The $2.2 billion disclosure and the presidency as a profit centre

A mandatory financial disclosure lands $2.2 billion in a single year, with crypto overtaking property. The number reframes the office itself.

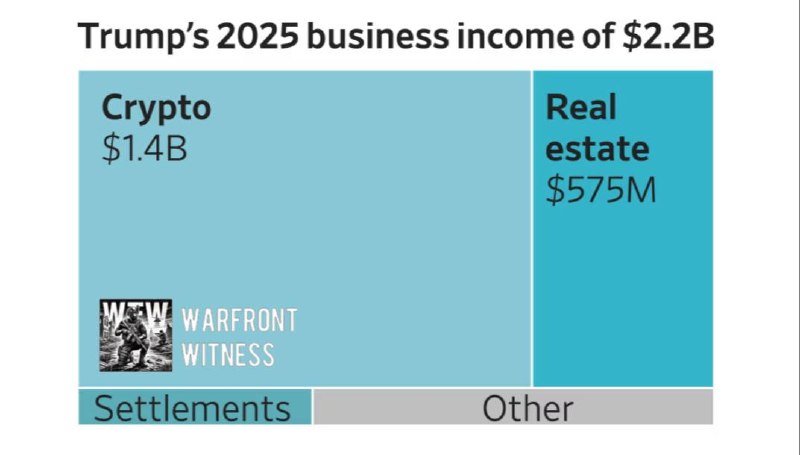

On 2 July 2026 the Office of Government Ethics released Donald Trump's annual financial disclosure, and the document does something modest on the surface and something enormous underneath. It reports roughly $2.2 billion in total income across the president's holdings, with about $1.4 billion flowing from crypto ventures and roughly $575 million from real estate — a near-mirror inversion of the portfolio most Americans still associate with the Trump brand (per coverage summarised by The Canary UK on 2 July 2026; WSJ figures cited by World Financial Witness the same day).

Strip away the headlines about scale and a sharper question emerges. What does it say about a republic when the man holding the office that commands the world's largest military, the nuclear codes, and the appointment power over federal regulators, can report an annual personal income that exceeds the GDP of several UN member states — and that income is concentrated in an asset class whose value depends, in part, on the goodwill of the very apparatus he controls?

What the disclosure actually shows

The headline figure is the $2.2 billion. The composition matters more. Crypto ventures produced about $1.4 billion in 2025; real estate produced about $575 million; the rest came from settlements and smaller business lines, per WSJ reporting cited by World Financial Witness on 2 July 2026. The disclosure is mandatory, signed under penalty of perjury, but it is also a snapshot — not an audited ledger — and it captures gross ranges rather than verified net worth.

Two things stand out. First, the crypto line item now dwarfs the property line, contradicting the public image of a real-estate magnate that carried Trump through four decades of business and one prior presidency. Second, the disclosure does not identify counterparties to the crypto income — exchanges, token issuers, treasury firms, foreign partners — and the Office of Government Ethics does not require it to.

That second point is the one that ethics lawyers tend to underline. The disclosure tells the public how much was earned. It does not tell the public from whom, on what terms, or under what regulatory standing.

The other fifty states

Presidents have always had wealth, and disclosure has always been leaky. What changed between Trump's first term and now is the structure of opportunity. In 2017 a sitting president's conflicts were largely real-estate-mediated: lease payments, foreign bookings at hotels, branded towers in capitals where the US had diplomatic interests. Today's pipeline runs through token launches, treasury vehicles, and digital-asset deals whose counterparties can sit in any jurisdiction and whose regulators are still being built. The conflict is the same — personal wealth intersects with state power — but the surface it flows across is harder to police and easier to obscure.

The dominant framing in the American press treats $2.2 billion as a corruption story. The framing in the crypto-friendly press treats it as proof that the industry has matured into a legitimate asset class. Both framings miss the more uncomfortable point: the disclosure does not have to be fraudulent to be corrosive. It only has to exist.

Reading the structure

Consider what a foreign government, a state-aligned fund, or a regulated exchange faces when negotiating with an American counterparty whose ultimate decision-maker reports a nine-figure crypto income. The negotiating party can route a transaction through a treasury vehicle, a token-purchase agreement, a licensing deal, or a hospitality line — each clean in form, each dependent on regulatory and political conditions the office in question can influence. The disclosure requirement makes the result visible. It does not make the pattern stoppable.

This is the darker version of an argument American institutions have made for decades about lobbying, contracting, and regulatory capture. Disclosure was supposed to be the disinfectant. The 2026 disclosure is the case study in why disclosure, on its own, does not disinfect much. Sunlight shows the volume. It does not interrupt the flow.

The structural fact is also a political fact. A sitting president with several billion in disclosed crypto exposure is, in effect, the lead promoter of an asset class under his own regulators' supervision. The SEC, the CFTC, the Treasury — each has, somewhere in its recent rulemaking, a decision that touches the price of tokens in which the president reports a material position. This is not an accusation. It is the shape of the disclosed portfolio.

Stakes, now and after

If the disclosure marks a new normal, three things shift. First, future presidents of both parties will face pressure to show crypto holdings, and to show them big — the political reward for visible participation in the asset class is now established. Second, conflict-of-interest law, written for real-estate and equity, will be tested against tokens, treasury companies, and decentralised-finance positions it was not designed to police. Third, the international audience that watches American self-governance will read the $1.4 billion figure not as scandal but as a confirmation: the presidency is now openly a platform for personal accumulation.

The counter-reading deserves a hearing too. Trump's supporters argue that the wealth was earned openly, disclosed under oath, and concentrated in an industry the administration has championed through elected policy — not hidden. Crypto-industry voices argue the same point with enthusiasm. Both are not wrong. They are both, however, addressing the wrong objection. The objection is not disclosure. The objection is that the office itself has become indistinguishable from the holding company that surrounds it.

The disclosure is dated 2 July 2026. The next one is twelve months away. By then the composition will have shifted again, and the question of whether the United States can credibly regulate an industry in which its chief executive is the largest disclosed beneficiary will still be unanswered. That is not a one-year problem. It is a structural one — written in dollars, repeated annually, on the public record.

Desk note: this publication led on the composition of the disclosure (crypto versus real estate) and on the structural conflict it documents, rather than the headline dollar figure alone.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/TheCanaryUK

- https://t.me/wfwitness