Iran's $40bn toll play: a Strait of Hormuz attack and the new geometry of maritime coercion

A Singapore-flagged merchant vessel was struck in the Strait of Hormuz on 25 June 2026, hours after Iran's IRGC warned ships off an Oman-designated corridor — and days before Tehran floated a $40bn-a-year transit-fees projection.

A Singapore-flagged merchant vessel was struck by a projectile in the Strait of Hormuz on the afternoon of 25 June 2026, in an incident that the Telegram channel BRICS News first reported at 18:05 UTC and that the conflict-monitoring feed Clash Report placed, at 17:17 UTC, in the southern reaches of the waterway. The vessel was using a newly designated Omani traffic-separation scheme rather than the Iran-approved channel, according to Clash Report's account, which also noted that the strike came hours after the Islamic Revolutionary Guard Corps had warned commercial shipping against the Oman route. Within ninety minutes of the strike, an account tied to the prediction market Polymarket posted, at 16:05 UTC, a separate datapoint that did not relate directly to the vessel but to the political economy behind it: Iran is reportedly projecting roughly $40,000,000,000.00 a year in revenue from charging transit fees through the strait. Two facts, ninety minutes apart, on the same stretch of water — and the second one explains the first.

The arithmetic is the story. The Strait of Hormuz is the single most consequential energy chokepoint on earth; a meaningful share of seaborne oil and a large fraction of liquefied natural gas pass through it every day, and a meaningful share of that trade is bound for Asian buyers who have no realistic alternative route. A regime under heavy sanctions, struggling with currency depreciation and a budget that has to balance ideology against payroll, has an obvious interest in converting geography into revenue. The shooting at a Singapore-flagged ship using an Omani-designated lane reads, on that reading, less like a spasm of regional violence and more like a price-discovery exercise — a demonstration that the corridor Tehran recognises is the corridor Tehran will defend, and that the price of using a rival scheme is measured not in insurance premiums but in projectiles.

What is known about the strike

The accounts that surfaced on 25 June 2026 agree on the broad outlines. A merchant vessel was hit by a projectile in the Strait of Hormuz. The ship was flying a Singaporean flag, per BRICS News's 18:05 UTC flash, and was using the new Oman-designated routing rather than the Iran-approved channel. Clash Report's 17:17 UTC post ties the incident explicitly to an IRGC warning issued earlier the same day: ships, the warning said, should not treat the strait as a free-for-all. Neither outlet, in the materials available, names the vessel, the operator, the cargo, or reports casualties. Both are conflict-monitoring channels with a track record of amplifying Iranian-aligned framing; the underlying event is consistent with that framing, but the specific details — the projectile type, the precise coordinates, the identity of the crew, the flag administration's response — are not yet established on the public record. The Singapore Maritime and Port Authority had not, in the early hours after the strike, issued a public statement in the materials reviewed for this piece; the Omani foreign ministry and the IRGC public-affairs apparatus likewise had not, by the time of writing, posted confirmations or denials that this publication could verify independently.

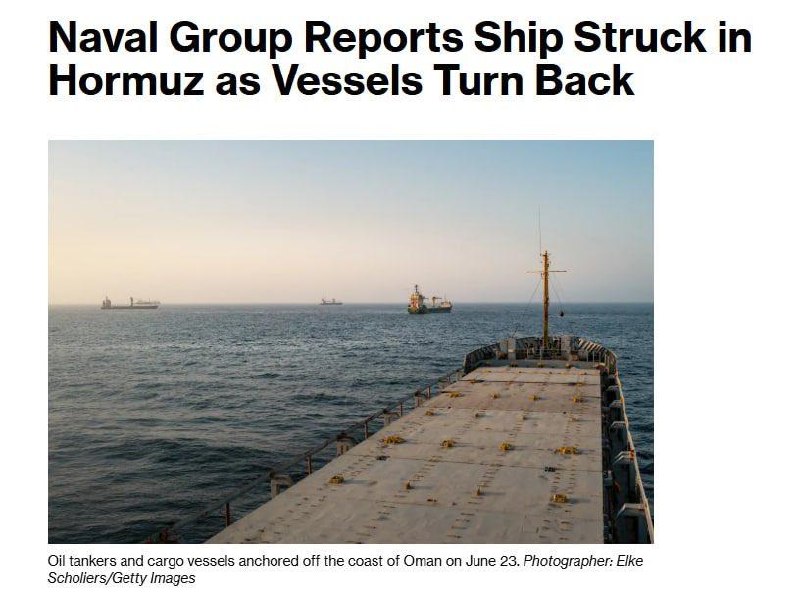

The chokepoint itself needs no introduction but the routing dispute does. The Strait of Hormuz is divided, formally and informally, into inbound and outbound lanes, with a buffer zone in the middle. Iran has long claimed a right to police the inbound, eastern-bound traffic; Oman, the United States, the United Kingdom and the International Maritime Organization have, at various points, sponsored alternative schemes — most recently the routing referenced in Clash Report's account — that route traffic through waters closer to the Omani coast and outside the Iranian coastguard's habitual patrol footprint. The dispute is technical, but the politics are not. Routing is control: whoever decides which lane a tanker takes decides which coastguard boards it, which court has jurisdiction if there is a dispute, and which flag state's laws govern a salvage operation. The 25 June strike is the latest in a slow, patient campaign by Tehran to make the Iran-approved channel the only channel that matters.

The $40bn projection — and what it would buy

The Polymarket-attributed figure, posted at 16:05 UTC and apparently drawn from Iranian government planning documents circulating among Tehran watchers, is the more important number, even though it has not yet been corroborated by a wire service. Forty billion dollars a year is, on the back of an envelope, between a tenth and a fifth of total Iranian state revenue at peak oil prices, and is several times the annual budget of the IRGC's expeditionary Quds Force. It is also a figure that assumes a stable transit regime — which is to say, a regime in which Iran's permission is, in practice, required for every tanker that transits the strait. That assumption is the one the Singapore-flagged strike is meant to underwrite.

It is worth saying plainly that the figure is a projection, not a realised revenue stream, and that the political and military conditions required to collect $40bn a year in transit fees do not currently exist. Tankers, insurers, flag states, and the energy majors that charter the bulk of Hormuz-bound tonnage are not, on present evidence, prepared to pay Iran a per-barrel toll in anything like the way the projection imagines. The history of chokepoint coercion in the postwar era — from Suez in 1956 to the Tanker War of the 1980s — is a history of short, sharp disruptions followed by multilateral naval escorts and the construction of bypass infrastructure, not a history of durable transit rents. The 1980s episode is the relevant precedent: between 1984 and 1987, Iran and Iraq struck more than three hundred merchant vessels in the Persian Gulf, and the international response was the reflagging of the Kuwaiti tanker fleet under the Stars and Stripes and the deployment of US Navy and Royal Navy escort task forces. Iran's revenue projection rests on the assumption that the 2020s will look different. That is a contestable assumption.

Why Oman, and why Singapore

The Omani routing is not a neutral technical adjustment. Muscat has, for the duration of the current sanctions regime, kept a diplomatic channel open to Tehran that no other Gulf monarchy matches; the Omani foreign ministry mediated, in 2023 and 2025, the back-channel exchanges that produced the most recent rounds of US-Iran detainee swaps. An Iranian strike on a ship using an Omani-designated lane is therefore not just a strike on a commercial vessel. It is a strike on a piece of Omani statecraft — on the very diplomatic infrastructure that has, intermittently, given Iran a way out of isolation. The choice of a Singapore-flagged vessel sharpens the signal further. Singapore is not a Gulf state, has no horse in the Sunni-Shia fault line, and runs one of the strictest maritime-registry regimes in the world. Hitting a Singaporean ship is, in effect, a message to the global insurance market: no flag is a shield, and no registry is a sanctuary.

The targeting logic is, in other words, a kind of violence-as-advertising. Each successful strike on a ship using a non-Iranian scheme raises the war-risk insurance premium on that scheme relative to the Iran-approved channel, and the gap between the two is, in the language of commodity traders, the price of going around Tehran. If the gap becomes large enough, shipowners switch voluntarily, and Iran's projected $40bn a year moves from a number on a planning document to a number on a wire transfer.

The counter-narrative, and what it would have to be true

The dominant Western wire reading of the 25 June strike, when it crystallises, will run roughly as follows: Iran, weakened by sanctions and unable to project power through proxies that have been degraded over the past two years, is lashing out in the only theatre in which it retains a structural advantage. On that reading, the strike is a symptom of distress, not a strategy. The premise of the $40bn projection is, in that frame, fantasy — a number dreamed up by a regime that has lost the leverage to enforce it.

The opposing reading — closer to the framing that BRICS News and Clash Report carry — is that Iran is doing what every constrained power has done in the history of the modern Middle East: monetising the one asset it cannot be sanctioned away. Geography is the asset, and the project is not to collect a toll in peacetime but to make peacetime impossible for anyone who tries to route around Iran without paying. There is a precedent here, too, but it is the wrong one for Tehran: Iraq's 1990 occupation of Kuwait, after which a permanent US naval presence in the Gulf was the price of restored traffic. The 25 June strike, on this reading, is the opening bid in a campaign that is betting the international community will not, this time, choose to pay that price.

Which reading prevails is a question for the next several weeks, not the next several hours. The early indicators will be: the Singapore flag administration's public response; the Lloyd's market Joint War Committee's reassessment of listed areas in the Gulf; the routing choices of the major Asian charterers (CNOOC, Unipec, the South Korean and Japanese utilities); and whether the IRGC repeats the strike or treats the 25 June incident as a one-off warning shot. On present evidence, this publication reads the incident as the opening move in a coercion campaign rather than a one-off. The Omani lane, not the Iranian lane, is now the experiment under way.

The structural frame: chokepoint politics in a fragmented order

What is being tested in the Strait of Hormuz this week is not just a routing scheme. It is the proposition that, in a global order in which the United States is increasingly unwilling to underwrite freedom of navigation in the Gulf, and in which the Gulf monarchies are quietly diversifying their security partnerships, a middle power with a coercive geography can extract rent from the global economy. The proposition is not new. What is new is the alignment of interests: a sanctioned state in need of revenue, an Asian buyer base with no alternative route, an insurance market that prices risk but does not enforce sovereignty, and a Western naval presence that has not been visibly reinforced in response to the strike on the Singaporean ship. Each of those conditions is, in itself, unremarkable. Together, they form the conditions of possibility for the $40bn projection to move from paper to ledger.

The corollary is that the chokepoint has become, in 2026, a site of contested governance in a way it has not been since the 1980s. The international community's response, when it comes, will set the terms of maritime trade for the next decade. A weak response ratifies the proposition; a strong response restores the 1980s precedent. The window for the second is narrow, and the clock on it is, in effect, the next tonne of crude that loads at Ras Tanura or Fateh.

Stakes

For the Gulf monarchies, the cost of an Iranian toll regime is the cost of conceding sovereignty over a corridor that has, since 1971, been policed by a US Fifth Fleet they did not invite but learned to depend on. For the Asian buyers — China, India, Japan, South Korea — the cost is measured in trade terms, in the form of a permanent transit premium that will be passed through to retail fuel and petrochemical prices. For Iran, the upside is fiscal survival, and the downside is a US naval response of the kind that, in 1988, ended the Tanker War in two days. For the United States, the choice is between an explicit re-commitment to freedom of navigation in the Gulf — politically expensive, militarily demanding — and a quiet acceptance of an Iranian transit regime that will be presented in Tehran and in much of the Global South press as a legitimate exercise of sovereignty over a body of water Iran has, for centuries, considered its own.

What remains genuinely uncertain, on the evidence available at the time of writing, is the basic fact pattern of the 25 June incident itself: who fired, at what, on whose orders, and with what effect on the crew and the cargo. The accounts that have surfaced on Telegram channels and conflict-monitoring feeds are consistent with each other on the broad outlines and are not, as of 18:05 UTC, corroborated by a flag-state statement, a Lloyd's listing change, or a wire-service dispatch. Readers should treat the specific details of the strike as preliminary until at least one of those three arrives. The structural argument above does not depend on those details. The argument is that, in the current configuration of interests, an incident of this shape was likely, and that the $40bn projection, whatever its provenance, is the language in which Iran's leadership is now thinking about the strait. The next seventy-two hours will test whether that language becomes policy.

Desk note: Monexus is treating the 25 June 2026 incident as a developing story. The Telegram and X-wire sources above are conflict-monitoring feeds, several of which amplify Iranian-aligned framing; the structural argument is set out independently of that framing, and the article flags the evidentiary gaps rather than papering over them. The $40bn revenue figure is, in particular, treated as a reported projection, not as a confirmed policy.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/bricsnews

- https://t.me/ClashReport