Hormuz traffic has collapsed to wartime lows — and the MoU is barely moving the needle

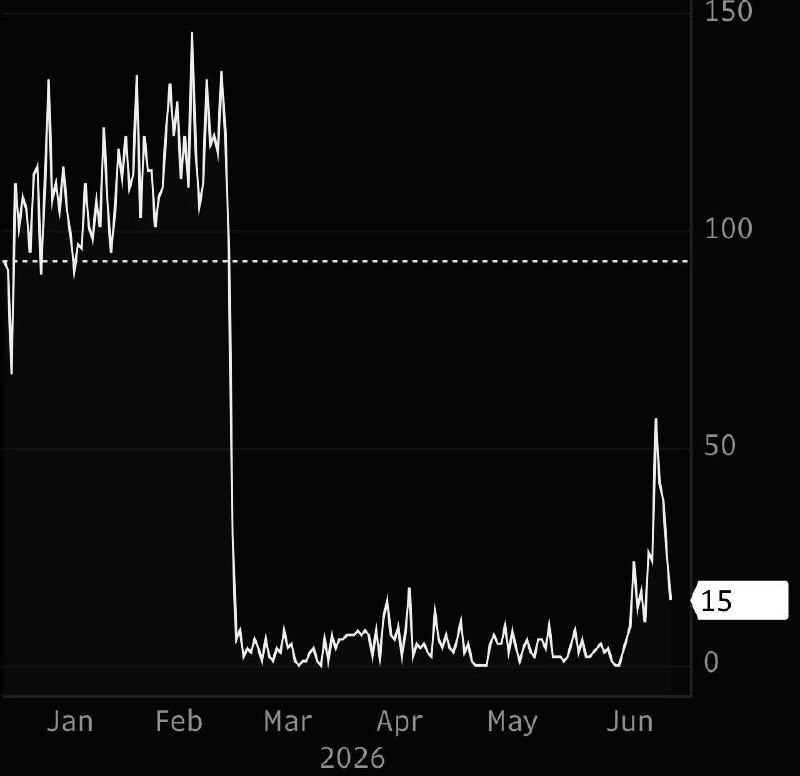

Vessel transits through the Strait of Hormuz have fallen to roughly 5–10 a day, the level seen during open war, according to a Middle East Spectator wire dated 29 June 2026 — and a freshly cited memorandum of understanding has lifted that figure only to 15–20.

The Strait of Hormuz — the 21-nautical-mile-wide corridor between Iran and Oman through which roughly a fifth of seaborne oil normally moves — is operating at wartime lows. On 29 June 2026 at 16:22 UTC, the Middle East Spectator wire reported that daily vessel transits had fallen to approximately 5–10 ships a day, the same level recorded during active hostilities, and that a freshly cited memorandum of understanding had lifted that figure only to 15–20. By any commercial standard, those are not the numbers of a settled waterway.

The headline here is not the MoU. It is that a diplomatic instrument described as easing tensions has, on the evidence available so far, done little to put commercial shipping back on the water. The chokepoint sits at the centre of the global energy map, and the price of its reopening is being paid in transit volumes, insurance premiums and the silence of hulls that would otherwise be transiting.

What the wires actually say

The Middle East Spectator dispatch frames the collapse in the bluntest possible terms: traffic has fallen to a wartime baseline, and the MoU has nudged transits up from roughly 5–10 vessels a day to 15–20. That is the entire delta the agreement appears to have produced on the water. Separately, at 08:22 UTC the same day, a Polymarket-flagged alert surfaced a warning from the chief executive of NYK, one of Japan's largest shipping lines, that mines have left safe routes through the strait "extremely limited." Read together, the two messages sketch a picture of a corridor that is technically passable, diplomatically de-escalated on paper, and operationally still treated as a war zone by the underwriters and operators who actually move the cargo.

There is no public, independently verified count of transits against either figure. The Middle East Spectator numbers are the wire's own; they have not been cross-checked against Lloyd's List Intelligence, TankerTrackers or port-state control data in the materials available to this publication. Treat the 5–10 and 15–20 ranges as directional, not audited.

Why the gap between paper and tonnage

Three mechanics explain why an MoU can coexist with a wartime shipping profile. First, mine risk is sticky. A single confirmed or even plausibly rumoured moored contact mine raises war-risk insurance premia for an entire fleet, and carriers react by rerouting, slowing or simply parking hulls until the threat is independently cleared. NYK's chief executive is naming that dynamic in public, which is itself a signal: shipping lines do not editorialise about route safety unless their operators are refusing to transit. Second, scheduling is path-dependent. Even if the political temperature drops tomorrow, the container and tanker networks that serve Gulf ports run on multi-week port-call rotations; restoring a normal pattern from a wartime trough takes weeks of consistent signalling, not a single communiqué. Third, the MoU itself is described only at the level of a maritime-traffic adjustment. Neither the text nor the parties to the agreement have been published in the materials available to this publication, which means commercial operators cannot price what has actually changed.

This is the gap the mainstream coverage is missing. Diplomatic choreography and commercial recovery are not the same event, and they do not move on the same clock. A deal that frees political airspace without producing a verifiable de-mining regime, an insurance reassessment and published guarantees of safe passage will look, to a shipowner in Tokyo or a charterer in Rotterdam, like a press release.

Counter-read: the MoU is the precondition, not the outcome

The counter-narrative, and the one Tehran has an interest in promoting, is that the MoU is the precondition for normal traffic, not the trigger. Under that reading, the 5–10-to-15–20 lift is the first measurable step on a curve that has further to climb; what matters is the direction, not the absolute level. Iranian state-aligned outlets are expected to frame any de-escalation in those terms, and the structural logic — confidence building before commercial normalisation — is not unreasonable. De-mining operations, shipping-insurance repricing and the publication of safe-passage protocols all take time, and there is a defensible argument that none of them can begin until the political settlement is visible.

The counter to that counter is operational. Operators do not wait for ideal conditions; they wait for the absence of acute, uninsurable risk. Until the mine threat is verifiably cleared — not merely acknowledged in a memorandum — war-risk premia will stay elevated, and elevated premia are themselves a tax on transit that suppresses volume. The Polymarket-flagged NYK statement is the clearest available evidence that the commercial side still considers the risk unpriced.

Stakes

If the trajectory holds, the bill lands in three places. Gulf hydrocarbon exporters lose the discount that insurance premia and freight rates already impose on their barrels relative to Brent. Asian importers — China, India, Japan, South Korea — absorb the freight differential on every cargo they cannot reroute via Sumed or Cape of Good Hope routings. And the United States, which has publicly traded diplomatic movement in the Gulf for concessions elsewhere, finds that the political asset it has purchased cannot be cashed until the water is actually safe to cross.

What remains genuinely uncertain is the gap between the Middle East Spectator's 5–10 figure and any audited transit count. The Polymarket-sourced NYK warning is qualitatively different from a tonnage figure: it is an operator's view of mine risk, not a measurement of throughput. Until a Lloyd's List, TankerTrackers or port-state dataset confirms the wire's range, the 15–20 ceiling should be read as the upper bound of a diplomatic floor, not as evidence of recovery.

Desk note: This article treats the Middle East Spectator wire as the primary quantitative claim and the Polymarket-flagged NYK CEO statement as the operator-side counterweight, reflecting how the sourcing actually arrived on the desk. Where independent transit data has not yet been published, this publication has said so rather than smoothing over the gap.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/Middle_East_Spectator

- https://x.com/polymarket/status/