Trump demands probe into gasoline 'gouging' as crude keeps falling — and pump prices don't

Crude has dropped sharply. Retail gasoline has not followed at the same pace. The President wants regulators to ask why.

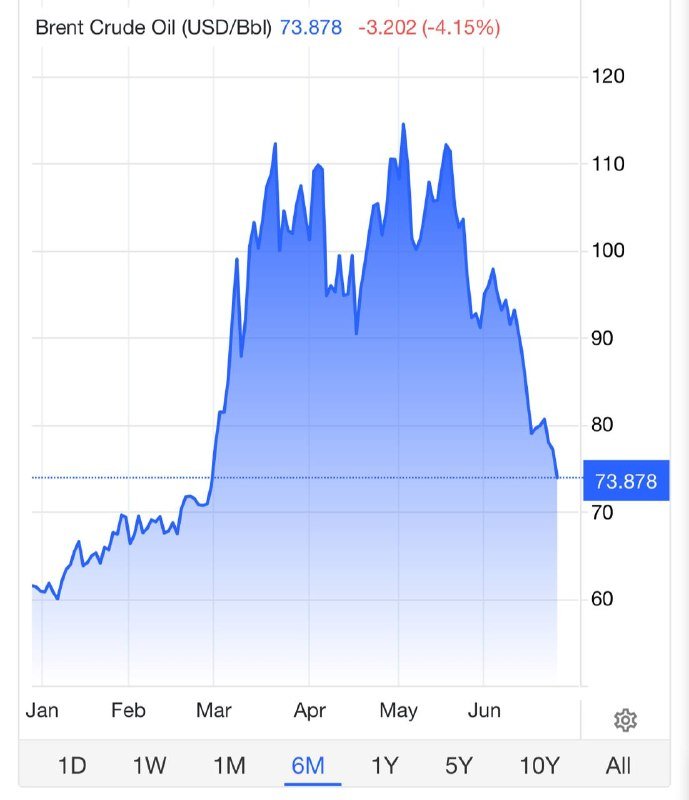

Crude oil has been sliding for weeks. The price at the American pump has not slid at anything like the same pace. On 24 June 2026, the gap between those two trajectories moved from a market story to a White House story: Donald Trump publicly called for a federal probe into what he described as gasoline price "gouging" by major oil companies, accusing refiners and retailers of holding pump prices artificially high even as their input costs fall.

The intervention lands at an awkward moment for the domestic energy industry. Wholesale crude benchmarks have eased materially through the spring of 2026, yet retail gasoline averages in the United States have lagged the move — a disconnection the industry attributes to refining margins, distribution costs and the seasonal shift to summer-blend fuels, and that the White House now says amounts to profiteering.

What Trump said, and where

The President's remarks surfaced across his own channels and were carried by Reuters on 24 June 2026 at 06:05 UTC. The framing was unusually blunt for a Republican administration historically aligned with domestic producers and refiners: oil companies, Trump wrote, are "not dropping their price at the pump commensurate with the sharply lower prices they are paying for Oil." A second statement, in English-language coverage distributed by Al Alam Arabic, sharpened the demand: "Gasoline prices must start falling at a much faster pace than what I see now."

Both messages were amplified through Telegram by outlets including Clash Report and Al Alam Arabic in the early European morning, indicating the messaging was designed for fast, multi-language distribution rather than a single domestic audience. The political signal is plain. With midterm-adjacent voters sensitive to fuel costs and with crude prices in retreat, the White House is publicly picking a fight with the firms that sit between the wellhead and the corner station.

The industry counter

The American Petroleum Institute and major integrated majors have, in recent weeks, pushed back on the framing. Their case is structural rather than conspiratorial. Refining capacity in the United States is tighter than it was a decade ago, after a wave of plant closures and conversions to renewable-diesel feedstock. Summer driving season reliably tightens inventories and pushes crack spreads — the difference between crude and refined product prices — higher. Distribution, retail and tax costs sit on top of the wholesale number and do not move one-for-one with crude.

That defence has merit. The historical correlation between retail gasoline and crude is high but not perfect, and crack spreads have widened at moments when crude has fallen quickly. None of that, however, fully neutralises the political optics: when input prices fall and retail prices barely move, voters do not reach for a textbook on refinery utilisation. They reach for the word "gouging." The industry's challenge in the days ahead will be to communicate a credible, specific explanation of the spread before the political narrative calcifies.

A structural frame, plainly stated

The episode is best read as a stress test of an arrangement that has held for most of the post-shale era. The United States became the world's largest crude producer, and the industry consolidated into a smaller number of larger firms controlling more of the value chain. That consolidation delivered lower-cost supply and, by most measures, lower long-run prices than the import-dependent era it replaced. It also concentrated the rents between well and wheel.

When crude prices fall, the firms sitting in the middle of the chain capture the spread for as long as their inventories and contract books allow. When crude prices rise, the same firms tend to pass increases through faster. The asymmetry is not a secret; it is the business model of a vertically integrated downstream sector with limited spare refining capacity. It is also precisely the kind of market structure that draws political attention in a year when pump prices feature prominently in household budgets and the executive branch wants to be visibly on the side of the consumer.

The call for a probe is itself a market signal. Threatened antitrust or price-gouging scrutiny raises the cost of holding retail prices elevated, because the expected penalty for being seen to do so rises. Even before any formal action, refiners and retailers now face a higher political discount on the margins they might otherwise retain through the summer driving season. That is the mechanism the White House is activating, regardless of whether a formal investigation ever opens.

Stakes and what to watch next

For the industry, the near-term calculus is straightforward: how aggressively to reduce posted retail prices, and how loudly to explain the structural reasons they cannot fall dollar-for-dollar with crude. Both choices carry risk. Aggressive pass-through compresses margins but buys political goodwill and reduces the chance of a formal Federal Trade Commission or state attorneys-general action. A more cautious posture preserves earnings but invites exactly the probe the President has now publicly requested.

For consumers, the test is whether retail prices respond meaningfully within the next two to four weeks. A material drop would defuse the political row and reinforce the credibility of market mechanisms. A continued lag would harden the case for intervention and could pull state-level attorneys-general — particularly in high-price coastal markets — into parallel inquiries.

For the broader energy picture, the episode underlines a tension that will outlast this news cycle. Industrial policy in the United States continues to favour domestic production, refining and downstream investment. Political pressure for cheap retail gasoline runs in the opposite direction whenever input costs fall. The two objectives are aligned when crude is high; they collide when crude is low. The current moment is firmly in the second category.

What remains uncertain

The sources do not yet specify which agency would lead a formal probe, nor whether the White House intends to direct the FTC, the Department of Energy or a state-level coalition to act. The industry has not, as of this writing, issued a coordinated public response to the specific framing of "gouging" — past practice suggests an API statement and individual company commentary in the coming days, but the timing and tone are not yet fixed. And the central empirical question — how much of the retail-crude gap is structural refining economics versus inventory-cycle pass-through versus market power — is contested. Analysts on both sides of the debate will, in the next week, produce their own numbers. The honest answer is that none of those numbers will settle the political question.

The political question is the one the President has put on the table, and it is the one the industry must now answer in public, with or without a formal investigation behind it.

Desk note: Monexus framed this as a stress test of vertical-integration rents in a falling-crude environment, rather than as a stand-alone price-gouging allegation. Reuters carried the wire; Telegram channels handled distribution; the industry's structural defence is given its full weight.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- http://reut.rs/4aje1D7

- https://t.me/ClashReport

- https://t.me/alalamarabic