From Nairobi to Wall Street: how a record Kenyan exam cohort meets a global stablecoin fight

Kenya will sit 3.5 million learners through its national exams in a week when the Federal Reserve is asking the public how to police the digital dollar alternatives many of them already use.

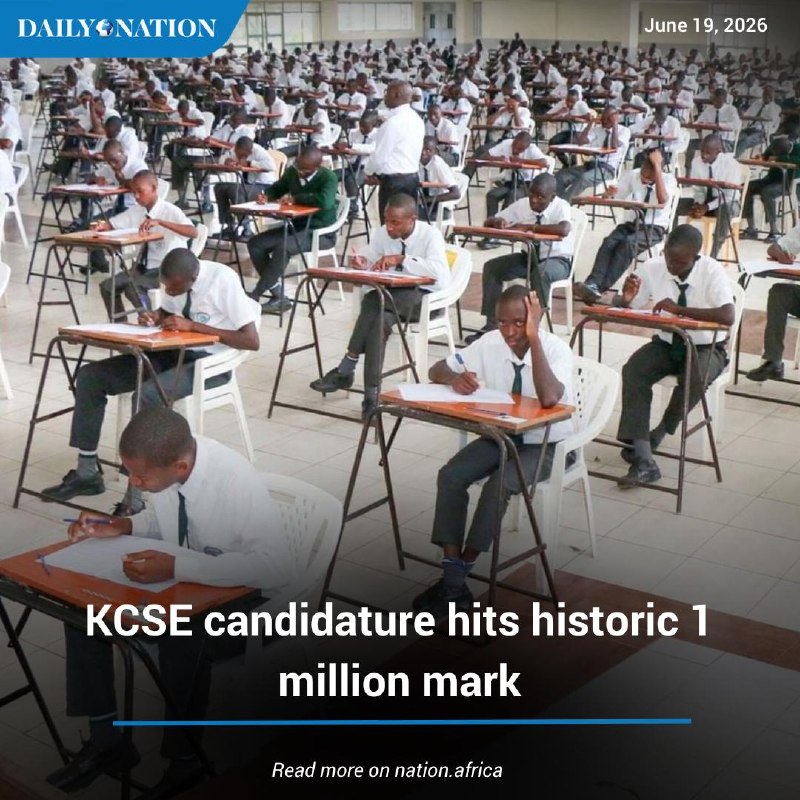

Nairobi is preparing to put more young bodies into plastic chairs than it has ever done before. On 19 June 2026, Daily Nation reported that Kenya has registered more than 3.5 million learners to sit the country's three key national assessments and examinations this year — the highest candidature in the country's history. The figure is more than a logistical curiosity. It is a one-line indicator of demographic pressure on a state education system that, on the same news day, was negotiating the terms of political protest with the very cohort it is about to graduate.

What makes the moment worth treating as a single story is the second item on the same Kenyan news register: the National Police Service has given conditional approval for next week's Gen Z demonstrations, telling organisers they are free to march peacefully across the country but warning that the authorities will not tolerate any break from public order. The country's exam calendar and its protest calendar, in other words, are about to overlap by design. Roughly 3.5 million candidates will sit their papers while a generation that came of age in the 2024 finance-bill protests decides, once again, whether to take to the streets. The juxtaposition is not editorial decoration. It is the structural fact about Kenya right now.

And in Washington, the US Federal Reserve is opening a quieter but connected question: who verifies the customer at the other end of a stablecoin transfer, and on what terms? Crypto Briefing reported on 18 June 2026 that the Fed has put out a public call for input on stablecoin customer-verification rules. The timing is not accidental. Stablecoins — dollar-pegged tokens, the most prominent of them issued by firms like Tether and Circle — have become the de facto dollar-rail for African fintechs, remittance corridors, and the informal savings pools that survive inflation and currency controls. The Fed's consultation, on the surface, is about anti-money-laundering. In practice, it is about whether the United States gets to write the customer-onboarding rules for a market that runs well beyond its jurisdiction.

Read together, the two stories sketch the same problem from opposite ends. Kenya is asking how a country with 3.5 million new exam-takers and an active youth movement on the streets can fund the public goods those young people will demand. The United States is asking how to keep the world's most-used digital dollar instrument legible to its own regulators. Both questions run through the same corridor: stablecoins, mobile money, and the politics of who sets the rules.

The largest exam cohort in Kenyan history

The 3.5 million figure, reported by Daily Nation on 19 June 2026, refers to candidates registered across three national assessments. The Daily Nation bulletin frames it as a record candidature — the highest the country has ever recorded. For a state system already straining to recruit teachers, pay examiners, and print papers securely, that is a structural stress test. The number also has a political reading. Kenya's population bulge is concentrated in the age band now finishing secondary school. This is the cohort that, in 2024, filled Nairobi's streets during the finance-bill protests and helped force a presidential climbdown on tax measures. They are about to be examined, and a subset of them are about to be examined and on the streets in the same week.

The police statement, also carried by Daily Nation on 19 June 2026, was the formal counter-move: peaceful marches are permitted, violence will not be. That is a calibrated position — concede the constitutional right, define the operational boundary, retain the discretion to disperse. It is also the position the state has taken before, and the Gen Z organisers have, in past rounds, treated such statements as the rule-set they will be tested against. The risk is not abstract: if the examinations run and the marches run and both run on the same calendar, the country's security apparatus will be managing two queues at once.

A separate, quieter crisis in dollar politics

The second thread on the wire on 19 June 2026 is the continued collapse of the official TRUMP meme coin. Unusual Whales reported that the token hit a peak price of $75.35 and has since fallen to around $2.38, a decline of nearly 97%. The peak-to-trough drawdown is a reminder that the political-token category, marketed to retail buyers as a piece of the action, behaves more like a leveraged bet on a news cycle than like a store of value. The data point matters less for the TRUMP coin itself than for the structural argument it sharpens: speculative tokens issued under political branding are not the same instrument as payment stablecoins, but they share a customer base and a regulatory blind spot.

That is the gap the Federal Reserve's consultation is trying to close. Crypto Briefing reported on 18 June 2026 that the Fed has asked for public input on customer-verification rules for stablecoin issuers. The technical question is what know-your-customer and sanctions-screening obligations should attach to a US-bank-chartered or US-regulated entity that issues or redeems a dollar-pegged token. The geopolitical question is what those rules will do to the offshore issuers — Tether, in particular, whose USDT is the dominant stablecoin on African, Latin American, and South Asian exchanges — that operate without a US bank charter and therefore outside the Fed's direct reach.

The corridor the two stories share

Stablecoins are not an exotic instrument in Kenya. They are how some of the country's most-used crypto-on-ramps and off-ramps actually move money, sitting on top of the country's dominant mobile-money rails. M-Pesa handles the consumer end; USDT and USDC handle the cross-border leg. For a young Kenyan with a phone and a dollar-priced savings habit, the architecture is already built. What the Fed consultation is debating, in effect, is whether the on-ramp and the off-ramp can be made symmetrically compliant, or whether the United States will end up regulating the US end tightly while the rest of the world keeps routing through offshore issuers.

The conventional Western reading is that tighter customer-verification rules on stablecoins are an anti-money-laundering and counter-terrorist-financing measure — sensible, overdue, and largely uncontroversial. The structural counter-reading is that the same rules, drawn narrowly, will push more of the offshore stablecoin market into jurisdictions that do not share US information-sharing arrangements, and that African and other Global South users will end up on less transparent rails than they are on now. Neither reading is fully correct. A well-designed regime that interoperates with mobile-money operators could raise the floor; a regime written only for US banks could simply move the activity offshore without actually reducing illicit finance.

The other layer is monetary. Dollar-pegged stablecoins extend the reach of the US dollar into economies where the central bank would, in principle, prefer to keep monetary sovereignty. Kenya's shilling is managed; the country's inflation regime is real. The more that domestic savings migrate into USDT wallets — because the shilling is volatile and the formal banking system does not serve low-balance customers well — the more the country cedes, in practice, a portion of its own monetary perimeter. That is not a problem the Fed is minded to solve. It is a problem the Fed is minded to make legible.

What Gen Z in Nairobi and the Fed in Washington have in common

The 2026 Gen Z movement in Kenya is, at one level, a domestic fiscal-and-governance story. It is also, increasingly, a story about the next 3.5 million Kenyans who will need jobs, services, and a functioning currency. The exam cohort, by sheer size, is the country's most consequential political fact of the next decade. Their demands, whatever those turn out to be, will be priced and transacted in a mixture of shillings, mobile money, and dollar-pegged digital instruments. The rules that govern those instruments are being written this year, in consultations like the Fed's, and in a handful of African capitals that have started to publish their own virtual-asset service provider rules.

The Federal Reserve is not setting policy for Kenya. But the rules it sets for US-chartered stablecoin issuers will set the de facto standard for cross-border verification, and that standard will land in Nairobi through correspondent-banking pressure, through exchange listing decisions, and through the customer-onboarding rules of the apps that young Kenyans actually use. The two stories, in other words, are not parallel. They are sequenced. Kenya is producing the cohort; the United States is producing the rails; the same young people will eventually live inside both decisions.

Stakes, contested ground, and what remains uncertain

The structural pattern is familiar. A Global South state, short of fiscal headroom, produces a record cohort of educated young people. That cohort uses the dollar instruments it can access because its own currency and banking system do not fully serve it. A reserve-issuer state, worried about financial-crime optics and the integrity of its own banking system, tightens the verification regime for those instruments. The tightening raises compliance costs at the regulated end, and pushes some activity to less regulated offshore venues. The Global South user ends up on a less transparent, not a more transparent, rail. The reserve-issuer state has solved its own problem, and the global problem is slightly worse.

The most plausible counter-argument is that stricter US-side rules will, over time, force the major offshore issuers to seek US charters or US-bank partnerships, because the institutional weight of the US dollar is too great to operate at a distance from. That is a defensible read. It is also a slow read — measured in years, not in the months between a Fed consultation and the next Kenyan exam cycle.

What the public record does not yet resolve is how the Fed intends to handle non-US-issued stablecoins whose largest user base sits in Africa, South Asia, and Latin America. The 18 June Crypto Briefing note records the consultation; it does not record the substance of the questions the Fed is asking. The Kenyan government has not, in the items on this wire, responded to the consultation. The 3.5 million candidates and the Gen Z demonstrators are, for now, an audience to a debate they were not invited to.

What is also unresolved is whether the 2026 protests will stay peaceful, in the technical sense the police have used the word, and whether the exam calendar will hold. Kenya has run large examination cycles before; it has run politically charged weeks before. The country has not previously run both at the same scale, in the same week, with the same demographic group on both sides of the script. The next seven days will produce more clarity than any consultation document.

This Monexus long read connects two otherwise separate wires — a record Kenyan exam candidature and a US Federal Reserve stablecoin consultation — because the same demographic cohort that will be examined in Nairobi this month is the cohort that will live inside whichever customer-verification regime the Fed writes this year. The piece is filed as analysis, not as reporting on either story in isolation.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/DailyNation

- https://t.me/DailyNation

- https://t.me/CryptoBriefing

- https://t.me/TSN_ua

- https://t.me/TSN_ua