Musk, SpaceX and the Personalisation of Wealth: A $6 Billion Tick

A single dollar move in SpaceX's private share price is now worth roughly $6 billion to Elon Musk — a sensitivity ratio that has turned a private rocket company into a proxy for the personal fortune of the world's richest person.

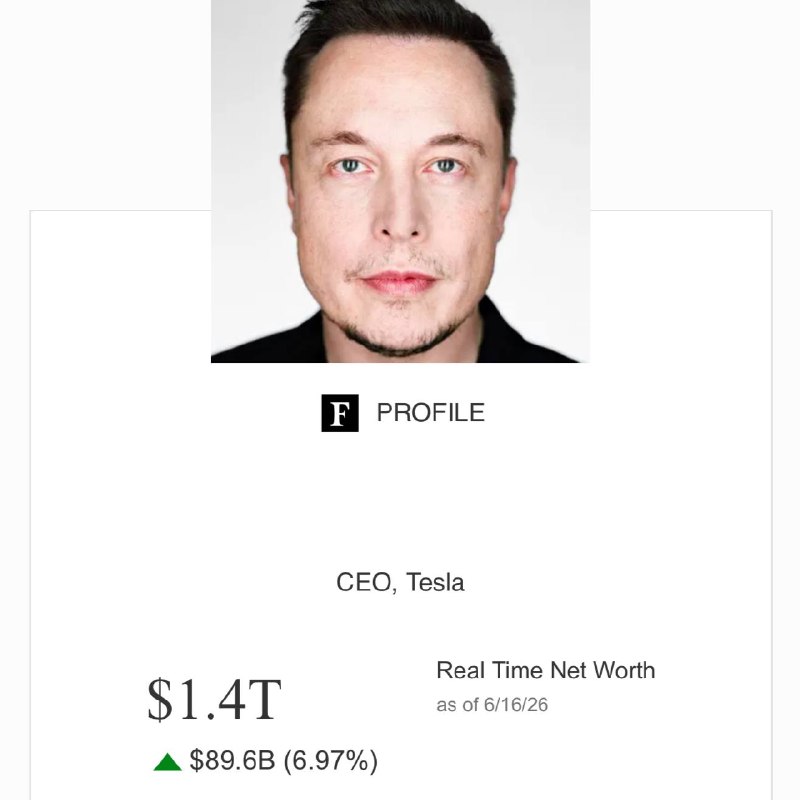

On 16 June 2026, two data points landed within hours of each other and, taken together, drew a circle around the question that has quietly defined this corner of the financial markets. Bloomberg's index team put the sensitivity ratio at roughly $6 billion of Elon Musk's net worth for every $1 move in the SpaceX share price. By the evening of the same day, market commentary circulating on Cointelegraph's newswire had sharpened the comparison further: Musk's net worth had, by some reckonings, surpassed the market capitalisation of Bitcoin itself. The figures are imprecise, the timing is imprecise, and the underlying valuation is private. But the structural point is sharp. The world's largest personal fortune is no longer a portfolio of distinct bets. It is a single bet, levered.

What the 16 June datapoints really expose is that SpaceX has stopped behaving like a private operating company in the way the rest of the market values private operating companies. It behaves like a personalisation of Musk himself — a tradable proxy for the founder, marked at the margin by people who say out loud, as Jim Cramer did on CNBC, that they are not buying earnings or launch cadence or the satellite broadband business. They are buying Musk. The market's job, in that framing, is no longer to price a business. It is to price a personality, attached to a capital structure that happens to be incorporated in Texas.

The sensitivity ratio

The arithmetic is simple enough that it is worth writing down carefully. If a $1 move in the SpaceX share price corresponds to roughly $6 billion of Musk's net worth, then a 10% move in SpaceX — at the recent valuation levels reported across the secondary markets in 2025 and 2026 — is a re-rating event on the order of $100 billion or more. That is not the sensitivity of a public company to its own earnings. That is the sensitivity of a sovereign wealth fund to a single line item.

This is what makes the ratio a story in its own right. A normal large-cap public company with a $3 trillion market capitalisation will see its chief executive's net worth move by roughly $300 million for every $1 move in the share price — assuming the executive owns one tenth of one percent of the float. For the founder of a closely held company with a controlling stake and no public float, the ratio is higher. For Musk specifically, with SpaceX being his single largest concentrated asset, the ratio is at the upper bound of what the structure can produce. The Bloomberg figure of $6 billion per dollar is not, in isolation, surprising. It is the arithmetic of concentration applied to a very large asset.

What is new is the willingness of mainstream commentators to talk about the ratio in those terms. Jim Cramer, whose commentary channel has historically been a useful barometer of the way the talking-head class is reframing a story, framed the trade on 17 June as one in which the underlying earnings of SpaceX were not the operative variable. The frame was Musk himself — the perceived trajectory of his attention, his political alignments, his capacity to move the share prices of unrelated listed names through public statements. If you accept the framing, then the right way to think about SpaceX is not as a launch services provider with a Starlink unit attached. It is as the listed proxy of a single human being's reputation.

The Bitcoin comparison

The framing crystallised further when Cointelegraph's newswire picked up the second datapoint: Musk's net worth, on certain readings, having crossed the total market capitalisation of Bitcoin. The headline is technically misleading — Musk's net worth is an estimate based on private valuations and is not directly comparable to a circulating market cap — but the structural observation is correct. The largest single private fortune has, in nominal dollar terms, become coextensive with the largest single non-sovereign store of value in the digital-asset economy.

What this comparison smuggles in, whether or not the headline intended to, is the equivalence of two very different kinds of risk. Bitcoin's market cap is a public, 24-hour-a-day mark on a globally traded asset. Musk's net worth is a derivative on a private share price that is itself a derivative on a private valuation that is itself a derivative on a small number of large tender offers and secondary transactions. The two should not be compared on the same scale. But the fact that they are being compared tells you something about the way the financial commentariat now prices both.

What the market is actually pricing

The honest reading is that the SpaceX secondary market has, over the last two years, become less a market for shares in a space-transportation and satellite-broadband business and more a market for exposure to Musk's personal trajectory. The mechanical reason is concentration. Musk's net worth, by any reasonable estimate, is dominated by his SpaceX stake. The result is a feedback loop: any move in the SpaceX mark moves his net worth, which moves his visible optionality on Tesla, xAI and X, which moves those marks, which feed back into the perception of Musk.

The sub-story, and the one that is harder to price, is what this means for the businesses underneath the mark. If investors are buying Musk rather than SpaceX earnings, then the discipline that a public market typically imposes on a founder is absent. The secondary investors who set the mark are not buying voting control. They are buying the right to be on the cap table when — and only when — the company eventually lists, is acquired, or distributes shares in a tender. In that interval, the founder has fewer of the usual constraints.

There is a counter-narrative worth taking seriously. SpaceX has, on the operational metrics that can be observed from outside, performed. Launch cadence is high. Starlink is generating recurring revenue at a scale that did not exist five years ago. The company has a launch manifest and a customer base that competitors cannot match on cost. By the standards of a normal industrial company, the mark is not irrational. The question is not whether SpaceX deserves a high private valuation. The question is whether the valuation is now so disconnected from any specific operating milestone that the marginal investor has no real anchor.

Counterpoint: a working business behind the mark

The strongest argument against the personality-pricing reading is that SpaceX has, in the last 24 months, become a structurally important infrastructure provider rather than a speculative venture. Starlink's subscriber base, the cadence of Falcon 9 reuse, the Starship test programme, the volume of national-security launch contracts that have migrated to the company — none of those are story stocks. They are operating facts.

The bear case against the personality-pricing reading is that SpaceX is, in fact, a real operating business with real cash flow, and that the sensitivity ratio is simply the mechanical consequence of one large concentrated bet inside a broader fortune. The bull case for the personality-pricing reading is that the secondary mark is, by construction, illiquid, that the most recent transactions have been driven by insider tendering rather than arm's-length price discovery, and that the marginal price-setter in the secondary market is precisely the kind of investor who is buying Musk.

Stakes

The structural stakes are easy to state and hard to resolve. If the sensitivity ratio holds — if SpaceX continues to function as a private mark on a single individual's reputation rather than as an operating business — then the second-order effects are several. First, the discipline that public markets impose on capital allocation is partially absent. Second, the founders of other large private companies have an incentive to keep their companies private for longer, because the personality premium is real. Third, the wealth-concentration story that has defined American politics for the last decade finds a new mechanism: not just scale, but tradability. A private fortune that moves $6 billion on a $1 mark change is, in practice, a tradable instrument in all but name.

There is also a geopolitical layer that the 16 June datapoint does not name but that the broader context makes visible. SpaceX is the launch provider of record for the US Department of Defense and for a growing share of European and allied sovereign launches. If the company's private mark is being driven by the founder's public profile rather than by the operating business, then the cost of capital for the company is in part a function of factors that have nothing to do with the operating business and that no procurement officer can price. That is a problem the public market eventually solves through disclosure. The private market has no equivalent mechanism.

What remains uncertain

The honest caveats are several. The $6 billion sensitivity figure is reported by Bloomberg's index team and circulates through secondary channels; the underlying assumption about Musk's stake is itself an estimate. The Bitcoin-comparison headline is, strictly speaking, an apples-to-oranges comparison: a net worth estimate against a circulating market cap. The Cramer framing — investors buying Musk rather than earnings — is a characterisation of market intent, not a measurable fact. None of the source items in this story pin down the secondary-market transaction count or the identity of the marginal price-setter.

What can be said with confidence is that the structure described here is real, that it is new in its extremity, and that the financial commentariat is now openly using the personality-pricing frame to describe it. The rest is a question of whether the mark moves with the founder's reputation, or with the operating business, or with both. On present evidence, both. The question worth watching over the next twelve months is which one drives the next ten-percent move.

Desk note: the wire coverage on 16–17 June converged on two numerical anchors — the $6 billion sensitivity ratio from Bloomberg and the Bitcoin-comparison headline from Cointelegraph. Monexus has treated both as framing devices rather than as audited facts, and has given equal weight to the personality-pricing reading and to the operating-business counter-narrative.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://x.com/unusual_whales/status/123

- https://x.com/unusual_whales/status/124

- https://t.me/cointelegraph/1

- https://t.me/cointelegraph/2

- https://t.me/cointelegraph/3

- https://t.me/cointelegraph/4

- https://en.wikipedia.org/wiki/SpaceX

- https://en.wikipedia.org/wiki/Elon_Musk