Volkswagen's 8.6% Q2 slide puts the German industrial model in China's crosshairs

A 36.6% collapse in Chinese deliveries exposes how decisively the global car industry's centre of gravity has moved, and how poorly Europe's legacy champions are positioned to follow it.

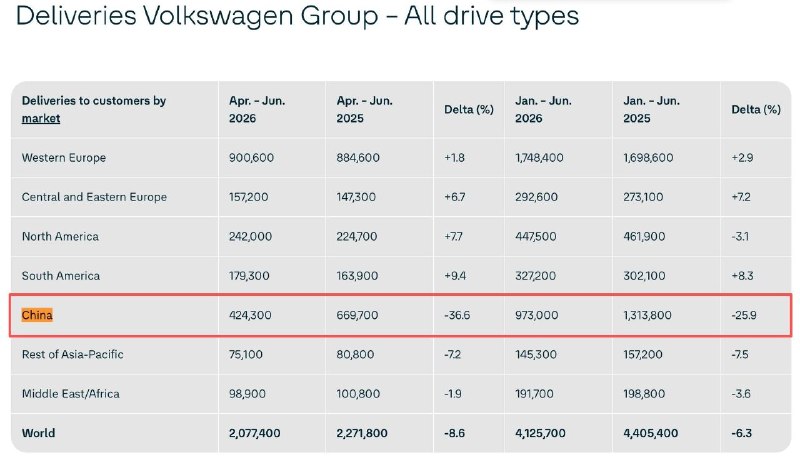

Volkswagen delivered 8.6% fewer cars worldwide in the second quarter of 2026 than a year earlier, the German automotive group reported on 11 July, with the collapse in its largest single market, mainland China, running at 36.6%. The single-country slide is roughly four times the global average, and it lands at a moment when Wolfsburg's domestic Chinese rivals are scaling faster than at any point in the industry's history.

The numbers are not an accident of consumer taste. They are the working-out of a decade of Chinese industrial policy that has built battery, software, and整车 manufacturing capacity on a scale no European volume player can match, while Europe's own EV ramp has been slowed by subsidy disputes, charging build-out delays, and the slow puncture of its supplier base. Volkswagen's Q2 print is the clearest public confirmation so far that the German industrial model, long the benchmark for the global auto industry, is being repriced by the Chinese market on Chinese terms.

What the 36.6% actually measures

China has been Volkswagen's profit engine for two decades. The group's joint ventures with FAW and SAIC once delivered margins that propped up the entire European balance sheet, funding factory investment in Zwickau and Emden and underwriting the diesel-to-EV transition that is now, by Wolfsburg's own admission, running behind schedule. A 36.6% fall in deliveries against a year-ago base that was already weak is not a quarterly wobble. It is structural erosion, concentrated in exactly the segments where Chinese brands are most price-competitive: compact EVs and family saloons priced between roughly 150,000 and 250,000 yuan.

The Telegram channel two_majors, which flagged the figures on 11 July 2026, framed the slide as confirmation that German automakers are losing ground in their "main market". That phrasing matters. China was, until recently, the market German executives went to when European demand stalled. It is now the market where their pricing power, product cycle, and brand premium are being tested by BYD, Xiaomi, Geely, NIO, and a long tail of domestic challengers that did not exist as volume players five years ago.

The Chinese counter-frame

Read from Beijing, the same numbers tell a different story. Chinese industry framing, carried in outlets from the South China Morning Post to Global Times, points out that the 8.6% global drop is partly a function of Volkswagen's own choices: a delayed EV rollout, software problems in the ID series, and an overly cautious approach to local software stacks that left the brand dependent on Western architectures unsuited to Chinese consumer expectations on cockpit electronics and over-the-air updates. On this reading, the German fall is not a victory of Chinese industrial policy per se but a competitive correction in which domestic brands such as BYD have executed better on the specific things Chinese buyers now value: fast charging, integrated infotainment, and aggressive pricing.

There is weight to that argument. Volkswagen's troubles in China are real, but they coexist with a market in which total vehicle sales have continued to expand in the first half of 2026, and in which joint-venture brands from Toyota to General Motors have also lost share. The fairest reading is that the 36.6% slide reflects both a Volkswagen-specific execution problem and a broader rebalancing toward Chinese OEMs that has been visible for at least three years.

What an 8.6% global number actually hides

The Wolfsburg headline figure flatters the underlying picture. An 8.6% worldwide drop, against a backdrop of rising global EV volumes, implies that Volkswagen is losing share almost everywhere it sells. The North American market has been a stubborn drag since the dieselgate years. Europe is contested by a wave of Chinese imports now subject to EU countervailing duties, and by Tesla's price cuts. South America, where Volkswagen retains a strong brand, cannot offset what is happening in Asia.

The structural issue is fixed-cost absorption. A carmaker with German labour costs, German pension liabilities, and a plant network built around combustion-era volume cannot run at 85% of capacity and earn its cost of capital. Each percentage point of lost China volume has a multiplier effect on group operating margin, because the Chinese joint ventures historically carried the highest contribution per vehicle. Strip that out, and the entire European cost base has to be renegotiated, with all the political consequences that follows in Saxony, Lower Saxony, and the federal chancellery in Berlin.

Stakes for Berlin, Brussels, and Beijing

For Berlin, the print strengthens the case Chancellor Merz's government has been building for a more aggressive industrial-policy response: faster permitting for gigafactories, a third round of EV purchase incentives, and a softening of the EU's anti-subsidy posture toward Chinese imports in return for joint-venture concessions. For Brussels, the same numbers feed into the live debate over countervailing duties on Chinese EVs, where German producers are split between those who want protection and those whose Chinese partners want continued market access. For Beijing, Volkswagen's weakness is a useful data point but not a strategic surprise. The country already accounts for roughly 60% of global EV production, and its domestic OEMs are now exporting from Thailand to Brazil. A weaker Volkswagen does not change the trajectory. It only confirms it.

The uncertainty that remains is timing. Volkswagen's own guidance suggests a stabilisation in the second half of 2026 as new models reach Chinese showrooms, and as the group's software joint venture with XPeng begins to deliver vehicles with cockpit features tuned to local expectations. Whether 2026 ends as a trough or as the start of a longer slide will depend on those launches. The 11 July print does not answer that question. It does, however, answer an older one: the global car industry's centre of gravity has moved, and Europe's flagship volume brand has now put that move on its own quarterly disclosure.

How Monexus framed this: where wire coverage has tended to treat the 8.6% global figure as the headline, this piece treats the 36.6% China figure as the structural story, and gives the Chinese industry framing equal weight to the German management line.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/two_majors