A million-dollar starter home and a trillion-dollar rocket: the two Americas Elon Musk is building at once

On the same day Zillow declared 242 cities off-limits to first-time buyers, Elon Musk told markets SpaceX could clear $1 trillion in revenue by 2030. Both announcements describe the same economy — and neither is the whole story.

On 15 June 2026, Zillow published a finding that should end the polite national conversation about "affordable" housing. The portal now counts 242 U.S. cities in which a so-called starter home costs at least $1 million — triple the figure recorded in 2020. Six years ago, a million bucks still bought something in most of the country. Today, in a quarter of the cities Zillow tracks, it does not even buy a first step onto the ladder. The line between "aspirational" and "impossible" has simply been redrawn, and the redecoration was done without anyone voting on it.

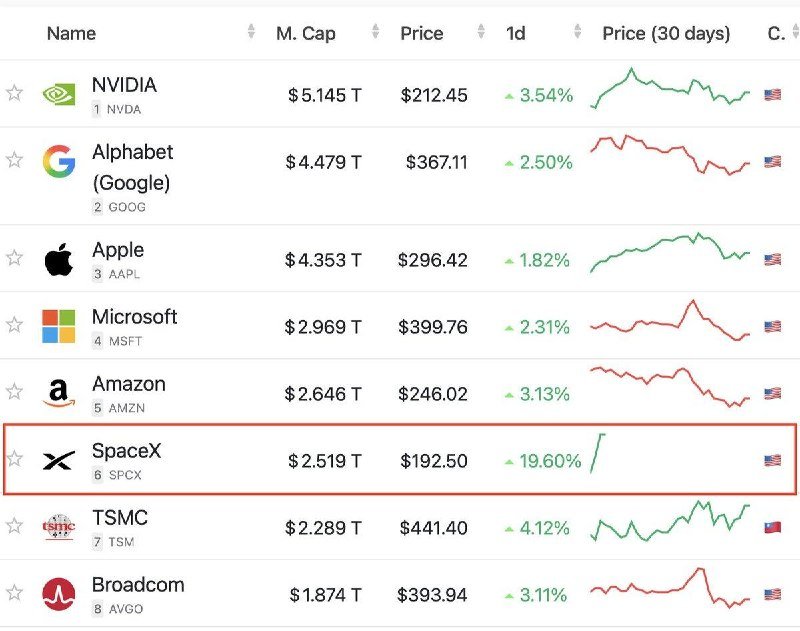

Hours later, the same news cycle delivered a different number. Elon Musk, speaking publicly on 15 June, told markets he believes SpaceX could reach approximately $1 trillion in annual revenue by 2030. The figure is staggering on its face; the more striking thing is that the broader market treated it as a plausible anchor for valuation rather than a CEO's daydream. SpaceX shares rose about 8% on the day.

Read those two data points together and the United States stops looking like a single economy. It looks like two of them, stacked on top of each other, sharing a currency and little else.

The price of entry, and the price of escape

For a generation that was promised a country where work translated into a home, the Zillow number is the corrective. The starter home — the modest, sometimes shabby, almost always viable first purchase — has been functionally abolished in 242 cities. The cities are not exotic. They include mid-sized industrial centres, Sun Belt retirement towns, college cities, and former bedroom communities. The mechanism is well-rehearsed: a decade of suppressed construction, a pandemic-era reshuffle of where work happens, institutional capital crowding out first-time buyers, and a mortgage market that scales with the asset rather than the buyer. The result is not a crisis in any single zip code; it is a structural reset of who gets to live where.

The $1 trillion SpaceX number, meanwhile, is the price of escape. The rocket company, fresh off its IPO trajectory and already sitting on a private valuation north of $300 billion, is now being priced by public-market participants as if its addressable market is the entire orbital economy of the next decade. Musk is not wrong to point at launch demand, Starlink subscriptions, Pentagon and intelligence-agency contracts, and a nascent point-to-point Earth transport business. There is real revenue behind the pitch. The bet is that orbital infrastructure becomes the next utility — and utilities, when they work, do generate trillion-dollar revenue lines.

Two economies, one balance sheet

The juxtaposition is not a coincidence of news timing. It is a portrait of capital allocation in an economy that has stopped compounding for the median household and started compounding for the frontier.

The arithmetic of a $1 trillion SpaceX revenue line implies that orbital bandwidth, launch capacity, and downstream services become a line item on the global economy the way container shipping or cloud compute is today. The arithmetic of 242 cities with million-dollar starter homes implies that the largest single investment most American families will ever make is now gated behind inheritance, dual-professional income, or institutional capital. One set of numbers describes an asset class that has been de-risked into something resembling a sovereign contract. The other describes a basic necessity that has been re-priced into a luxury good.

This is what "two-track growth" looks like in practice. The first track is accessible, in principle, to any household with a job, a savings habit, and a fifteen-year horizon. It no longer works. The second track is accessible, in principle, to any institutional allocator with patience and a balance sheet. It is being subsidised, indirectly, by the same fiscal and monetary environment that did nothing to keep starter homes within reach. The Federal Reserve held policy rates at near-zero for the better part of a decade after 2008 and again after 2020; asset prices responded. Wage growth for the median worker did not respond at the same speed. The result is the bifurcation the Zillow data now confirms.

The markets know exactly what they are pricing

There is a counter-narrative worth airing. The same investors who are underwriting a $1 trillion SpaceX projection are, in aggregate, the same ones sitting on portfolios of single-family rental homes, mortgage-backed securities, and build-to-rent developments. They are not stupid. They are not blind to the Zillow number. They are, however, doing the thing that allocators have always done: positioning for the world that is actually arriving, not the one that a 1970s social contract promised.

The optimistic read is that the frontier economy will eventually pull the median up. SpaceX revenue, Starlink subscriptions, and the industrial base that builds them are real American jobs — many of them manufacturing, many of them in places that have lost ground for two generations. If the orbital economy scales, those jobs scale with it.

The pessimistic read is the obvious one. Trillion-dollar frontier revenues do not automatically translate into cheaper starter homes. They translate into equity returns, options exercises, and the further accumulation of the asset class that the median household was already priced out of. The link between a soaring SpaceX market cap and a 25-year-old nurse's ability to buy a condominium in Phoenix is, at best, indirect and long. There is no mechanism in U.S. policy right now that converts the first into the second at speed.

Stakes

Both stories will keep moving. Zillow's count of million-dollar starter cities will, on current trajectory, pass 300 within a year. SpaceX's revenue line, if it tracks even halfway to Musk's $1 trillion 2030 anchor, will redraw the market-cap leaderboard in U.S. equities. The question is not whether both trends continue. The question is what the country does in the gap between them.

That gap is the actual policy story of the next decade: who pays for the housing that the market will not build, who shares in the upside of the frontier economy that the market is already pricing, and whether the institutions that were built to do both — Fannie, Freddie, the FHA, the public housing stock, the community reinvestment architecture — get rebuilt for the scale of the problem Zillow has now put a number on.

The two announcements landed on the same day. The housing story will not get a Cointelegraph push notification. The SpaceX story will. That asymmetry of attention is itself the most honest read of where the country's capital is going.

This publication finds that the convergence of these two data points is the most under-reported economic story of the week: a U.S. economy in which the most ambitious private venture of the decade is being priced for a trillion-dollar trajectory, while the most basic private investment of a working life is being priced out of a quarter of the country.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://x.com/polymarket/status/

- https://x.com/polymarket/status/

- https://x.com/polymarket/status/

- https://t.me/cointelegraph/

- https://t.me/cointelegraph/