After the Strait: What a Quieter Hormuz Actually Means

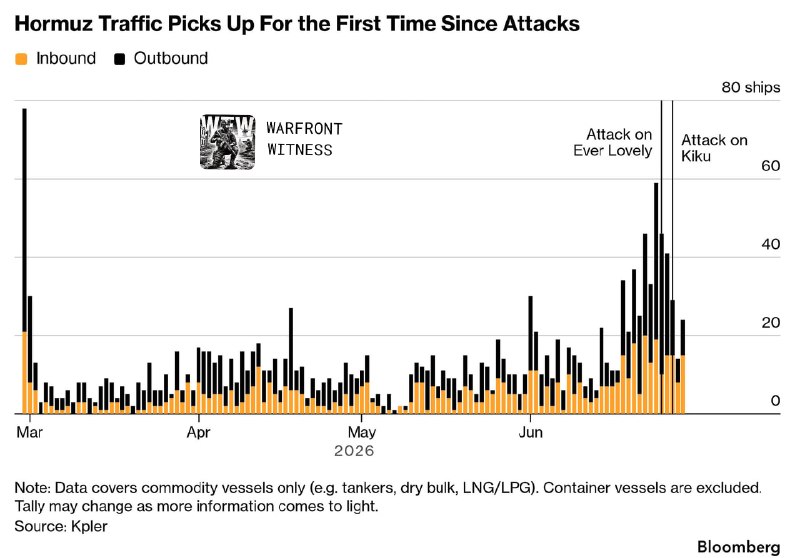

Traffic through the Strait of Hormuz is recovering after weeks of disruption, but it remains below normal. The pattern matters less for the barrels than for what it says about who is now underwriting the route.

Commercial shipping through the Strait of Hormuz has climbed past ten million barrels per day in recent weeks, with United States military support credited by Western wire reporting with helping restore oil flows along the waterway, according to a 1 July 2026 Telegram post citing Bloomberg. The same Bloomberg data, flagged by the markets account Unusual Whales the same afternoon, shows traffic recovering but still below the corridor's normal baseline. The gap between the two readings — a surge, and a still-subdued baseline — is the story. Whatever closed partially across the spring did not snap back to where it was, and the United States is now the visible underwriter of the route.

What looks like a routine recovery is a quiet rearrangement of who guarantees one of the world's most consequential energy corridors. The Strait of Hormuz sits between Oman and Iran and links Persian Gulf producers to the Gulf of Oman, the Arabian Sea and, from there, the rest of the world's tanker fleet. Disruption there does not merely move a price — it removes the discount that markets have historically applied to oil supplied through a single chokepoint, and forces buyers and sellers to rebuild that margin through insurance, rerouting, and political guarantees. The fact that those guarantees are now visibly American is the change that will outlast the headlines.

What the traffic data actually says

The headline number — ten million barrels per day, with U.S. military help cited — frames the Strait as a problem essentially solved. The more cautious reading, in the same Bloomberg thread, is that traffic is picking up but remains below normal. Both can be true at once: a corridor that fell sharply can rise sharply without returning to its prior level, and the percent change off a depressed base overstates the recovery. Without the absolute pre-disruption baseline in the public wire items, the honest reading is the cautious one — that the route is healing, not healed.

The U.S. contribution to that healing is the more consequential variable. If American naval escorts, surveillance and intelligence sharing are the difference between a transit corridor and an insurance crisis, then the chokepoint's risk premium has been partially converted into a U.S. security bill — one that ships, charterers, and ultimately oil buyers will pay in some form. The geopolitical reading is straightforward: a corridor that the world relies on for a large share of seaborne crude is now safer to use partly because Washington has chosen to make it safer. That is a strategic asset, not a neutral service.

The Iranian counter-read

The Iranian framing, surfaced the same day by the state-aligned outlet Tasnim in English, treats the Strait not as a transit route but as a "security asset" — a phrase that recasts a common waterway as something a sovereign can ration. The argument runs that political initiatives should be measured by strategic criteria, and that the end of any single battle is not the end of the underlying competition. Read plainly, this is the case that the corridor's openness is contingent, not contractual; that the calm is a permission that can be revoked; and that the pricing of oil through Hormuz should reflect not just current insurance and freight but a political risk premium attached to Iranian discretion.

That framing is not the preserve of Iranian state media alone. It is the implicit operating assumption of every oil trader who, in quieter weeks, books a Hormuz transit at a thin margin and in tenser weeks pays a war-risk surcharge. The Tasnim editorial is unusual only in saying out loud what the market already does in its spreads. The Western reporting that frames the recovery as a U.S. success and the Iranian commentary that frames the corridor as a strategic lever are not contradictory — they are two halves of the same transaction. One side is being paid in barrels; the other is being paid in leverage.

Why a quieter Hormuz is not a settled Hormuz

The structural problem is older than the present episode. Roughly a fifth of globally traded oil moves through the Strait, and the corridor's narrow shipping lanes, with the two-mile inbound and outbound channels, leave little room for error at the best of times. A serious incident — a seizure, a mining, a sustained drone or missile campaign — does not need to close the waterway to close the price. It needs only to make insurance, or the willingness of crews to sail, uneconomic.

That is why the U.S. military presence in the Gulf matters beyond any single convoy. American naval assets in the Fifth Fleet area, combined with allied contributions, are what allow commercial underwriters to keep writing Hormuz transit cover at non-stressed rates. When that cover thins, as it did earlier in the disruption, the visible effect is not empty water but fewer sailings, longer round trips, and a bid for non-Middle East barrels — West African, North Sea, U.S. Gulf, Brazilian — that pushes the global benchmark up before any physical shortage is felt. The recovery, then, is partly a recovery of willingness to sail underwritten by a specific flag.

Who pays, who gains, and what the new map looks like

The actors with the most to gain from a quiet Hormuz are the same ones with the most to lose from a noisy one. Gulf producers — Saudi Arabia, the UAE, Kuwait, Iraq, and Qatar for LNG — need the corridor open to convert their reserves into revenue on terms the market will accept. They also need it open to maintain the customer relationships that diversify their sales away from any single buyer. A Strait that only works because U.S. forces underwrite it is, for them, both a relief and a quiet erosion of their own pricing power: the more the route's safety is associated with one outside power, the more the political conversation about Middle Eastern energy flows is held in that power's vocabulary.

Iran's position is more layered. Tehran benefits when the corridor is contested, because contested energy routes lift the global price and reward Iran's ability to act on the margin — through proxy capabilities, through the IRINMCN's maritime posture, and through the periodic detention of commercial tankers. It loses when the corridor is quietly secured by a coalition that can absorb the cost of keeping it open. The Tasnim framing of the Strait as a strategic asset is, in effect, a reminder that Iran's leverage is highest at the moment of tension and lowest at the moment of recovery — and that even a partial recovery narrows Tehran's room to manoeuvre.

For the United States, the strategic dividend is subtler. A stable Hormuz underwrites the dollar pricing of oil, which remains the spine of the petrodollar arrangement that has shaped global finance for half a century. It also gives Washington a continuing reason to maintain a naval posture in the Gulf that doubles as a presence alongside partners from the GCC and, increasingly, India — a country that buys most of its crude through Hormuz and has its own reasons to keep the corridor open. The cost of that posture is real, in hulls, in fuel, in readiness. The benefit is measured in something harder to price: the ability to ensure that a contested stretch of water does not, on any given week, become the world's most expensive insurance policy.

What remains contested, and what the wires have not settled

Three things the available reporting does not resolve, and which a careful reader should hold open. First, the absolute baseline: how far below normal traffic actually is. The Bloomberg-sourced thread says recovery, not full recovery; without a specific pre-disruption daily figure in the public reporting, the size of the remaining gap is a matter of inference. Second, the precise U.S. military contribution: escort operations, intelligence sharing, and maritime surveillance can all be described as "support," but they carry different cost and risk profiles, and the wire items do not break out which is doing most of the work. Third, the durability of the calm. The Iranian framing of the Strait as a strategic asset is a statement of intent as much as of fact; the next test is whether the corridor's openness holds through a quarter without a headline incident.

A sober reading of the present picture is that the water is calmer, the insurance market is thinner than it would be in a fully settled baseline, and the difference between the two is currently being paid for in U.S. naval posture and in the political patience of Gulf capitals. None of that is a permanent equilibrium. It is a working arrangement — one that will be tested the next time a tanker is detained, the next time a drone is launched, the next time an underwriter decides that the premium no longer matches the risk.

The Strait of Hormuz was never just a transit route. It is a stage on which the world's largest energy importers and exporters argue, in the only language they all share — the language of barrels in motion and dollars committed. The current argument is being won, in its narrow tactical sense, by the side willing to keep the lights on in the corridor. The larger argument — over who sets the terms under which the corridor opens at all — is not over, and the wire items from this week do not pretend that it is.

Desk note: Where the wire reporting frames the Hormuz recovery as a U.S.-backed restoration of flows, Monexus has paired that line with the Iranian counter-reading of the corridor as a strategic asset. The point is not to balance one official line against another, but to make visible the bargain the market is currently pricing: openness in exchange for an external security guarantee whose political weight extends well beyond the waterway itself.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/wfwitness

- https://t.me/tasnimnews_en

- https://en.wikipedia.org/wiki/Strait_of_Hormuz

- https://en.wikipedia.org/wiki/United_States_Fifth_Fleet

- https://en.wikipedia.org/wiki/Petrodollar

- https://en.wikipedia.org/wiki/Iranian_Revolutionary_Guard_Corps_Navy

- https://en.wikipedia.org/wiki/War_risk_shipping_insurance