Europe's Ukrainian refugee count ticks up again as temporary protection rolls into a fifth year

EU-wide monthly data show temporary-protection registrations rising in 22 of 26 member states in May, with Poland still hosting the largest share of Ukrainians displaced since February 2022.

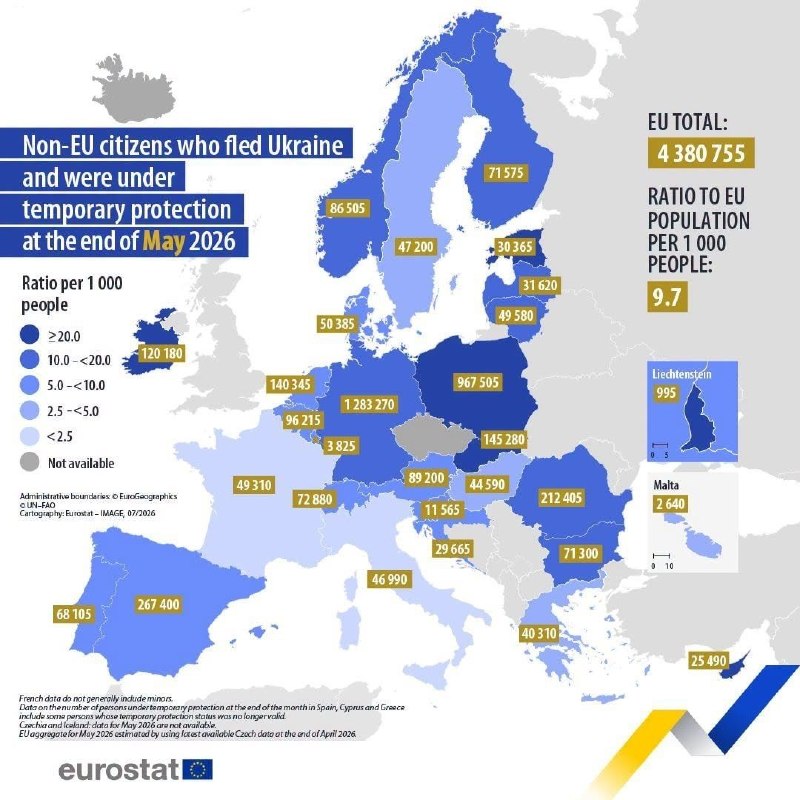

The European Union's statistical office recorded another monthly rise in the number of Ukrainians holding temporary protection status across the bloc in May, according to Eurostat figures circulated on 11 July 2026 via the Telegram channel DDGeopolitics. The dataset covers the 26 EU countries reporting that month and shows registrations climbing in 22 of them — a quiet but persistent reminder that displacement from Russia's full-scale invasion shows no sign of reversing, even as headlines move on to other crises.

The monthly tick is small. The political weight is not. Five years after the invasion that began on 24 February 2022, the EU's temporary-protection directive — activated for the first time ever in response to a mass displacement event — is still the legal scaffolding holding millions of lives in place. That the count is still rising rather than falling says something important about the war's trajectory and about Europe's institutional choice to keep the door open rather than force returns into an active conflict zone.

The shape of the distribution

Poland remains the single largest host country for Ukrainians with temporary protection, continuing a pattern established in the spring of 2022 and consolidated by Warsaw's early decision to issue national ID numbers (pesel) and grant near-immediate access to the labour market and to public services. Germany and the Czech Republic follow as the next-largest recipients, with the Baltic states — Lithuania, Latvia and Estonia — continuing to record some of the highest per-capita concentrations in the bloc. Mediterranean member states, which absorbed a much smaller share of the initial 2022 wave, have seen the slowest growth in subsequent months.

The Eurostat series captures only beneficiaries of the temporary-protection directive, not the larger universe of Ukrainians resident in the EU on other legal grounds — students, workers on national visas, family-reunification cases. The directive's headline number is therefore a floor, not a ceiling, on the real Ukrainian population living under EU jurisdiction. Eurostat does not publish a single consolidated estimate of that wider figure in the monthly series.

Why the count is still climbing

Three forces are pushing the May numbers up. First, ongoing attrition in front-line regions continues to produce new outflows, with people moving from already-displaced status inside Ukraine to international protection abroad. Second, the directive's automatic extension — it has been renewed through successive Council decisions, most recently extending validity into 2027 — removes the legal cliff-edge that would otherwise force beneficiaries to convert status or leave. Third, a steady stream of Ukrainians who initially sheltered in non-EU countries such as Moldova has been re-routing into the bloc as the limits of longer-term stay in those transit states become visible.

The 22-of-26 majority is itself a political signal. In every member state where the count rose, national authorities chose — implicitly or explicitly — not to push beneficiaries toward return. That choice carries costs: housing market pressure in mid-sized Polish and Czech cities, school enrolment strain, and competition for social housing in capital regions that pre-dated February 2022. Those costs are real and well-documented in domestic press reporting, and they are surfacing in local electoral politics. But the dominant policy frame across the EU has remained one of continued reception, not managed return.

The structural frame

The directive in force today is the same legal instrument the Council activated in March 2022 — a piece of legislation drafted in the early 2000s and never used until Russia's invasion made it operational. Its design choice — group-based rather than case-by-case protection, with renewable validity and immediate rights to work, healthcare and education — was deliberately calibrated to avoid the delays and the asylum backlogs that had defined earlier European responses to mass displacement. The fact that the system has absorbed multiple years of arrivals without the kind of visible humanitarian breakdown seen in 2015-16 is, on its own terms, a measurable policy success.

The counter-current is harder to read. Several member states have tightened access to family-reunification benefits and to long-term social housing in the past 18 months, and at least two have signalled interest in a graduated framework that would distinguish between Ukrainians able to support themselves and those needing continued state support. Neither move is a withdrawal from the directive; both are quiet recalibrations of the welfare settlement attached to it. The May data, on their own, cannot tell us whether the next fiscal year will mark a turning point toward managed return — that decision sits in national capitals, not in the Eurostat release.

What to watch next

Two dates will clarify the trajectory. The Council is expected to revisit the directive's validity horizon later this year, and any extension beyond the current 2027 envelope will be the first hard signal of how long EU governments expect the protection regime to remain operational. The second is the next round of EU-wide returns monitoring — a much smaller and more contested dataset, but the one that would show whether the May uptick in registrations is matched by any meaningful outflow in the other direction. Neither release is imminent, but both are now the right place to look.

The uncertainty worth naming is the absence of a unified figure for the total Ukrainian population in the EU. The temporary-protection series is clean, monthly and EU-wide; the broader population — students, workers, family cases, undocumented arrivals who never registered — is not. Any argument about the political sustainability of Europe's response rests on that wider denominator, and Eurostat does not provide it.

This piece draws on the Eurostat release summarised by DDGeopolitics on 11 July 2026. Monexus frames the monthly tick as a continuation of an established policy choice rather than a new crisis, in contrast to wire coverage that has tended to treat each rise as a discrete emergency.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/DDGeopolitics