The Red Sea is open again — and shipowners don't trust it

The ceasefire between Washington and Sanaa's de facto authorities is holding in name. The freight market is voting with its hulls and saying the war risks are still too live to resume the Suez shortcut.

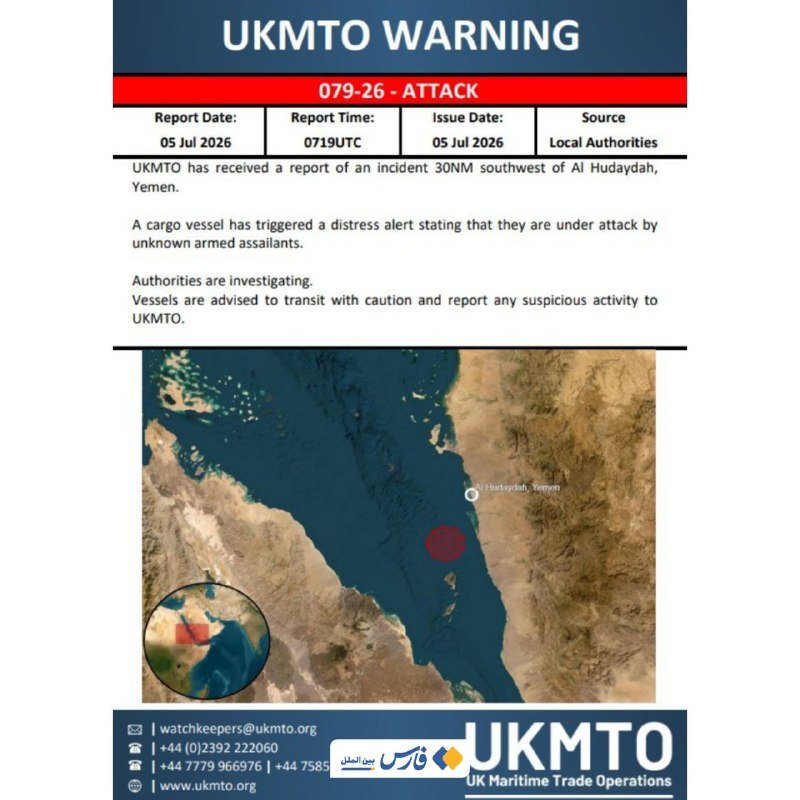

On 5 July 2026, at 08:53 UTC, the United Kingdom Maritime Trade Operations centre issued an attack warning: a cargo vessel had triggered a distress alert reporting it was under attack by unknown armed assailants 30 nautical miles southwest of Al Hudaydah, the Houthi-controlled Yemeni port city. The geographic plotter @wfwitness relayed the UKMTO bulletin in real time; @AMK_Mapping placed the incident in context a half-hour later. The vessel, her cargo and her eventual fate remain unconfirmed. The frame does not: a corridor that is officially being marketed as reopened for commercial traffic has, on the same morning, produced another live distress call.

The discrepancy between diplomatic language and operational risk is the story. A ceasefire arrangement between Washington and the Sanaa authorities has held in name. Naval task forces have repositioned. Insurance underwriters have, in some cases, quietly trimmed their war-risk premia. And yet the freight market — the most honest pricing mechanism in global commerce — is still routing cargo the long way around Africa. The Cape of Good Hope detour adds roughly ten to fourteen days to Europe-Asia container voyages and burns fuel that a Suez transit does not. The market is paying that bill anyway. That is what the price says: shipowners do not yet believe the Red Sea is safe.

What 5 July actually shows

UKMTO's bulletin does not name the assailants. It does not name the vessel, the flag, the operator or the cargo. It confirms only the operational sequence: a distress alert was triggered; the position was 30 nautical miles southwest of Al Hudaydah; the reporting came through the UKMTO channel that the Royal Navy maintains for merchant traffic. The bulletin is the same format the centre has used since the Houthi campaign against commercial shipping began in late 2023. What 5 July shows is not a single dramatic event; it is the persistence of a pattern. The corridor is contested. The commercial layer of the route is contested.

Read alongside the wire reporting that has accompanied the broader ceasefire, the incident is a useful forcing function. If the arrangement were genuinely delivering maritime quiet, an alert in the waters off Al Hudaydah would be the exception that prompted an investigation. Instead it is one more bullet point in a long list. The volume of incidents, not the severity of any single one, is the operational signal that shipping desks read.

The pricing tells you what the press releases do not

Maritime insurance is the cleanest available thermometer. War-risk premia for Red Sea transits dropped when the ceasefire took hold in mid-2026, but they dropped from wartime peaks — they did not fall back to pre-2023 levels. Insurers are not pricing a return to normal commerce. They are pricing a corridor with a known attacker, known capability, and a known pattern of attack on ships in roughly the same operating area. Meanwhile container freight rates on the Asia-Europe lane — the lane that the Suez shortcut was built to serve — remain elevated versus the pre-disruption baseline. The Cape detour still consumes tonnage and fuel that the route would otherwise spare. Until freight indices converge back to pre-2023 norms, the trade press's talk of reopening is doing work the shipping markets are not.

There is also the question of cargo composition. Not all goods tolerate a ten-day delay equally. Consumer electronics, fast-fashion inventory and time-sensitive industrial inputs get pushed onto the air or onto a hull that will absorb the schedule hit. Dry bulk, energy and slower-moving manufactured goods tolerate the detour. The Red Sea is therefore reopening selectively, which is not the same as reopening. It is the kind of reopening that an underwriter recognises and a press release does not.

The structural frame

Maritime chokepoints are where the global economy's abstraction meets its physics. The Suez Canal handles roughly twelve per cent of global trade by value. The Bab el-Mandeb strait, which the Red Sea feeds into, sits between the same Horn of Africa coastline and the Arabian Peninsula that the current disruption is centred on. When a single actor — whether a recognised state, a non-state armed movement, or an allied naval coalition — can impose a meaningful cost on traffic through that corridor, the world's just-in-time logistics model reveals how much it depends on a small number of physical bottlenecks. The current episode is not novel in that respect. What is novel is that the actor imposing the cost is doing so in the context of an active regional war, an active ceasefire arrangement with a Western government, and a freight market that has already demonstrated it will route around the problem rather than absorb the risk.

The deeper pattern is the redistribution of leverage away from the platforms that built the modern shipping system and toward the actors who can credibly threaten the chokepoints those platforms depend on. Naval coalitions can escort; they cannot escort every hull. Insurers can discount; they cannot insure away a missile. Ceasefires can hold in headline form and still produce weekly distress alerts. The structural fact the market is pricing is that control of a corridor is no longer something that flows only from a blue-water navy.

Stakes

If the current arrangement holds long enough that the freight indices converge, the commercial story will become one of a successful diplomatic re-opening — and the underlying redistribution of leverage will continue, quietly, with shipowners as the residual risk-bearers. If the pattern of alerts persists at the rate the 5 July incident suggests, the Cape detour becomes the new operating baseline for an entire generation of container tonnage, with knock-on effects on shipping emissions, on the price of every Asian-manufactured good sold in Europe, and on the strategic logic of naval deployments in the Indian Ocean. Egypt, which earns hard currency from Suez transit fees, and Djibouti, which hosts the foreign naval bases that the response architecture depends on, have the most direct exposure. European importers and Asian exporters carry the rest.

What remains genuinely uncertain is whether the 5 July alert was an outlier, a deliberate test of the ceasefire's limits, or the leading edge of a renewed campaign. The sources available do not specify. UKMTO's bulletin is the operational record; it does not assign responsibility. Until the flag, the operator, the cargo and the damage assessment are public, the prudent read is that the corridor is being contested rather than closed, and contested is enough to keep the freight market voting with its hulls.

This publication treats Red Sea shipping disruption as a commercial story that happens to have a security backdrop, not the other way around — the price of moving a box from Shanghai to Rotterdam is the cleanest evidence the market produces.

Wire provenance

This editorial synthesis draws on the following public wire/social posts:

- https://t.me/wfwitness

- https://t.me/AMK_Mapping