Strait of Hormuz: How a 33-kilometre choke point became Iran’s leverage play against the world

Tehran has declared a sovereign right to control parts of the waterway through which a fifth of the world’s oil passes. Polymarket traders give it 50-50 odds that transit fees follow by the end of August.

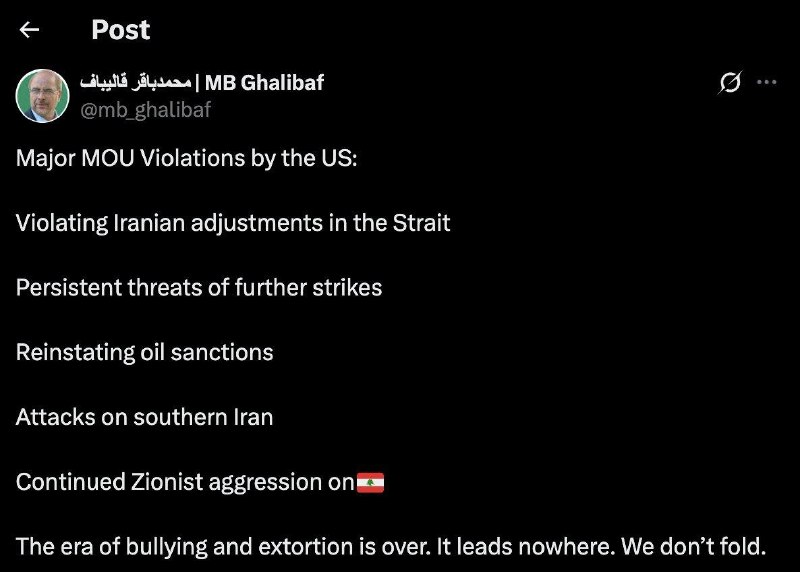

At 16:34 UTC on 7 July 2026, a wire channel tied to prediction-market operator Polymarket flashed a single line across trading desks: Iran had declared that it held a sovereign right to control “parts” of the Strait of Hormuz. Seven minutes earlier, the same operator had listed a contract pricing the odds of Tehran charging transit fees on Hormuz shipping by the end of the following month at 50-50. Within an hour, the messaging channel Clash Report was carrying a line from Mohammad Bagher Ghalibaf, the speaker of Iran’s parliament, telling domestic audiences that “the era of bullying and extortion is over. It leads nowhere. We don’t fold.” And by 16:27 UTC, the markets channel Unusual Whales had reposted a Guardian report that Iran had intensified attacks on vessels in the strait, language that fuses the political declaration, the financial bet and the kinetic threat into a single, escalating picture.

The story this publication is watching is not whether a single tanker gets hit. It is whether the world’s most consequential oil chokepoint is being converted, in plain sight, from a public good into a tool of state leverage — and whether the bet that Iran can monetise that leverage is, as of this week, a 50-50 proposition among people putting real money on the outcome.

A 33-kilometre funnel for a fifth of the world’s oil

The geography has not changed. The Strait of Hormuz, between Iran to the north and Oman and the United Arab Emirates to the south, narrows to roughly 33 kilometres at its tightest point, with shipping lanes in each direction confined to two-mile-wide channels. By any standard accounting, more than a fifth of globally traded crude — and a comparable share of liquefied natural gas — moves through it every day. The strait is the exit valve for Saudi Arabian, Iraqi, Kuwaiti, Qatari and Emirati production, and the import corridor for the major Asian economies whose refineries are calibrated to Middle Eastern grades.

What changed this week is rhetorical posture. Tehran’s claim of a sovereign right to control “parts” of the waterway is not, on its face, a new doctrine. Iran has asserted oversight over its northern littoral for decades, and the legal landscape of transit passage — codified under the United Nations Convention on the Law of the Sea — is contested terrain. The novelty is the packaging: a public declaration of authority, a parliamentary speaker framing the moment as the end of “bullying and extortion,” and a simultaneous uptick in vessel attacks reported by a major Western wire. The three threads are converging fast enough that a market has decided they belong on a single trading screen.

The Polymarket signal: priced as a coin-flip

The Polymarket contract listed on 7 July 2026 — “50% chance Iran charges Hormuz fees by the end of next month” — is the cleanest read we have on how informed money is sizing the risk. A 50-50 price is not a prediction; it is an admission that the path is genuinely uncertain, and that the resolution criteria — an Iranian-imposed fee, however framed, on shipping that the international community treats as free transit — could be triggered by any one of several moves.

The market is doing something the official press corps is not. It is forcing a numerical answer to a question that diplomats prefer to leave vague: is Tehran bluffing, or is it preparing an instrument? When Polymarket trades at 50-50, it usually means that the smart money has already decided it does not know — and that the marginal price move over the next 72 hours will track operational evidence on the water, not statements in parliament.

It is worth saying plainly what a Hormuz transit fee would look like in practice. Even a modest levy — a few dollars per barrel on the estimated 17 to 21 million barrels a day that move through the strait — would amount to tens of millions of dollars a day in revenue for the Iranian state, and a comparable per-barrel surcharge for every Asian importer from Beijing to New Delhi. It is the kind of instrument that, once introduced, is very hard to walk back, because the credibility of the threat depends on Tehran continuing to enforce it.

What ‘intensified attacks’ actually means at sea

The Guardian report flagged by Unusual Whales on 7 July uses the word “intensified,” which in shipping-security vocabulary usually means one of three things: a higher tempo of small-boardings or seizures, a shift from nuisance incidents to strikes on vessel hulls, or an expansion of the geographic box in which incidents are reported. The wire reporting available to this publication confirms only the direction, not the precise mechanism, and the sources disagree on whether the recent pattern amounts to a campaign or a spike.

What the wire reporting does establish is that the targeting is being framed, in Tehran, as a response to “bullying and extortion,” in Ghalibaf’s words — language that locates the action inside a longer Iranian narrative about sanctions enforcement, frozen assets and the legal status of the nuclear file. That framing matters because it suggests the attacks on shipping are not being treated, by the Iranian side, as a separate track from the diplomatic one. They are the enforcement layer of the political claim.

The counter-read, which any honest analysis has to put in the room, is that a Hormuz transit fee and a sustained campaign of attacks on shipping are not the same thing. The former can be introduced with a single, public decree; the latter is a continuous operational programme with its own escalation ladder. It is possible — and the markets may eventually price this — that Tehran intends only the first, and that the kinetic activity is designed to set the table for a negotiation in which the fee is offered as the de-escalatory off-ramp. The Polymarket contract is structured to resolve on the fee, not on the attacks. That is a tell.

The structural frame: leverage in a dollar-priced world

Stripped of rhetoric, the move is about leverage — specifically, about what leverage looks like for a mid-sized power whose financial system is ringed by sanctions, whose currency is not freely convertible, and whose conventional military cannot project far from its own coastline. In that position, geography is the only asset class that cannot be sanctioned.

The wider context is that the price of oil is set in dollars, that the clearing infrastructure for that oil runs through a small number of Western-controlled chokepoints of its own — the messaging systems, the insurance markets, the banking rails — and that the United States has, over the past two decades, repeatedly used that infrastructure as a foreign-policy instrument. From the Iranian vantage point, the argument that the strait is a shared public good has always cut both ways. If the global oil trade can be weaponised against Iran, then the strait through which that trade moves can be weaponised in return. The new claim of a sovereign right to control “parts” of the waterway is, in that sense, not a break with the existing order so much as a mirror of it.

The Asian importers — China, India, Japan, South Korea — are the silent principals in this calculation. They are the customers whose refineries must be kept running, whose political support Tehran needs if a fee regime is to have any chance of being accepted, and whose diplomats have spent two decades trying to keep the Hormuz question off the front pages. A transit fee that is paid quietly by Asian buyers is one thing. A transit fee that requires European insurers to write new clauses is quite another, and the diplomatic work of getting from the first to the second will define the next month.

What remains uncertain — and what this publication is watching

The source material this article is built on is thinner than the stakes warrant, and that is itself a finding. We have a parliamentary statement, a prediction-market price, a wire report of “intensified” attacks and a social-media relay. We do not have a confirmed fee schedule, a list of named vessels hit, a casualty count, an official Iranian regulatory text, or a response from any of the five littoral states on the southern side of the strait. The Polymarket price is the most honest single number in the file, and it is, by construction, a confession of uncertainty.

What this publication will be watching over the next two weeks is straightforward. First, whether the Polymarket contract moves off 50-50 — in either direction — as operational evidence accumulates. Second, whether the Iranian declaration is followed by a written instrument, or whether it remains at the level of parliamentary rhetoric. Third, whether the pattern of attacks reported in the Guardian extends to flagged vessels of major Asian importers, which would be the test of whether the leverage is being aimed at the global system or at specific counterparties. Fourth, and most quietly, whether any of the southern littoral states — the Sultanate of Oman, the United Arab Emirates — say anything in public. Their silence, or its absence, will be the loudest signal of all.

A 33-kilometre funnel is now the front line of an argument about whether the global oil trade is, in the last instance, governable by consensus or by capacity. The markets have decided, for the moment, that the answer is genuinely in doubt. The next month will be the proof.

Desk note: Monexus is framing this as a leverage question, not a war question — the political declaration, the prediction-market contract and the shipping incidents are being treated as one story, because that is how the participants are treating them. The source list is short because the public record is short; we have resisted the temptation to pad it with synthesised context.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/ClashReport

- https://x.com/polymarket/status/