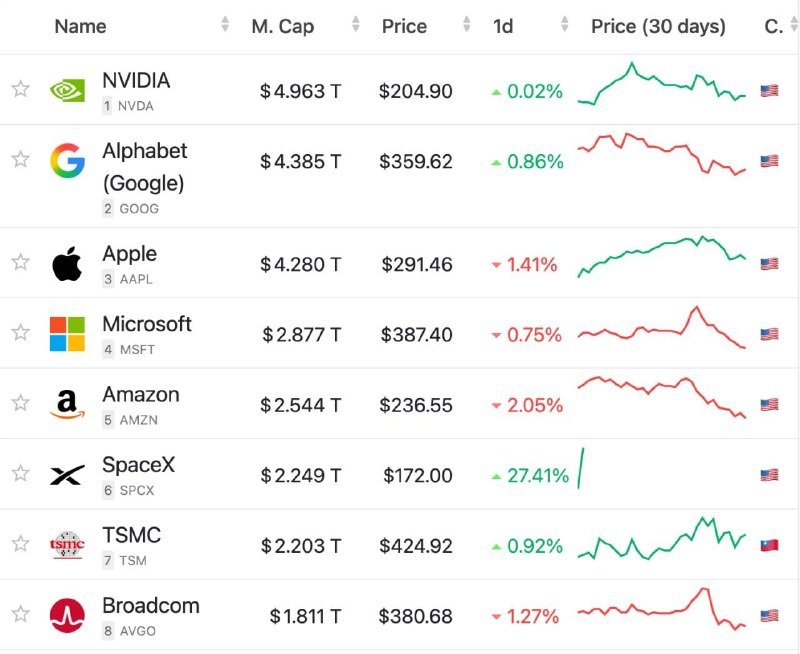

The news on 12 June 2026 was not that SpaceX went public. It was that three of the largest offshore crypto exchanges — Binance, Bybit and Bitget — quietly cancelled the tokenised SpaceX IPO campaigns they had marketed to retail users, citing an "allocation shortfall" in coordinated press notes circulated through the day. The headline read like a footnote next to the larger story: SpaceX's market debut, the 35 percent jump signalled by derivatives, the company's emergence as the eighth-largest public holder of Bitcoin with 18,712 BTC on its balance sheet. Read together, the cancellation and the IPO tell a more useful story about who actually gets access to the year's most anticipated listing.

Retail investors were promised a back door into a private company that, until this week, existed only in the ledgers of venture funds, sovereign vehicles, and the secondary desks that serve them. Tokenisation — the wrapping of a single private-market share in a synthetic, on-chain instrument — was sold as that back door. Binance, Bybit and Bitget each built landing pages, ran countdown timers, and accepted user commitments denominated in stablecoins. As of 17:18 UTC on 12 June, those pages were being walked back.

What "allocation shortfall" actually means

Exchanges do not, as a rule, admit that they oversold a product. The phrase "allocation shortfall" is a tell. It means the counterparty holding the underlying shares — typically a private-market desk or a structured-note issuer — was unwilling or unable to deliver the number of tokens the marketing campaign had implied. In a traditional IPO this is the moment the syndicate rebalances; in a tokenised wrapper it is the moment the wrapper admits the wrapper is not the asset. The retail user ends up holding a claim on a claim on a claim, with three layers of counterparty risk stacked between them and any actual SpaceX common stock.

The campaign language during the run-up, judging from the public material that circulated, leaned hard on the word "exposure." Users were not buying SpaceX. They were buying a structured product whose value was meant to track SpaceX. When the underlying allocation came in light, the exchange had two options: dilute the per-token backing across more users, or cancel. They cancelled. That is the honest answer. It is also the rarer one in this corner of the market.

The structural read

A privatised asset cycle is being constructed in real time, and the retail-facing edge of it is the part most likely to fail. Private market shares are scarce by design. The funds and family offices that hold them pay for that scarcity through lockups, capital calls, and the implicit promise that they will not flood the cap table with retail flow. Tokenisation, on paper, was supposed to disaggregate that scarcity — one private share sliced into a thousand tradable units, each priced for a retail wallet. In practice, the issuer of the token still has to source the underlying shares from a counterparty that has a relationship with the company. If that counterparty can only deliver a fraction of the demand, the token does not become more accessible. It becomes a rationed claim with worse economics than the original instrument.

This is not a new problem. The 2021 boom in tokenised pre-IPO products — the synthetic Coinbase, the synthetic Robinhood, the synthetic Stripe — ran into the same wall and produced the same awkward press notes. The difference in 2026 is the scale. SpaceX is the most anticipated listing of the cycle. The retail demand that was being aggregated across three of the largest offshore venues is, by definition, the demand the institutional book did not want to absorb. When the institutional book was already oversubscribed — as derivatives on the day suggested, with a 35 percent jump being signalled — the only direction for retail flow was into the wrapper. The wrapper ran out of wrapper.

What the Bitcoin treasury tells you

The same news cycle that carried the cancellation carried SpaceX's appearance as the eighth-largest public Bitcoin holder, with 18,712 BTC on the balance sheet. The juxtaposition is not incidental. A company that publicly holds a treasury reserve of that size is signalling something specific to public-market investors: a willingness to use a non-cash, non-Treasury asset as a store-of-value proxy. That is a posture that institutional capital reads as sophisticated. It is also a posture that retail users buying a token with the SpaceX name on it are not, in any direct sense, buying into. They are buying exposure to an equity, in a wrapper that has now been publicly shown to under-allocate.

The honest framing is that retail users are being sold the brand of a private company, not its economics. The Bitcoin treasury belongs to SpaceX. The token belongs to the issuer. The user holds a contract with the exchange. These are not the same instrument, and the 12 June cancellations are the clearest evidence yet that the gap between them is widening rather than closing.

What the wire said, and what it didn't

Coverage of the IPO debut and the treasury disclosure leaned into the narrative of strong debut demand and bullish derivatives positioning. Coverage of the retail-campaign cancellation leaned into the language the exchanges themselves provided — "allocation shortfall," "demand outstripped supply," the implication that the product was a victim of its own success. Neither framing is wrong. Both are incomplete. A product that is cancelled after retail users have already committed stablecoins is not simply over-subscribed. It is a product whose issuer could not honour the marketing.

The structural pattern, repeated often enough to be visible, is that tokenised private-market campaigns are being used to harvest retail demand that the institutional book will not absorb, with the exchange keeping the float and the user keeping the cancellation notice. The SpaceX episode is the largest and most public instance of that pattern to date. It will not be the last.

This publication views the 12 June cancellations as the cleanest data point yet on the difference between exposure to a brand and ownership of an asset — and on the specific role offshore exchanges have come to play in the gap between them.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/CryptoBriefing

- https://t.me/CryptoBriefing

- https://t.me/CryptoBriefing

- https://t.me/CryptoBriefing