Gulf strikes, drone shootdowns, and a Main Street pivot: parsing three threads from the US-Iran flashpoint

Missile strikes hit oil and gas facilities around the Persian Gulf, US forces shot down three of four Iranian one-way attack drones, and Treasury Secretary Scott Bessent is recasting the administration's economic agenda as a break from four decades of asset-led growth.

Three dispatches circulated in the early hours of 2026-06-29 UTC describe a single, interlocking crisis. Iranian missile strikes have hit oil and gas infrastructure along the Gulf. The United States has shot down three of four one-way attack drones launched by Iran, with the fourth striking the upper deck of a cargo ship. And inside the Treasury Department, Secretary Scott Bessent is reframing the Trump economic agenda as a deliberate break from the asset-led growth model that has defined US policy since the 1980s. Read together, the threads sketch a wartime American economy under reconstruction — one whose fiscal and industrial direction is being argued out while kinetic events in the Gulf set the tempo.

The pattern is not new, but the simultaneity is. A shooting war in the Middle East is being matched, almost in real time, by an explicit policy turn away from the wealth-effect economics that has long tied American household balance sheets to equity prices. The question is whether the rhetoric survives the contact with energy markets, supply chains, and a Treasury still issuing record gross debt.

What the Gulf strikes actually hit

Reporting carried by Nikkei Asia on 2026-06-29T04:31 UTC documents damage to oil and gas facilities around the Gulf during the military conflict between the United States and Iran. Missile strikes hit installations across multiple jurisdictions bordering the Strait of Hormuz, the corridor through which a significant share of globally traded crude and liquefied natural gas transits. The Nikkei dispatch frames the strikes as a direct hit on the physical infrastructure that anchors Gulf export volumes — not a symbolic attack on administrative targets, but on storage tanks, processing trains, and the pipeline clusters that feed export terminals.

That distinction matters. Energy-market analysts typically treat Gulf disruption as a flow shock that can be smoothed by stockpiles and spare capacity. Damage to midstream infrastructure — the storage, pumping, and processing nodes between wellhead and tanker — compresses that buffer. Rebuilding takes weeks to months, not the days that headline traders tend to assume. Until repair timelines are published, the relevant question is not whether barrels can be replaced but how long Gulf exporters can ship at full nomination.

The Nikkei framing does not specify individual facilities or provide dollar-value damage estimates in the available excerpt, and Monexus has not yet independently verified the precise inventory of damaged sites from primary sources. What is documented is that missile strikes hit oil and gas installations in the Gulf region during the US-Iran military conflict, and that the damage profile is consistent with an effort to degrade export capacity rather than to register a symbolic protest.

The drone exchange and the rules of engagement

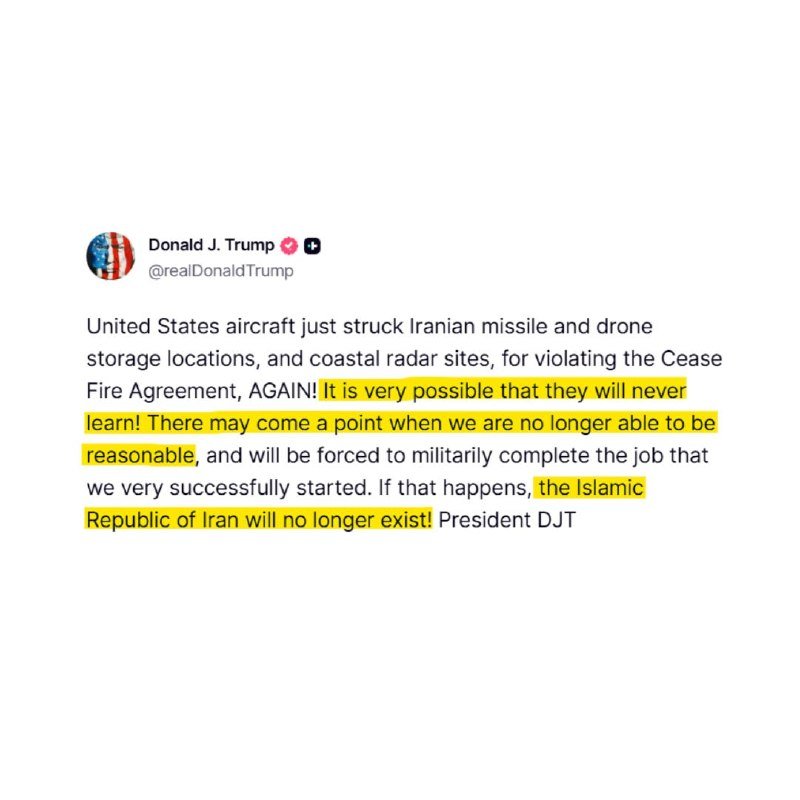

In a separate dispatch timestamped 2026-06-29T00:46 UTC, US President Donald Trump stated that American forces shot down three of four one-way attack drones launched by Iran, with the fourth striking the upper deck of a cargo-carrying ship. The framing places the exchange in the open waters of the Gulf or the wider Arabian Sea basin, where commercial shipping and military presence routinely overlap.

The mechanics of one-way attack drones — munitions that loiter, identify a target, and dive on it without recovering — are designed to saturate defensive screens. A three-out-of-four interception rate is operationally respectable but not reassuring for tanker crews. Even a single confirmed hit on a commercial hull changes insurance premia, routing decisions, and reflagging behaviour across the global fleet within days. The reported strike on the cargo ship's upper deck, if corroborated by vessel-tracking data and owner statements, would be the first confirmed Iranian drone strike on a commercial hull in this exchange.

This publication has not yet located independent confirmation of the specific incident from the ship's operator or from maritime authorities; the available sourcing for the strike runs through Trump's own statement as carried by Unusual Whales. That is a thin evidentiary base. The pattern of one-way drone use against both military and civilian targets in the Gulf is, however, consistent with Iran's published doctrine of layered deterrence in the Strait of Hormuz.

Bessent's pivot and the asset-led growth question

The third thread, timestamped 2026-06-28T03:16 UTC, captures Treasury Secretary Scott Bessent reframing the Trump economic agenda as a deliberate break from four decades of asset-led growth. The phrase is a direct repudiation of the post-Reagan policy consensus under which Federal Reserve policy, tax cuts, and deregulatory priorities have been justified, in significant part, by their effect on equity, real estate, and other asset prices — on the theory that wealth-effect spending would lift the broader economy.

Bessent's framing, as reported, recasts the policy goal as Main Street production rather than portfolio values. That is a non-trivial repositioning. It implies tolerance for higher rates and tighter financial conditions if those conditions are the cost of rebuilding domestic manufacturing capacity; it implies that stock-market drawdowns will be treated as policy inputs to be absorbed rather than emergencies to be reversed; and it implies a more sceptical view of the asset-valuation channel that has shaped Republican and Democratic economic thinking alike since the Volcker era.

The intellectual content here is familiar — the critique that asset-led growth hollows out working-class balance sheets even as it inflates headline wealth — but the political positioning is novel. A Treasury secretary stating that the goal is to wean the economy off asset-driven demand is, in effect, conceding that the prior framework was a choice and not a law of nature. The markets have not yet been asked to price what that means for the duration of elevated long yields, for the relative valuation of capital-intensive industrials versus asset-light platform companies, or for the fiscal trajectory.

How the three threads fit together

The composite picture is an administration conducting a hot kinetic operation in the Gulf while arguing, simultaneously, that the domestic economic order of the past forty years needs to be rebuilt. The two are not contradictory — they may, in fact, be complementary. A Middle East energy shock that pushes consumer fuel prices higher is politically manageable only if the administration can point to a domestic production and industrial base that benefits from the dislocation. Bessent's pivot is most legible in that light: the war is the externality; the industrial policy is the response.

The risk in the framing is that it relies on the Gulf disruption being short and shallow. If the strikes documented by Nikkei prove extensive enough to require multi-month reconstruction, the energy-price pass-through will erode the political space for any pivot, asset-led or otherwise. Brent and benchmark Gulf crudes, in that scenario, would do the work that Fed tightening never could — drain real household incomes at exactly the moment the administration is asking Main Street to absorb the cost of an industrial rebuild.

The counter-narrative, worth taking seriously, is that the pivot is rhetorical cover for a budget trajectory that the bond market would otherwise reject. If gross Treasury issuance continues to climb while Bessent signals tolerance for tighter financial conditions, the implicit bet is that foreign and domestic buyers will absorb the supply at yields high enough to clear the market. That is a testable proposition, but it is not the same proposition as rebuilding American industry. The two can diverge sharply if fiscal arithmetic forces a course correction.

What remains uncertain

Three evidentiary gaps shape this picture. First, the inventory and severity of damage to Gulf oil and gas facilities has been characterised in broad terms by Nikkei Asia but not yet enumerated facility by facility; the operational consequence depends on that detail. Second, the Iranian drone strike on a commercial cargo ship rests, in the available sourcing, on the US president's own account; independent confirmation from the vessel operator or maritime authorities is the standard that would lift the report from statement to established fact. Third, Bessent's pivot has been articulated but not yet stress-tested against a Treasury issuance calendar or a sustained Gulf energy shock. Until those tests arrive, the new framing is best read as an announced direction rather than a settled policy.

Monexus will update this picture as primary-source verification arrives on each thread. The working hypothesis, consistent with the available material, is that the Gulf conflict and the domestic economic pivot are being managed as a single integrated posture — but the integration is contingent on the depth of the energy disruption, the duration of the military exchange, and the bond market's patience with the announced direction.

This article treats the three threads in parallel rather than as a single unified event. Monexus reads the Gulf strikes as reported by Nikkei Asia, the drone exchange as stated by President Trump and carried by Unusual Whales, and the Bessent pivot as reported in the same Unusual Whales feed. Where the reporting rests on a single named source, that limitation is flagged in the body. Where the available material does not specify a figure or attribution, the gap is named rather than filled.