A Two-Week Truce, Not a Settlement: How the US-Iran Ceasefire Holds the Strait of Hormuz Together

A reported US-Iran agreement to halt strikes and continue negotiations has bought the Strait of Hormuz a brief reprieve, leaving oil markets and Gulf shipping to weigh relief against the underlying instability.

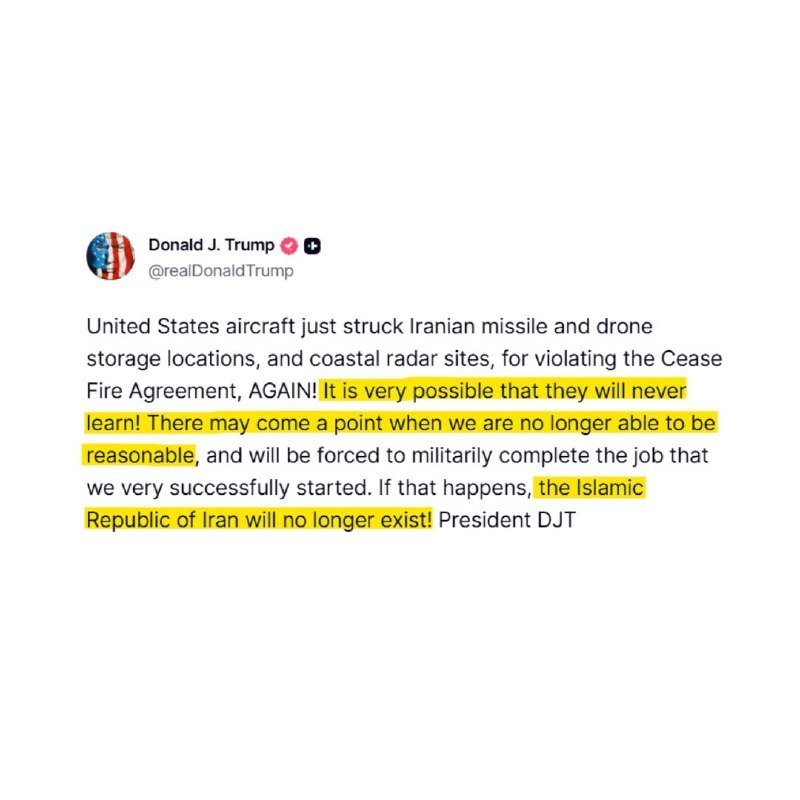

At 05:24 UTC on 29 June 2026, the open-source channel OSINTdefender reported that the United States and Iran had agreed to halt strikes and continue negotiations. The two-line bulletin, repeated across the channel's main feed and chat room, carried no operational details, no declared ceasefire architecture, and no third-party verification beyond the channel's own aggregation. It nonetheless landed on screens already jittery from a fortnight of escalation that had pushed crude prices higher, with shipping through the Strait of Hormuz repeatedly disrupted by tit-for-tat strikes between Washington and Tehran.

What has been announced, on the evidence available at publication, is a pause, not a settlement. The distinction matters because the same body of water that carries roughly a fifth of seaborne oil is now functioning as both arena and arbiter. A pause that holds for days can ease insurance premiums; a settlement that fails can do far more damage than the original quarrel. Monexus finds that the operative question for markets and governments is not whether negotiations will resume — both sides have said they will — but whether the chokepoint itself becomes a permanent participant in the talks.

What the open-source record actually shows

The only confirmed developments in the public record on the morning of 29 June are the cessation of strikes and the resumption of a negotiating track. OSINTdefender's 05:24 UTC post is the clearest statement of that arrangement, framed as an agreement between Washington and Tehran to stop mutual strikes and continue talks. There is, as of publication, no joint communique, no signed framework, no name attached to the channel of communication, and no timetable for the next round.

Markets have, predictably, read the headline before the detail. Middle East Eye reported at 04:49 UTC on 29 June that oil prices had risen after several days of tit-for-tat strikes had disrupted shipping through the Strait of Hormuz and reignited concerns about global energy supplies. The phrasing — concerns renewed, not conditions restored — captures the asymmetry of the moment: the news wires are pricing relief against a baseline that has already moved.

The absence of a formal document is itself the story. A ceasefire that requires only a Telegram post to summarise is a ceasefire that can be undone by the same medium. Western governments, Gulf monarchies, and Asian importers will be looking for an institutional anchor — a verification regime, an Omani or Qatari back-channel, a UN Security Council product — before they treat the pause as durable. None has been announced.

The two-week ledger, in plain terms

The reporting window since the strikes resumed has been short, sharp, and contained to a narrow geography. The incidents described by Middle East Eye centred on the Strait of Hormuz, the 21-mile-wide sealane between Iran and the Arabian Peninsula through which a disproportionate share of the world's crude and liquefied natural gas transits daily. Disruption there is not a marginal event; it is a global price event.

Three points should be made about the framing.

First, the term tit-for-tat implies symmetry. The maritime domain rarely produces clean symmetry. Iranian capability along the northern shore — fast-attack craft, anti-ship missiles, mining options — is geographically privileged. United States capability in the Gulf is naval, allied, and offshore. When both sides strike, the immediate casualty surface and the immediate insurance surface are different. The headline conceals that asymmetry.

Second, negotiations in this context is a vessel term. The two governments have a long history of near-agreements, last-minute pauses, and parallel tracks that produce neither war nor peace. The 2015 nuclear framework, the 2020 maximum-pressure collapse, and subsequent Omani-mediated exchanges all sit in this archive. A resumption of talks on 29 June is therefore not a discontinuity; it is a continuation of a pattern.

Third, oil prices rose is the part of the Middle East Eye line that will do the most economic work, and it deserves precision. The same reporting notes that the rise came after several days of disruption. Markets moved on the strikes; the ceasefire announcement now sets up a test of whether that move reverses. Initial price action in Asia following the 05:24 UTC post will be the first measurable verdict.

Why the Strait keeps doing this

The Strait of Hormuz is not just a piece of geography; it is a structural feature of the global energy economy, and structural features do not negotiate. Roughly a fifth of seaborne oil, and a significant share of LNG, transits the corridor. There is no overland substitute at scale on the timelines that importers operate. Insurance markets, tanker-routing decisions, and refinery input costs are all keyed to a single chokepoint.

This is what turns a regional exchange of fire into a global price event within hours. When the corridor is functioning, the premium for disruption is low and the market forgets. When the corridor is contested, the premium rises sharply and the market begins to price futures of disruption rather than just spot barrels. The Middle East Eye observation that prices rose after several days of disruption suggests the market is now operating in the second mode.

Two consequences follow. One, every actor with a stake in the corridor — Saudi Arabia, the UAE, Oman, Iraq, Kuwait, Qatar, the major Asian importers — has an incentive to push both sides toward quiet. Two, every actor with a stake in not having the corridor normalised — including factions inside Iran that view the Strait as leverage, and political constituencies in Washington that view restraint as weakness — has the opposite incentive. The ceasefire does not dissolve those incentives; it papers over them.

What remains contested and what has not been verified

The open-source record on the morning of 29 June is thinner than the headlines suggest. Several items are not in the public domain at publication:

- The identity of the mediating channel, if any. Oman's Muscat process has historically hosted back-channels; Qatar and Switzerland have played similar roles in different phases. No mediating party has been named in the items reviewed.

- The scope of the cessation of strikes. A halt to direct US-Iranian exchanges is one thing; an extension to Iranian proxies — Houthi action in the Red Sea, militia posture in Iraq and Syria — is another. The OSINTdefender post is silent on this.

- The duration of the pause. Two weeks is the working assumption in some trading-desk chatter; nothing in the cited material confirms a timeframe.

- The status of pre-existing sanctions architecture, nuclear-file negotiations, and any prisoner-exchange track. These run on separate clocks and were not addressed.

Monexus treats the cessation of strikes and the resumption of negotiations as the only verified elements of the 29 June development. Everything else is working assumption, market positioning, or analyst expectation. That distinction will matter if the announcement collapses.

Stakes, and what to watch next

If the ceasefire holds, the immediate beneficiaries are importers — China, India, Japan, South Korea, and the European Union — whose marginal barrels depend on the corridor functioning. Refiners in Singapore and Rotterdam that had repriced disruption risk will see insurance and freight rates ease. Gulf producers, whose export volumes were being discounted by perceived risk, will see a partial restoration of realised prices. The United States, as both a producer and a security guarantor, gains from a quiet Gulf without the diplomatic cost of a formal agreement.

If the ceasefire collapses, the same chain runs in reverse, but faster. Insurance markets price in days; tanker re-routing around the Cape of Good Hope adds weeks to delivery; strategic petroleum reserve drawdowns become politically salient. A second disruption event inside a fortnight would also harden the structural read: that the Strait of Hormuz is now an enduring premium in the global price of energy, not a contingent one.

The next 72 hours will tell which trajectory is operative. Watch for three signals: a named mediator or third-party host; a verifiable incident count at or near zero across the northern shore of the Gulf; and an OPEC+ or Saudi-UAE public statement that prices a return to normal cargo flows. The absence of all three by midweek would suggest that what is being called a ceasefire is in fact a breathing space — useful, expensive to maintain, and structurally fragile.

This article treats the 29 June announcement as a working pause, not a resolution, and will be updated as primary-source verification of its terms becomes available.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/s/OSINTdefender

- https://t.me/s/middleeasteye

- https://t.me/s/OSINTdefender

- https://t.me/s/middleeasteye

- https://t.me/s/OSINTdefender/