Bitcoin at $60,000 and the quiet repricing nobody is naming

A round-number print, an $11.85 billion options expiry, and a 14,000-user AI-inference network are all telling the same story about who is left holding the bag.

Bitcoin traded through $60,000 at 13:51 UTC on 25 June 2026, according to Cointelegraph's markets desk, the first clean round-number print the asset has touched since the cycle's pre-halving peak. The number lands like a checkpoint, not a celebration, and the way the move arrived tells you more about the structure of this market than any chart does.

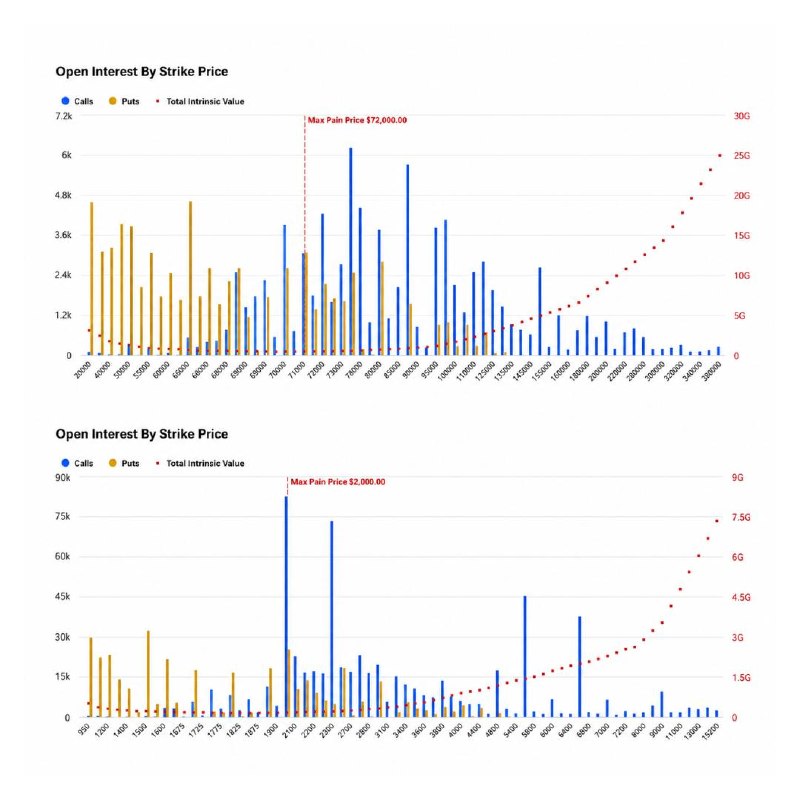

The right way to read the print is to look at the calendar two days to the right. Cointelegraph reported at 10:15 UTC the same morning that $11.85 billion in crypto options expires this Friday, with $10.16 billion of that in 162,000 Bitcoin contracts alone. With spot at $61,750 and a max-pain level that the same report flags, the path of least resistance for dealers short gamma is to pin the market near a level that maximises the pain of option buyers. A round number is a useful pin. A six-handle is an even better one. The repricing is being done, in other words, by a derivatives complex with a vested interest in keeping the tape quiet.

The round number is the message

Markets do not move on round numbers the way retail traders like to claim they do; they move on the options open interest clustered at those strikes. When $10 billion of notional is sitting on one side of a Friday expiry, the gravitational centre for the next forty-eight hours is not the news flow or the spot order book. It is the dealer hedging flow. The Cointelegraph research note is unusually frank about this: it names the notional, names the contract count, and names the price at which the maximum number of contracts expire worthless. The market is being steered, gently, toward that price by participants who are paid to manage exactly that steering.

The honest read of a $60,000 print, on the data available at 13:51 UTC, is that it is an interim settlement, not a verdict. Anyone telling you that the bear market is over because the round number held is reading the tape backwards. The round number held because a specific expiry created a specific incentive to hold it. A week on the other side of Friday, with the gamma unwind complete, the same level will mean something different.

What the AI-inference crowd is telling you, by accident

In the same news window, Cointelegraph's coverage of decentralised AI inference flagged a network called DGrid with 14,000-plus paid users running on-chain quality verification, a category the report notes "didn't exist two years ago." That detail is doing a lot of work. It tells you where the marginal dollar of crypto risk-tolerance has been migrating while the Bitcoin tape has been flat. The capital that was once levered long spot is, increasingly, being deployed into infrastructure plays where the marketing is built around the words "decentralised," "on-chain," and "AI." Those three words, stacked, are the crypto equivalent of a jingle: they bypass the part of the brain that asks for revenue.

The structural point is that the 14,000 paid users are not the story. The story is that they exist at all, two years into a bear market, with no spot-driven wealth effect to recruit them. Demand for these products is being generated by the products themselves, not by the broader market. That is either a sign of a maturing sector with its own internal demand curve, or it is a sign that the marginal buyer has stopped pricing cycles and started pricing narratives. Both readings are unflattering in their own way, and both are, on present evidence, partly true.

The counter-narrative is thinner than usual

The bullish case for a $60,000 print is that the spot market has absorbed the ETF outflows, the miner capitulation, and the regulatory chill of the past eighteen months, and is now ready to re-rate on the back of the next halving-quadrant supply shock. There is a real version of this argument. The Cointelegraph research note is careful to flag that the open interest is heavily skewed, that a clean break above the max-pain level would force a gamma squeeze to the upside, and that the historical pattern around post-halving quarters has, more often than not, rewarded the patient long.

None of that is the dominant frame, though, because the dominant frame is mechanical, not narrative. The market is being run, for the next forty-eight hours, by dealers who want a quiet tape, and the round number is the deliverable. If you are positioning around a print, you are positioning around the expiry, not the spot. Anyone telling you otherwise is selling you a story they would not personally underwrite.

The stakes, plainly stated

If the $60,000 level holds through Friday's expiry, the derivatives complex re-prices the next leg higher and the spot market is granted permission to start acting like a bull market again. If it doesn't hold, the same flow that pinned the level inverts, and the next stop is not a round number at all. The DGrid user count, in that scenario, becomes a leading indicator: a sector that raised capital on the promise of a recovery that failed to materialise is a sector that has to find its own demand, fast.

The honest position, on the information available at the time of writing, is that the $60,000 print is a derivative artefact with a Friday deadline, and the real story of the next quarter is being written on the demand side, not the price side. The market has not broken out. It has been pinned. There is a difference, and the difference is, on present evidence, the only thing worth trading.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/cointelegraph/12345

- https://t.me/cointelegraph/12346

- https://t.me/cointelegraph/12347