Strategy's 32-Year Bitcoin Dividend and the Taxman Coming for Illinois

Three signals in 24 hours — a corporate treasury claiming a generational bitcoin runway, a state-level transaction tax, and a Federal Reserve holding pat — sketch a sharper map of where US crypto policy actually lives.

On 17 June 2026, three announcements landed within four hours of one another, and the spacing matters. At 17:40 UTC, Illinois lawmakers passed a 0.2% levy on bitcoin and crypto transactions, due to take effect in 2027 and already drawing the label of the most punitive digital-asset tax in the United States. Twenty minutes later, at 18:00 UTC, the Federal Reserve held interest rates steady. By 21:20 UTC, Strategy — the MicroStrategy-rebranded corporate treasury that has made bitcoin its balance sheet — was telling markets that its bitcoin reserve provides enough coverage to support dividend payments for the next 32 years. Each item is, on its own, a piece of trivia. Together, they sketch a map.

The map is this: US digital-asset policy is no longer being written in Washington. It is being written in Springfield, Illinois; in the price action of bitcoin against a Federal Reserve that refuses to move; and inside the earnings statements of a single publicly listed company that has, in effect, become an unregulated bitcoin holding company with a software business attached. If you want to know what the next decade of American crypto looks like, those are the three coordinates to watch.

Springfield as the new front line

Illinois's 0.2% transaction levy — described in early coverage as the most punitive digital-asset tax in the country — is small in percentage terms and enormous in signal value. State-level transaction taxes are the policy instrument Washington has so far refused to deploy. The federal approach has been disclosure rules, accounting guidance and a slow-motion fight over whether most tokens count as securities. A transactional levy cuts through all of that. It treats every on-chain transfer, swap or stablecoin movement as taxable event infrastructure, and it raises revenue in proportion to activity rather than to capital gains realisation.

The counter-narrative is straightforward and worth airing. Critics who framed the measure as punitive are, in many cases, the same voices who have spent five years arguing that crypto needs to "come inside the regulatory perimeter." A small, predictable transaction levy is, structurally, exactly that: a perimeter, with a price of entry. It is what state governments do when they want to normalise an industry without outlawing it. The case for the tax is that digital-asset activity now generates real economic throughput — node operators, mining capacity, exchange payroll — and that throughput should be taxed the way retail transactions, brokerage activity and ATM withdrawals already are.

The case against is more interesting. Transaction taxes distort behaviour at the margin. In equities, the equivalent instrument — the financial-transaction tax — has a long history of academic critique and a short history of political survival. Illinois is not the European Union; capital and nodes will move to neighbouring states and to decentralised infrastructure that does not see state borders. If the goal is revenue, the elasticity of crypto transaction volume is the variable to watch. If the goal is signalling — telling the industry that public-chain finance is now ordinary commerce — the tax succeeds on day one regardless of what it raises.

The Fed's patience, and what it costs

The Federal Reserve's decision on 17 June to leave rates unchanged is, by mid-2026, no longer news in itself. It is the underlying condition. A held rate combined with elevated inflation in services means the real cost of holding non-yielding assets — including bitcoin — has tightened even as the nominal cost has not. That is why corporate-treasury disclosures about bitcoin runway matter more than they would in a cutting cycle. The price of holding is doing the work that interest rates used to do.

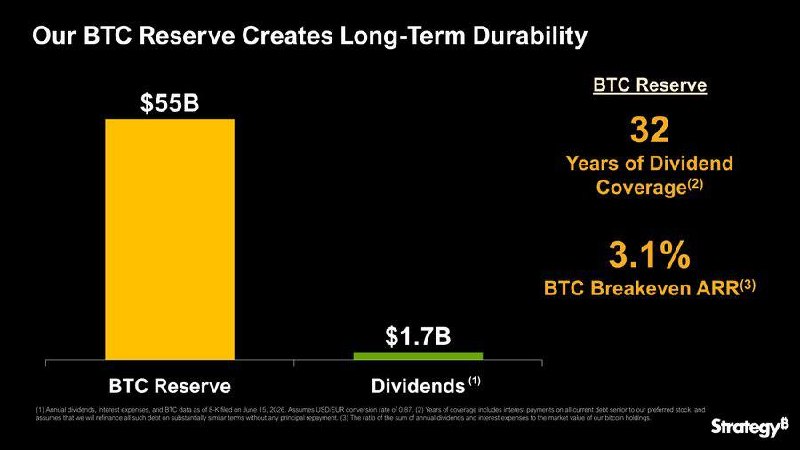

Strategy's 32-year dividend-coverage claim is the kind of number that should be read with a long cool stare. It rests on a stated reserve figure, a stated dividend obligation and a stated assumption about bitcoin's future value. The first two are auditable. The third is not. The honest reading is that Strategy has enough bitcoin, at current prices, to cover a known dividend liability for a long time — and that the company's equity will trade as a leveraged bitcoin proxy for as long as that arithmetic holds. The dishonest reading, which will dominate crypto Twitter for the next 72 hours, is that the company has "made bitcoin safe." It has not. It has made a balance sheet.

The structural picture, in plain prose

What the three announcements together describe is the slow unbundling of digital-asset policy from any single centre of authority. Treasury handles sanctions and accounting. The SEC handles disclosure. The Fed handles the cost of money. And now individual states — beginning, plausibly, with Illinois — handle the price of using the rails. That is a more honest architecture than the one the industry spent 2021-2024 demanding, which was a single federal regulator who would bless everything and tax nothing. The new architecture taxes at the edges, regulates at the centre, and lets the Federal Reserve do what central banks do: move slowly, signal deliberately, and force every other actor to price around it.

A more sceptical reading is also available. A patchwork of state transaction taxes, a passive Fed and a corporate treasury using its own share count as a bitcoin proxy is not a policy framework. It is what policy looks like when no one is in charge. The industry will adapt by routing activity through low-tax jurisdictions, by using decentralised exchanges that do not see state borders, and by treating the Illinois levy the way early Bitcoin users treated New York's BitLicense: a cost of doing business in a particular state, not a national rule. Whether that turns out to be a feature or a bug depends on which side of the statehouse you sit on.

What to watch next

Three things, in order. First, the implementation text of the Illinois levy — what counts as a "transaction," whether self-custody transfers are in scope, and whether mining and validation rewards are taxable events. Those drafting choices will determine whether the tax is a precedent or a curiosity. Second, the next two Consumer Price Index prints, because a held Fed is a Fed that is watching the data, and a hot services print will push the real cost of holding non-yielding assets higher. Third, Strategy's next 10-Q. The 32-year figure will be stress-tested by auditors, by short-sellers and by a Securities and Exchange Commission that has shown, in recent quarters, a new appetite for treasury-disclosure review. The claim is auditable. The audit has not yet happened.

None of this resolves the deeper question — whether public-chain finance becomes ordinary infrastructure, with ordinary taxation, or remains a parallel system routed around ordinary taxation. The signals from 17 June point in both directions at once. Illinois is bringing it inside. Strategy is building a balance sheet that assumes it stays inside. The Fed is doing nothing, which is its own kind of endorsement.

This publication reads the 17 June cluster as evidence that US crypto policy is fragmenting by design — federal posture, state revenue and corporate treasury each pulling in different directions — rather than converging on a single regime.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph

- https://t.me/s/cointelegraph